This Content Is Only For Subscribers

Real estate feels tangible—buildings you can touch, land you can map. But once you pool investor money to buy, finance, or develop property, you step into a world shaped by securities law, fund rules, lending covenants, tax regimes, and plain-old landlord obligations. If you’re a newer investor, this guide explains the regulatory landscape in plain English: who the referees are, how the fund structures differ, where the main “gotchas” live, and what to look for in diligence.

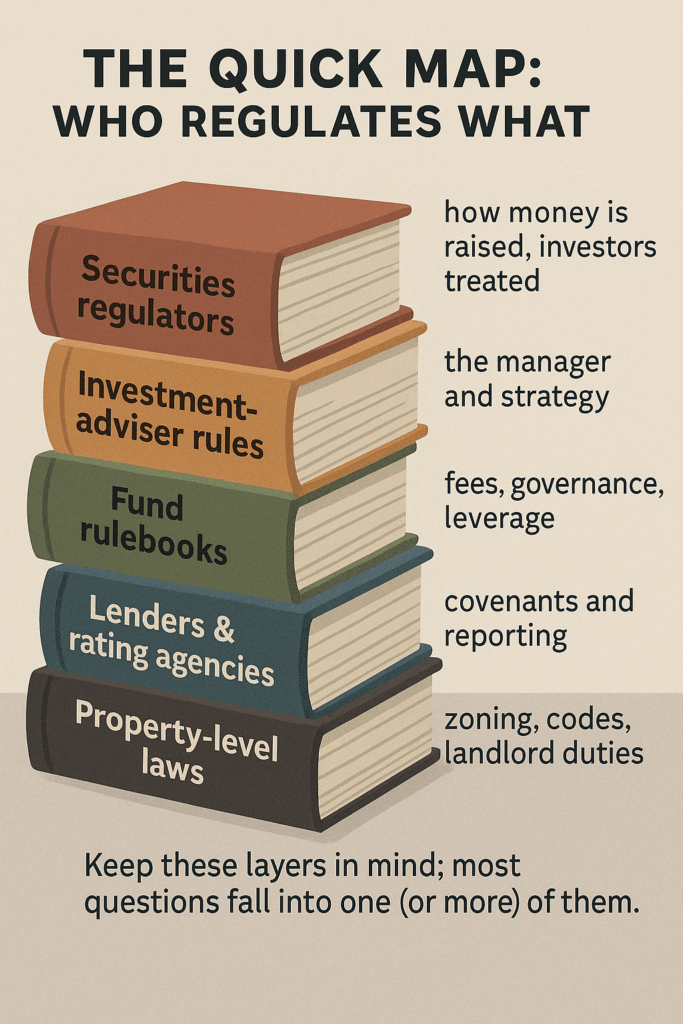

The quick map: who regulates what

- Securities regulators oversee how real estate funds raise money, market performance, and treat investors. In the U.S., that’s largely the Securities and Exchange Commission (SEC) plus state “blue-sky” authorities. Many other countries have similar securities regulators and private-offering regimes.

- Investment-adviser rules govern the manager (the firm that picks properties and runs the strategy). Rules cover fiduciary duties, advertising/marketing claims, recordkeeping, and conflicts.

- Fund rulebooks (the partnership agreement, offering memorandum, and side letters) control fees, governance, valuation, leverage, and liquidity. They’re legally binding and crucial to read.

- Lenders and rating agencies impose covenants and reporting through mortgages, credit facilities, and securitizations.

- Property-level laws—zoning, building codes, environmental rules, landlord-tenant, fair housing, accessibility—apply to the assets themselves.

- Tax authorities shape fund structures and after-tax returns (think pass-through partnerships, REIT requirements, depreciation rules, withholding for foreign investors).

Keep these layers in mind; most regulatory questions fall neatly into one (or more) of them.

What is a “real estate fund,” exactly?

“Real estate fund” is an umbrella term. Most vehicles fall into a few familiar types:

- Closed-end private equity real estate (PERE) funds buy, improve, and sell over a 7–12-year life. Strategies range from core (low leverage, stabilized, long leases) to core-plus, value-add (capex + leasing), and opportunistic (development, repositioning, higher leverage).

- Open-end core funds offer periodic subscriptions/redemptions and aim for stabilized income with moderate leverage. They use gates and queues to manage liquidity.

- Debt funds originate or purchase loans (senior, mezzanine, construction), sometimes packaging them into securitizations. They live and die by credit underwriting and borrower covenants.

- REITs (real estate investment trusts) are corporations or trusts that meet strict income/asset tests and distribution rules. Some trade publicly; others are non-traded or private. REITs have their own regulatory and tax regime distinct from private funds.

Different wrappers, same idea: a manager deploys your capital into property or loans under a set of rules.

How real estate funds raise capital (and why it matters)

Most private funds raise through private placements. Here’s what that means for you:

- Eligibility gates. Offerings typically target accredited and, for some vehicles, qualified purchaser investors. The bar you must clear depends on the fund’s structure.

- Two common routes.

- A “quiet” raise (often called 506(b) in the U.S.) that does not use public advertising; investors generally self-certify eligibility in subscription documents.

- A public-facing private raise (often 506(c)) that does allow advertising but requires the manager to take reasonable steps to verify your eligibility (documents or third-party letters; a checkbox isn’t enough).

- State notices and timing. Even when federal (or national) rules apply, managers often file state/provincial notices and pay fees where investors reside. You’ll see this referenced in the subscription packet.

Investor takeaway: Your onboarding experience—what you disclose, what the manager can say publicly—flows from the offering route they choose. Neither route changes the substance of the fund; it changes the marketing and verification process.

The manager is regulated, too (and this is good for you)

Real estate funds are run by investment advisers (or their local equivalents). Whether fully registered or operating under exemptions, good managers live by these principles:

- Fiduciary duty. Act in clients’ best interests. Disclose conflicts. Don’t mislead. In practice, that’s about fair fees, honest performance, and alignment when allocating deals or expenses.

- Compliance and records. Written policies, a real Chief Compliance Officer (CCO), and books and records that back up what’s in the deck—especially any performance claims, case studies, or “top-quartile” statements.

- Advertising/marketing rules. Testimonials, endorsements, and net vs. gross performance all come with conditions. If a slide touts a 20-year IRR, the team should be able to show the work (cash flows, methodology, benchmark).

- Custody & audits. Many pooled vehicles provide annual audited financial statements and use independent administrators for capital accounts and investor reporting. This helps catch expense mistakes and valuation drift.

Investor takeaway: Ask for the manager’s regulatory status, the last exam outcome (high-level), and one sample workpaper behind a performance slide. Calm, specific answers are a green flag.

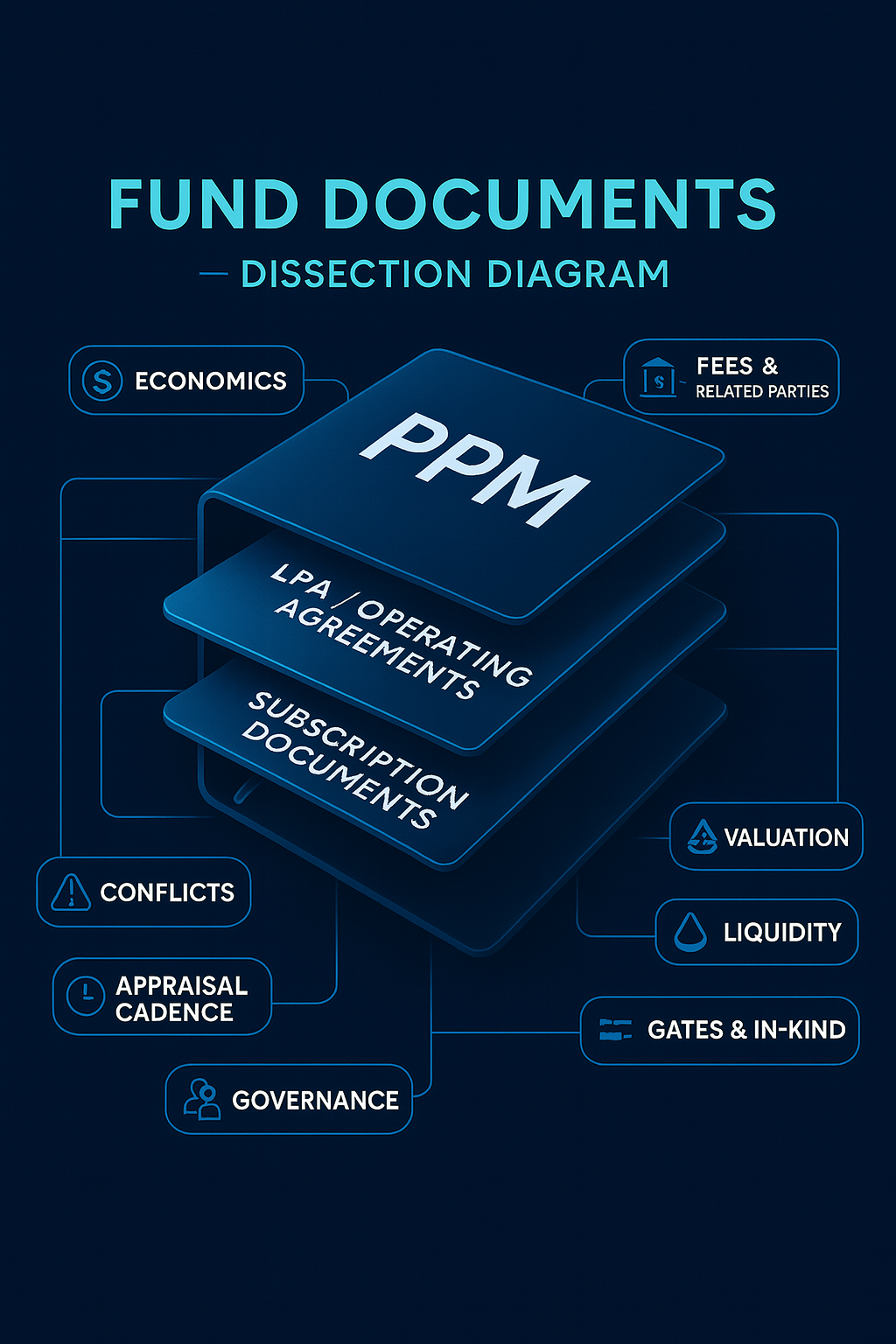

Fund documents: your real rulebook

Three documents tell you almost everything:

- Private Placement Memorandum (PPM) – strategy, risks, conflicts, and offering terms.

- Limited Partnership Agreement (LPA) or operating agreement – legally binding economics, governance, and rights.

- Subscription documents – your representations, eligibility, and tax forms.

Read them with a pencil and focus on:

- Economics. Management-fee schedule (rate, step-downs), the promote (carried interest), preferred return/hurdles, catch-up mechanics, and the waterfall (the order cash is distributed among LPs and GP).

- Fees and related parties. Beyond management fee + promote, look for acquisition/disposition fees, development or construction management fees, property-management fees, asset-management fees at the property level, and loan origination or servicing fees in debt funds. The key is who earns them, how much, and what offsets apply (e.g., property-level fees offset fund-level fees).

- Leverage policy. Maximum loan-to-value (LTV), interest-rate hedging, recourse vs. non-recourse debt, and cross-collateralization. For open-end funds, leverage bands often tie to liquidity management.

- Valuation. Appraisal frequency, who selects appraisers, and how fair value is determined for assets under development or heavy capex. Expect policies for impairments, capitalized costs, and assumptions (cap rates, rent growth, exit yields).

- Liquidity terms. Capital call timing, recycling rules, financing for late capital, gates and suspension rights in open-end funds, and in-kind distribution mechanics if the fund distributes property or loan interests.

- Conflicts & allocations. Co-investment policy, deal allocation between affiliated funds, cross-fund transactions, and any warehousing of assets pre-close. You want clarity on “who gets what” when multiple vehicles chase the same deal.

- Governance. Advisory committees (LPAC), their voting thresholds, what matters they must approve (e.g., conflicts, side pockets, valuation overrides), and information rights.

Valuation and reporting: where trust is earned (or lost)

Real estate valuation marries numbers with judgment. Strong managers show their math:

- Appraisal discipline. Independent appraisals at a set cadence (e.g., annual for closed-end funds, quarterly or rolling for open-end), plus internal reviews when major events occur (anchor tenant loss, refinancing failure, market shock).

- Key inputs. Net operating income (NOI), market rents, occupancy, cap rates/discount rates, lease rollover, and capex. Development deals need realistic hard/soft costs, contingencies, and lease-up schedules.

- Back-testing. Compare realized sale prices to prior valuations; if gaps appear, explain them and adjust methods.

- Performance presentation. Distinguish gross from net returns. Show DPI/TVPI (distributed and total value to paid-in), not just IRR. Break out attribution (income vs. appreciation vs. leverage).

- Financial statements. Annual audits, quarterly letters with asset-level KPIs, and capital account statements that tie back to the waterfall.

Investor takeaway: Ask for a recent appraisal summary, the valuation policy, and a realized-vs-valued case study from the last year.

Financing and lender oversight

Debt isn’t just a return amplifier—it’s a rule source. Loan documents often require:

- Financial covenants (DSCR, LTV tests), reserve accounts (TI/LC, capex), and cash management waterfalls.

- Reporting (rent rolls, operating statements, budgets) and consent rights (major leases, transfers, capex spend over thresholds).

- Recourse carve-outs (“bad-boy” guarantees) and completion guarantees in development.

Breaching covenants can force asset sales or capital calls at bad times. Good managers model refinancing risk and run hedging programs (rate caps/swaps) with counterparties approved by the credit facility.

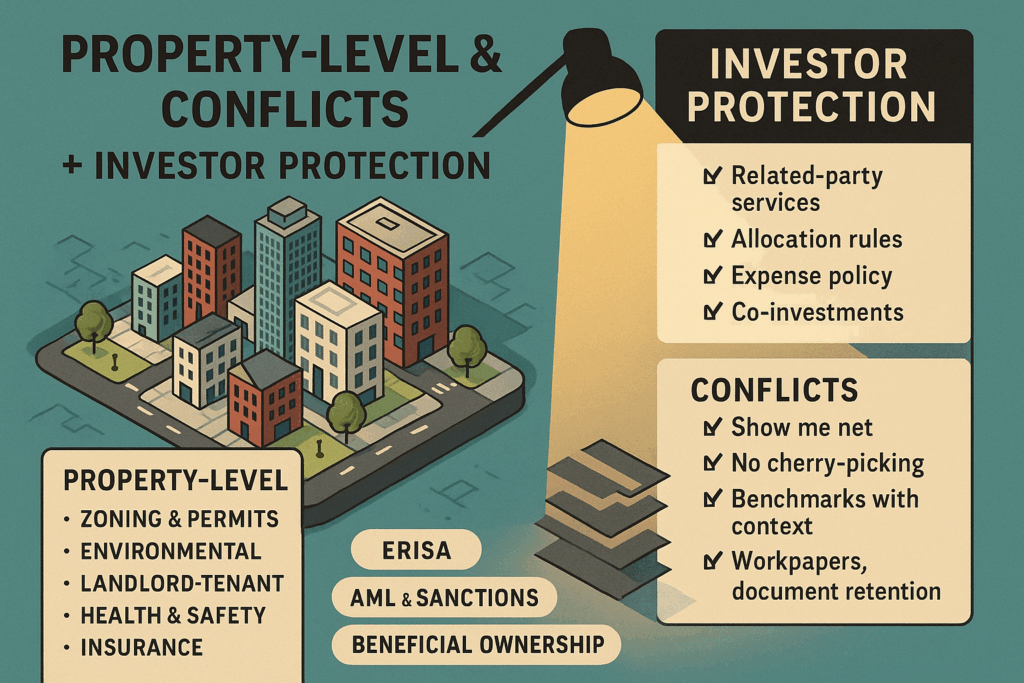

Property-level law: the ground rules that never go away

Every asset lives inside a local legal ecosystem:

- Zoning & permits. Use restrictions, density/FAR, parking, signage, historic overlays, and approval timelines. Development deals live and die here.

- Environmental. Phase I/II reports, remediation obligations, wetlands/coastal rules, asbestos/lead paint in older buildings, and stormwater requirements.

- Landlord-tenant & fair housing. Rent regulations (in some jurisdictions), eviction procedures, habitability standards, security-deposit rules, accessibility (e.g., ADA-style laws), and anti-discrimination.

- Health & safety. Fire codes, elevator inspections, emergency plans, and local occupancy requirements.

- Insurance. Property, liability, flood, wind, builder’s risk—plus business interruption for operating assets.

A fund can be perfectly compliant at the securities level and still get hurt by property-level mistakes. In diligence, ask how the manager tracks local compliance across the portfolio.

Conflicts of interest: where regulators—and LPs—focus

Real estate invites conflicts because managers often wear multiple hats: fund GP, property manager, developer, broker, leasing agent, construction manager, or loan servicer. That’s not inherently bad; it just needs daylight and discipline.

- Disclose and offset. If an affiliate is the property manager, is the fee market-based? Does it offset the asset-management fee? Are leasing/brokerage commissions capped or pre-approved by the LPAC?

- Allocation rules. When two funds could buy the same deal, what determines allocation? Is there a rotation or a priority based on mandate fit?

- Expense policy. Which costs are fund-level vs. manager-level (e.g., travel, research, deal sourcing)? Regulators and LPACs scrutinize “who pays for what.”

- Co-investments. How are they offered and allocated? Can co-investors leapfrog the main fund’s pro-rata rights?

You’re looking for clear rules + evidence of compliance (committee minutes, approvals, and audit trails).

Investor protection: marketing claims and recordkeeping

Modern advertising standards allow testimonials and third-party ratings in some jurisdictions—but with conditions (disclosures, substantiation, and records). Performance must be fair and balanced, with the underlying workpapers available. A few practical rules of thumb:

- “Show me net.” Always ask for net returns after all fees/expenses and carried interest.

- Don’t cherry-pick. Full-fund or full-composite results, with the treatment of realized vs. unrealized assets spelled out.

- Benchmarks with context. Real estate has multiple indices (by property type, geography, open-end vs. closed-end). Ensure the benchmark fits the strategy and vintage.

- Document retention. If the slide exists, the backup should too: appraisals, cash-flow models, sale docs, and fee calculations.

ERISA and plan-asset considerations (if pensions invest)

When retirement plans invest, plan-asset rules and fiduciary duties come into play. Funds either:

- Keep below certain ownership thresholds, or

- Qualify for exceptions (e.g., “real estate operating company” (REOC) or “venture capital operating company” (VCOC) tests in some regimes), or

- Structure governance to manage plan-asset implications.

The goal is to avoid turning the fund manager into a fiduciary for the plan’s assets beyond the agreed scope, or to manage that status knowingly. If your dollars come from pensions, ask how the fund handles plan-asset status and reporting.

Anti-money-laundering (AML), sanctions, and beneficial ownership

Regulators increasingly look at who is behind the money and the property:

- KYC/AML onboarding. Collecting documents, screening investors and counterparties, and understanding the source of funds.

- Sanctions screening. Ensuring no sanctioned person or entity is in the chain, including tenants and vendors where applicable.

- Beneficial-ownership reporting. Some jurisdictions require companies and trusts to report ultimate owners; real estate often has special rules for high-risk markets or cash purchases.

Good practice includes risk scoring counterparties, documenting overrides, and refreshing checks periodically—not just at subscription.

Tax frameworks: the parts investors actually feel

You don’t need to be a tax pro, but know the basics:

- Pass-through funds. Many private funds are taxed as partnerships; income, losses, depreciation, and gains pass through to you. Expect a K-1 and possibly state filings if the portfolio spans multiple states.

- Depreciation. Real estate offers sizable depreciation that can shelter income; cost segregation schedules are common. Depreciation recapture can claw back some benefits on exit.

- REITs. To qualify, a REIT must meet asset and income tests and distribute most taxable income. REIT dividends have unique tax treatment; some components may be ordinary, qualified, or capital gain.

- Foreign investors. Many countries impose withholding or gains taxes on real estate. Inbound/outbound investments may use blockers to manage tax exposure and treaties.

- Debt funds. Interest income is typically ordinary; watch for withholding and portfolio interest exceptions for non-resident investors.

Ask the manager what forms you’ll receive (K-1, 1099, local equivalents), when they arrive, and how they categorize income.

Cross-border investing adds another layer

Buying in a different country (or taking money from investors abroad) introduces:

- Marketing permissions. You can’t assume a fund authorized in one country can market in another without notices or approvals.

- Foreign-investment screening. Many countries review foreign ownership of sensitive land or critical-infrastructure-adjacent property.

- Currency and capital controls. Hedging programs, repatriation timelines, and local banking rules matter in volatile FX environments.

- Data and privacy. Tenant data, property-management systems, and cross-border reporting need privacy compliance.

A global strategy works best with a jurisdiction matrix: where the manager can market, file, buy, borrow, and hedge—and what could slow those activities.

Practical diligence: questions to copy/paste

Structure & governance

- What’s the vehicle type (closed-end, open-end, debt, REIT)? Term? Extensions?

- Fee stack in numbers: management fee, property-level fees, promote, catch-up, offsets.

- Who sits on the LPAC? What decisions need LPAC consent?

Valuation & reporting

4) Appraisal cadence and who appoints appraisers? One recent example with key assumptions.

5) How are development deals valued pre-stabilization?

6) Quarterly package sample: financials, KPI dashboard, and capital-account statement.

Leverage & liquidity

7) Leverage limits and hedging policies. What happens if covenants trip?

8) Open-end only: gates, queues, and suspensions—how often have you used them?

Conflicts & expenses

9) Related-party services (property management, brokerage, construction). Offsets or caps?

10) Expense policy: what’s fund-borne vs. manager-borne? One example of a rejected charge.

ESG & compliance

11) Environmental risk management: who owns it, and what’s your remediation playbook?

12) Fair-housing and accessibility compliance for resi; data-privacy for tenant systems.

13) AML/sanctions toolkit: screening vendor and refresh cadence.

Track record

14) Realized DPI and TVPI by vintage; loss ratio; two case studies (one win, one loss) with lessons.

Red flags (and green lights)

Red flags

- Fees beyond the PPM (surprise “admin” charges, ambiguous pass-throughs).

- Performance shown gross only, or selective asset “wins” with no full-fund view.

- Thin appraisal support or no back-testing against sales.

- Heavy related-party fees with weak offsets or approvals.

- “We’ve never had a covenant issue” without proof of stress testing.

Green lights

- Clear fee math on a numerical example (e.g., a $10M sale with promote outcomes).

- Independent appraisals, valuation committee minutes, and variance explanations.

- LPAC minutes available (with redactions) and a record of pushing back on conflicts.

- Realistic hedging and refinancing plans; covenant dashboards in quarterly letters.

- Timely audits and tax packages with state filing guidance.

Bottom line

Real estate funds aren’t a regulatory black box—they’re a stack of predictable rule sets layered on top of each other: securities rules for how money is raised and managers behave, fund documents for economics and governance, lender covenants for leverage discipline, property law for day-to-day operations, and tax rules for how your returns arrive.

As an investor, you don’t need to memorize statutes. You do need to:

- Read for consistency (deck ↔ PPM ↔ LPA ↔ reports).

- Demand net performance with clear appraisal and valuation methods.

- Understand the fee stack and where conflicts can appear—and how they’re mitigated.

- Know the leverage and refinancing plan, not just the target IRR.

- Verify compliance scaffolding (audits, AML/sanctions, property-level obligations).

Do that, and the regulatory terrain becomes an advantage, not a barrier. It helps you separate polished marketing from durable operations—so your real estate allocation does what it should: deliver income and appreciation with risks you actually recognize.

{kind=link}