Venture capital (VC) occupies a unique corner of the financial world. To some, it looks glamorous—Silicon Valley billionaires, unicorn startups, and fortunes built overnight. To others, it looks like reckless gambling—throwing money at risky ideas with little chance of success. The truth lies somewhere in between: venture capital is an extreme version of the risk-return tradeoff.

Most investments fail. A few succeed beyond anyone’s imagination. And the handful of winners not only drive profits for investors—they reshape industries and societies. To understand VC is to understand this balance between risk, patience, and asymmetric payoff.

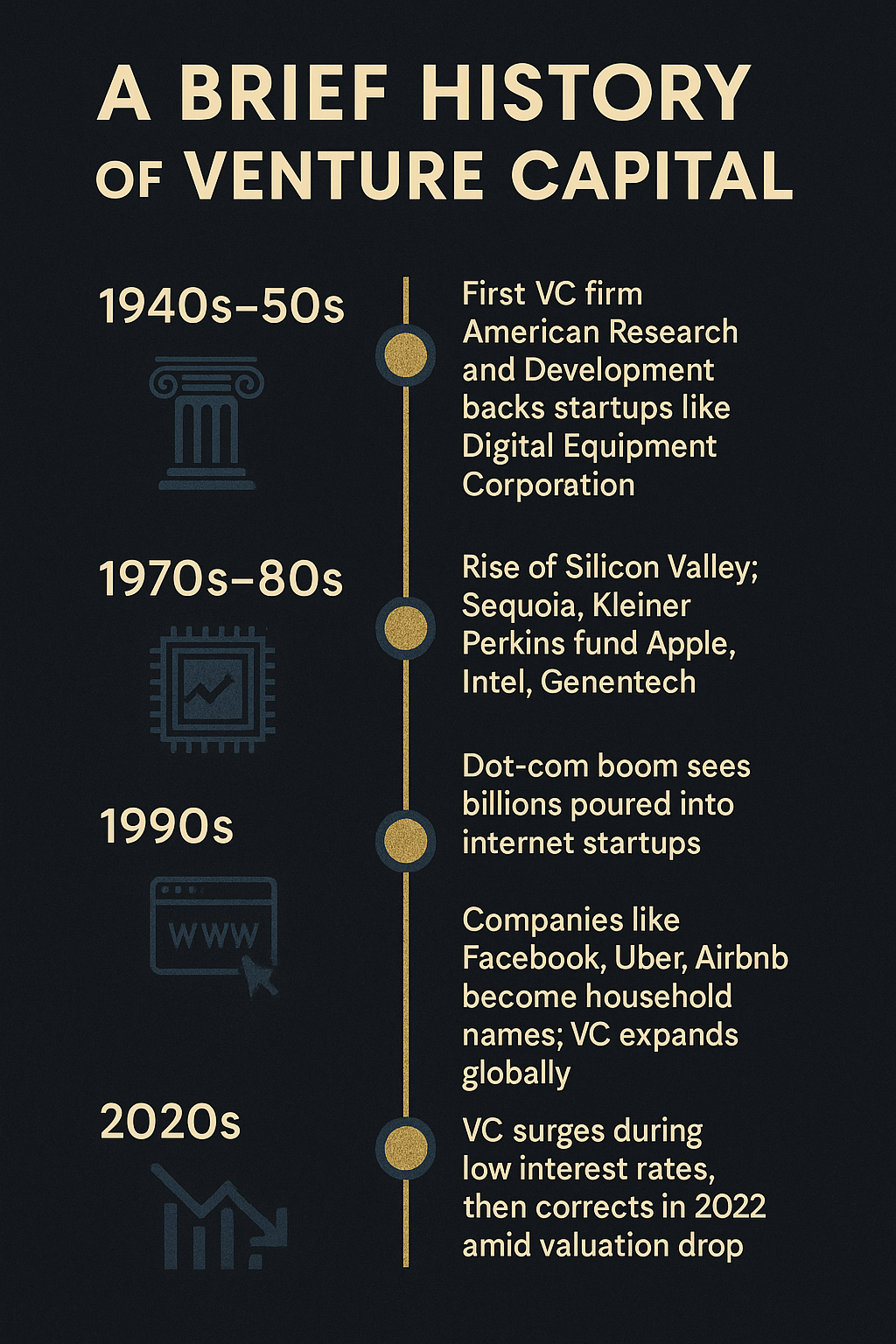

A Brief History of Venture Capital

Though venture capital seems modern, its roots go back decades.

- 1940s–50s: The first VC firm, American Research and Development (ARD), backed companies like Digital Equipment Corporation. This was the first time institutional money flowed into startups.

- 1970s–80s: The rise of Silicon Valley, fueled by VC firms like Sequoia and Kleiner Perkins, which funded Apple, Intel, and Genentech.

- 1990s dot-com boom: Billions poured into internet startups; many failed, but survivors like Amazon, Google, and eBay transformed the economy.

- 2000s–2010s: Venture-backed companies like Facebook, Uber, and Airbnb became household names. VC expanded globally, with China, India, and Europe building vibrant ecosystems.

- 2020s: Venture capital surged during low interest rate years, then faced a correction in 2022 as markets tightened and valuations dropped.

This historical arc shows a pattern: VC thrives in times of optimism and cheap capital, but busts remind everyone how risky it is.

The Risk-Return Shape: The Power Law

In most investing—say, the stock market—returns follow a bell curve. You might expect a range of outcomes, but the average matters. In venture capital, the average is meaningless. Returns follow a power law:

- Roughly two-thirds of startups fail and return nothing.

- Another 20–30% return only the capital invested.

- The top 5–10% of startups generate the majority of all returns.

This creates an industry obsessed with finding the outlier. A single company—Google, Facebook, or Airbnb—can make an entire fund successful.

Why the power law matters

- VCs can’t afford to play it safe. Safe bets rarely return enough.

- This drives the focus on massive markets. Only big opportunities can generate the exponential outcomes needed.

- It explains the culture of Silicon Valley: risk-taking, big visions, and tolerance for failure.

Case Studies: Home Runs and Strikeouts

The Winners

- Google (1999): Sequoia and Kleiner Perkins invested $25M. By IPO in 2004, those stakes were worth billions.

- Facebook (2005): Accel’s $12.7M check turned into billions at IPO in 2012.

- Zoom (2011): Sequoia backed an “uncool” video conferencing startup. In 2020, its IPO and pandemic-driven adoption made it one of the firm’s best-ever returns.

- Airbnb (2009): Initially mocked, it grew into a global travel company. Sequoia’s early investment paid off more than 1,000x.

The Failures

- Webvan: Raised $800M to deliver groceries in the 1990s. Bankrupt in 2001.

- Theranos: Raised $700M on faulty blood-testing tech. Imploded in fraud.

- Quibi: Raised $1.75B for mobile video, shut down in 6 months.

- Jawbone: Once valued at billions, collapsed after losing to Fitbit and Apple.

These extremes show VC’s reality: most fail, but the rare wins are spectacular.

The Mechanics of a VC Fund

VC funds aren’t just pools of cash. They’re structured businesses.

- Fund size: Can range from $50M seed funds to $10B mega-funds.

- Limited Partners (LPs): Institutions (pensions, endowments) supply most of the money.

- General Partners (GPs): The venture capitalists who manage the fund and make investments.

Fees and Carried Interest

- 2% management fee: Annual fee on committed capital, covering salaries and operations.

- 20% carry: VCs keep 20% of profits above what was returned to LPs.

Example: A $500M fund invests $20M in a startup. That startup exits for $400M. After returning $20M plus profits to LPs, the firm keeps $76M as carry.

This structure incentivizes VCs to chase big outcomes, since modest wins barely move the needle.

The Risk Side in Detail

Why do most startups fail?

- Market risk: Sometimes there’s simply no demand.

- Execution risk: Great ideas fall apart due to poor management or inability to scale.

- Financing risk: Startups need constant capital infusions. If markets dry up, they collapse.

- Competitive risk: Hot markets attract multiple players; only a few survive.

Managing Failure

VCs expect failure. They know that 7 out of 10 startups may go under. They manage this by:

- Diversifying portfolios across 20–40 startups.

- Reserving capital for “winners” in later rounds.

- Cutting losses early. If a startup stalls, they stop funding.

This discipline is what separates seasoned VCs from amateurs who chase sunk costs.

The Return Side: Why LPs Invest

Why would an endowment or pension put money into such a risky asset?

- Asymmetric returns: The upside is huge if you’re in the right fund.

- Access to innovation: Institutions want exposure to frontier tech.

- Diversification: VC returns don’t perfectly track public markets.

The Yale Endowment Model is the classic case. Under David Swensen, Yale allocated heavily to VC and alternative assets, reaping outsize returns compared to peers.

Time Horizons and Illiquidity

Venture capital is a long game:

- 10+ year fund life. Investors commit for a decade.

- 7–10 years to exit. Startups take time to grow.

- Illiquid stakes. You can’t just sell shares on a public exchange.

This is why VC is reserved for institutions with patient capital.

Stages of VC Risk and Return

- Seed stage: Idea only, highest risk, but lowest entry valuations.

- Series A/B: Early traction, still risky, but higher survival odds.

- Growth stage: Scaling, preparing for IPO, lower multiples but safer.

VCs often blend these stages across their portfolios to balance risk.

Global Venture Capital

VC is now global:

- United States: Still dominant in unicorn creation.

- China: Explosive growth in the 2010s (Alibaba, Didi, Bytedance). Regulatory crackdowns have cooled it.

- Europe: Spotify, Klarna, Revolut show Europe’s rise.

- India: Flipkart, Paytm, and growing fintech/ecosystem activity.

- Southeast Asia: Grab and GoTo are regional champions.

- Africa: Early but promising—fintech (Flutterwave, Chipper Cash) leads.

Each region faces unique risks: regulatory shifts in China, fragmented markets in Europe, infrastructure gaps in Africa.

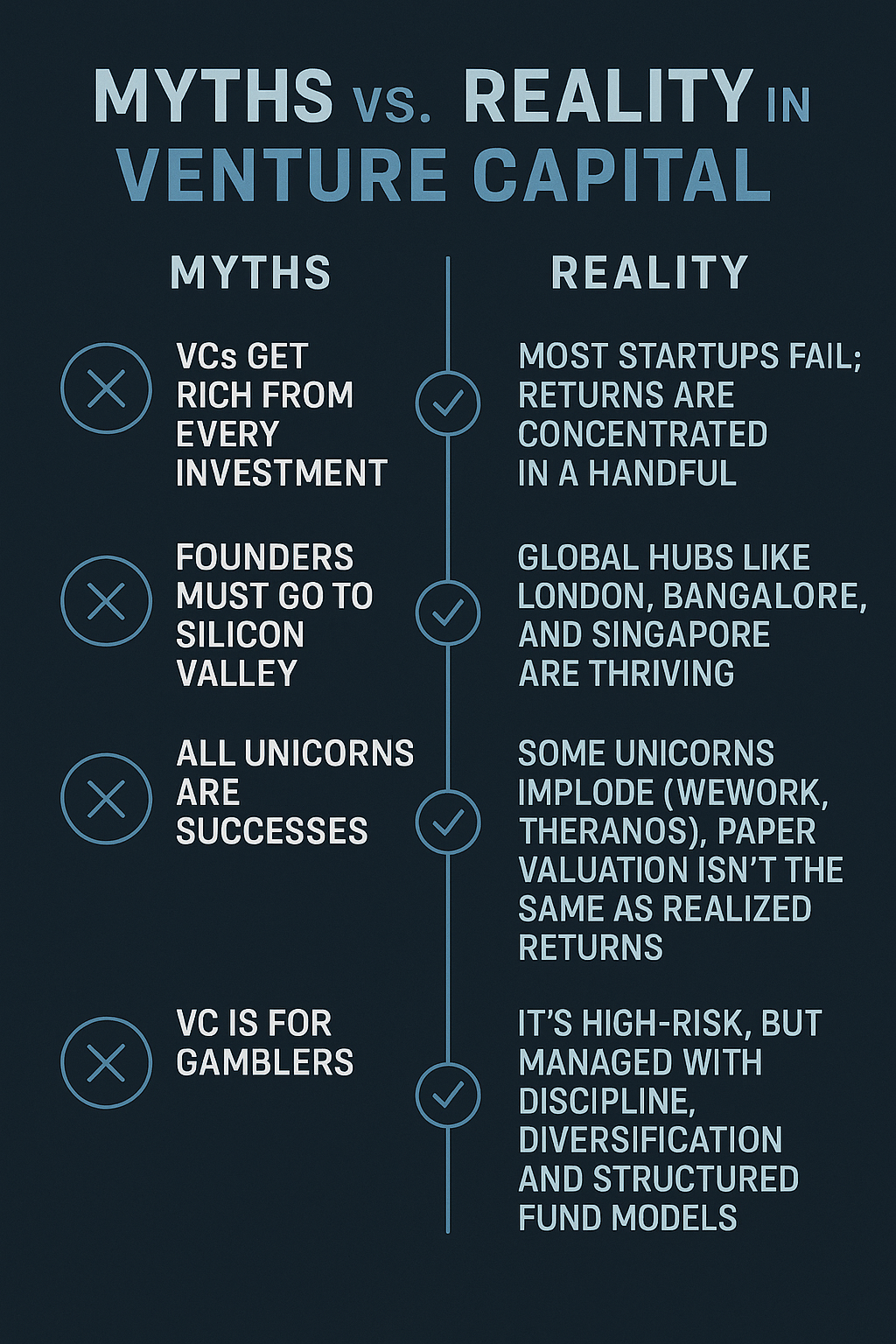

Myths vs. Reality in Venture Capital

- Myth: VCs get rich from every investment.

Reality: Most startups fail; returns are concentrated in a handful. - Myth: Founders must go to Silicon Valley.

Reality: Global hubs like London, Bangalore, and Singapore are thriving. - Myth: All unicorns are successes.

Reality: Some unicorns implode (WeWork, Theranos). Paper valuation isn’t the same as realized returns. - Myth: VC is for gamblers.

Reality: It’s high-risk, but managed with discipline, diversification, and structured fund models.

VC vs. Other Asset Classes

- Public equities: 8–10% long-term returns, liquid, lower risk.

- Private equity buyouts: 12–15% returns, stable cash-flow businesses.

- Real estate: 6–10% steady, asset-backed.

- Venture capital: Median funds underperform, but top quartile deliver 20–30% IRR.

This shows why VC is a satellite allocation, not a portfolio core.

Behavioral Dynamics

Venture capital is as much psychology as finance:

- Optimism bias: Founders and VCs overestimate success.

- Herd behavior: Everyone piles into hot trends (crypto, AI, social apps).

- Narratives over numbers: Early-stage investing relies heavily on belief.

For individuals, the lesson is caution: don’t let hype or herd mentality drive your choices.

VC’s Impact on the World

Venture capital has fueled the rise of industries:

- Personal computing (Apple, Intel).

- Biotech (Genentech, Moderna).

- Internet platforms (Google, Facebook).

- Mobility (Uber, Tesla).

Beyond returns, VC creates jobs, drives innovation, and shapes entire economies.

Lessons for Novice Investors

- Diversify. Don’t rely on one bet.

- Budget for failure. Losses are part of the model.

- Think long-term. Great outcomes take time.

- Avoid hype. Remember Theranos and Quibi.

- Seek asymmetric upside. Favor opportunities where potential reward dwarfs risk.

- Stay disciplined. Like VCs, cut losers quickly.

- Understand liquidity. Don’t lock up money you need soon.

- Know the manager matters. In VC, top-quartile funds dominate performance.

Closing Thoughts

The risk-return profile of venture capital is unlike any other asset class. It is risky, illiquid, and uneven. Most startups fail, but the rare successes can be life-changing—for investors and for society.

For individuals, the bigger lesson is timeless: the greatest rewards often come from tolerating uncertainty, playing the long game, and balancing boldness with discipline.

When venture capital works, it doesn’t just generate wealth—it shapes the future.

{kind=link}