This Content Is Only For Subscribers

In private credit, you don’t control the economy—or the borrower’s every decision. What you can control is the contract and the cash cushion. That’s the heart of risk management: reserves (money set aside to handle foreseeable bumps) and covenants (rules and early-warning alarms baked into the loan). Here’s a clear, investor-friendly guide to how each works and what to look for before you commit capital.

Reserves: cash cushions with a job to do

A reserve is money carved out at closing—or funded over time—for specific purposes. It lowers default odds by making sure the next bill gets paid even if the quarter is bumpy.

- Interest Reserve.

A pot of cash earmarked to cover interest payments during ramp-up periods (e.g., after an acquisition or during construction). It buys time for the borrower’s plan to start generating cash before debt service is due. - Operating/Working-Capital Reserve.

Funds to absorb normal volatility—seasonality, customer delays, inventory swings—so small hiccups don’t become covenant breaches. - Capex/Maintenance Reserve.

Keeps critical assets (equipment, properties, software) in working order. If a business starves maintenance in a tight quarter, long-run value erodes and recovery prospects fall. This reserve prevents that spiral. - Tax/Insurance Reserve.

Especially common in asset-heavy or real-estate deals, ensuring non-negotiable bills get paid on time. - Holdbacks/Escrows.

Sums withheld at closing to address identified risks (e.g., unresolved litigation, a delayed permit) that are released only when the issue is cleared.

How to judge reserves:

Ask who controls the account (lender, agent, or borrower), what release tests apply, and how quickly reserves would fund payments if performance dips. Good managers size reserves to realistic stress cases, not just the base plan.

Covenants: rules, alarms, and levers

Covenants are the operating manual for the loan. They don’t stop problems from happening; they surface them earlyand give the lender leverage to fix them while options still exist.

- Financial maintenance covenants (the early alarms).

Tested quarterly (or monthly in asset-based lending). Examples:- Leverage (Debt/EBITDA) caps prevent over-borrowing.

- Interest Coverage (EBITDA/Interest) ensures cash flow supports debt service.

- Fixed-Charge Coverage guards against thin free cash flow.

- Minimum Liquidity requires a cash or revolver cushion.

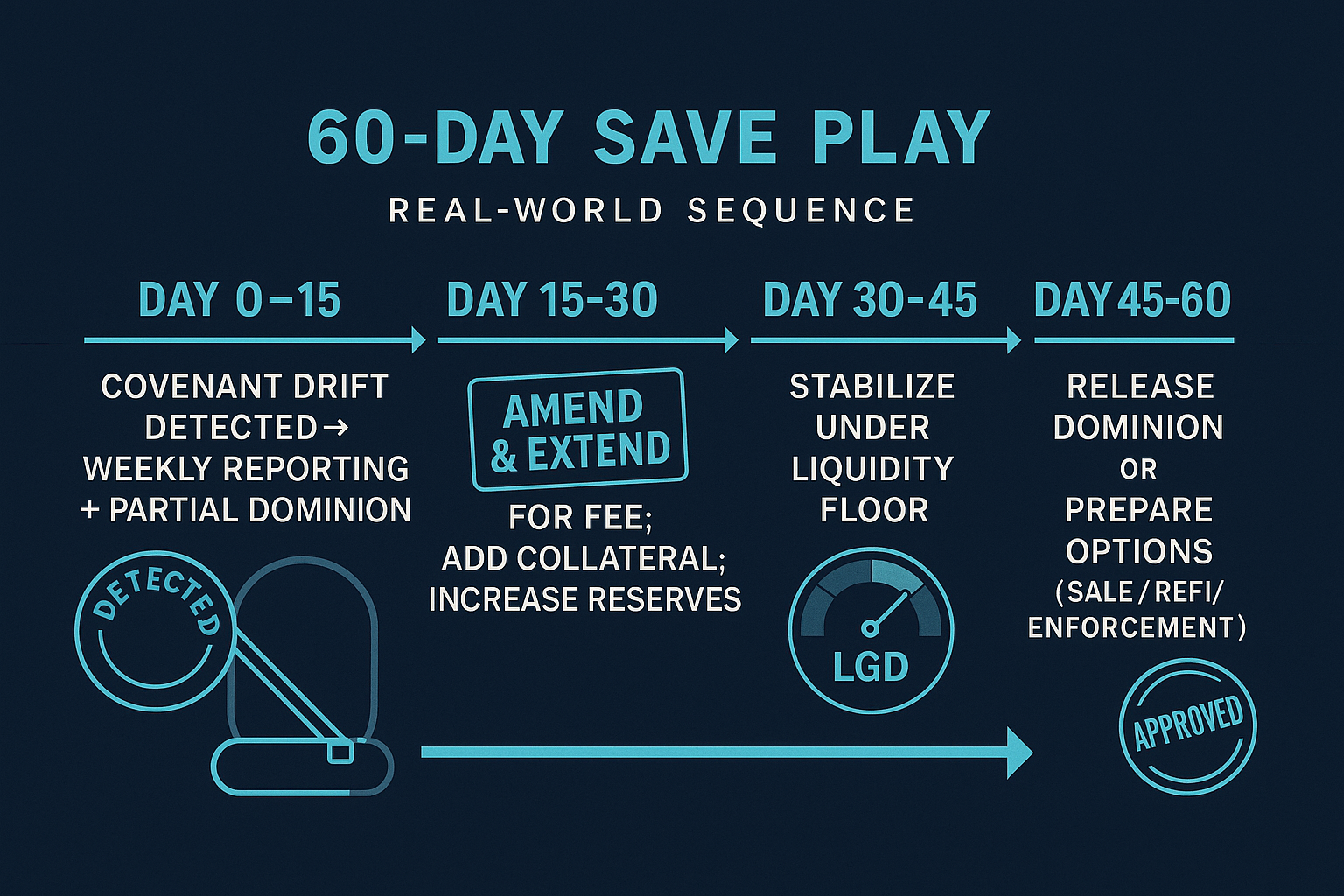

Breaches trigger discussions, fees, tighter terms—or, if needed, remedies.

- Incurrence covenants (the guardrails).

These restrict actions unless pro-formas are met: issuing more debt, paying dividends, buying back stock, or selling assets. They keep the borrower from adding risk midstream. - Information covenants (the headlights).

Frequent reporting, KPI dashboards, borrowing-base certificates, auditor letters, and notification of material events. Without timely data, lenders fly blind. - Negative covenants (the fences).

Limits on liens, affiliate transactions, asset transfers, or changes in business lines—so collateral and cash flow aren’t quietly diverted.

How to judge covenants:

Look for tight definitions (no wiggle room), short reporting lags, and springing controls—like cash dominion or blocked accounts—if covenants trip.

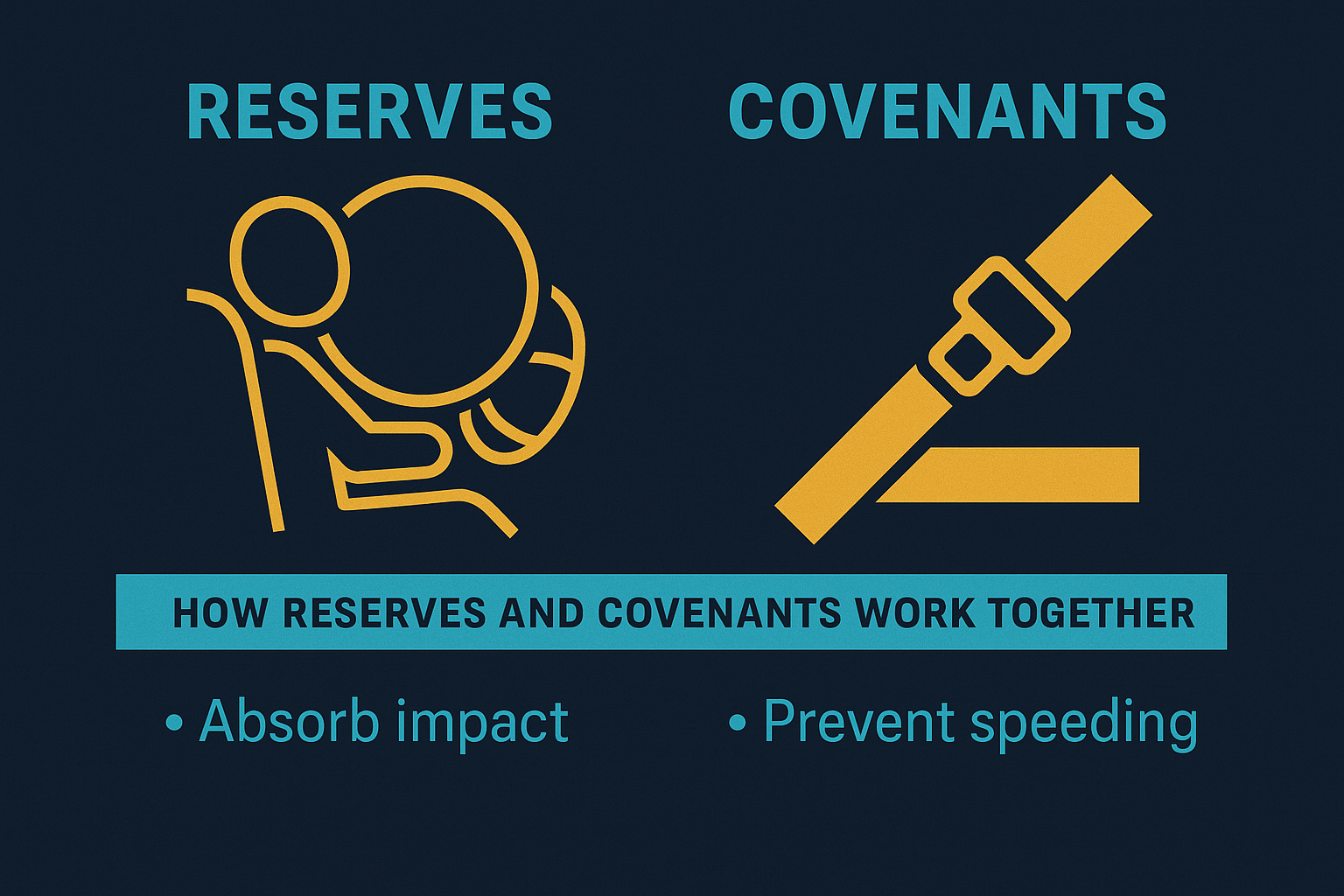

How reserves and covenants work together

Think of reserves as the airbags and covenants as the seatbelts and sensors. Reserves absorb impact; covenants prevent speeding and warn when the road gets icy.

Example: A borrower closes an acquisition and needs two quarters to integrate customers. An interest reserve pays coupons during that window. Meanwhile, maintenance covenants watch leverage and coverage. If leverage spikes or cash tightens, the lender can amend and extend—charging a fee, adding collateral, or tightening baskets—before the reserve runs dry.

Signs of strength (and weakness)

Green flags

- Reserves sized to credible stress cases with independent validation.

- Maintenance covenants that bite early (not only at year-end).

- Clear triggers for cash control and reserve releases.

- Borrowing-base rules with eligibility criteria (aging/concentration) and field exams in asset-based loans.

- A documented amendment playbook: fee step-ups, collateral adds, equity cures.

Red flags

- Covenant-lite packages—few or no maintenance tests—especially in cyclical sectors.

- Over-generous baskets for additional debt or liens that can dilute collateral.

- Reserves that are small relative to forecast volatility—or easily released on optimistic projections.

- Long reporting lags; lenders learning about problems after the quarter is over.

Questions to copy/paste for diligence

- What reserves exist, who controls them, and what release tests apply?

- Which financial covenants are tested, how often, and at what levels?

- What happens automatically (cash dominion, pricing step-ups) if a test is missed?

- How are baskets sized for additional debt, liens, dividends, and investments—and do they grow automatically?

- For ABL: What are the borrowing-base advance rates, eligibility criteria, reserves, and field-exam cadence?

- Amendment history: Show one recent amendment—what changed, what fee was charged, and how risk fell.

Bottom line

Reserves give borrowers runway; covenants give lenders control. The best managers design both to surface issues early, keep cash flowing to the right places, and earn better terms when risk rises. If a manager can show you the math behind reserve sizing and walk you through a recent covenant negotiation—with documents, not anecdotes—you’re looking at a platform that manages risk on purpose, not by luck.

{kind=link}