This Content Is Only For Subscribers

If there’s one story that turned private equity from an insider’s game into front-page drama, it’s the 1988 takeover of RJR Nabisco. The deal—led by Kohlberg Kravis Roberts (KKR)—wasn’t just big; it was a cultural moment. It defined an era of leveraged buyouts (LBOs), spawned a best-selling book, and shaped public perception of Wall Street for decades.

For beginners, the RJR Nabisco saga is more than financial folklore. It’s a case study in how bidding wars can inflate prices, how leverage can both empower and endanger, and how management incentives can collide with shareholder interests. Let’s unpack what happened, why it mattered, and what a modern investor can learn from it.

The Company Behind the Headlines

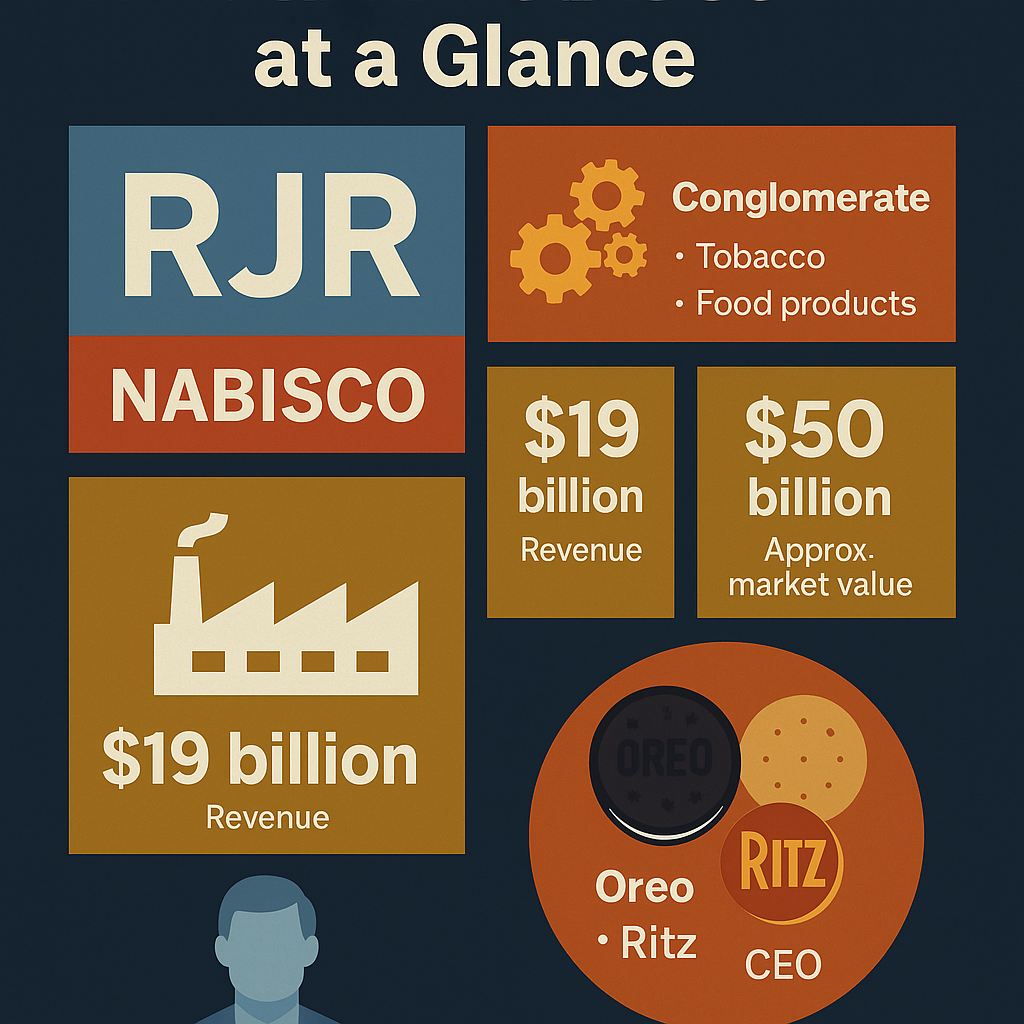

RJR Nabisco was a conglomerate—a mashup of RJR (a tobacco company behind brands like Camel and Winston) and Nabisco (a food giant known for Oreo, Ritz, and other household staples). The business had valuable assets and steady cash flow, but like many conglomerates of the era, it was seen as complex and inefficient. Investors suspected that under the right ownership—and with a tighter focus—it could be worth more than the public market was assigning.

At the center was CEO F. Ross Johnson, a charismatic leader who believed the company was undervalued. His solution was bold: take RJR Nabisco private in a management-led buyout (MBO). The pitch was that management, freed from the quarterly pressure of public markets, could make long-term decisions and unlock value.

The Spark That Lit the Bidding War

Once Johnson’s MBO proposal became public, it set off a feeding frenzy. Private equity firms, including KKR, saw an opportunity. If the business was truly undervalued, a financial sponsor might be able to pay shareholders a premium, restructure the company, and still make a profit over time.

What followed was a high-stakes bidding war. Each round of offers ratcheted up the price, as rival camps sought to outbid one another. For shareholders, this was great in the short term—offers kept climbing. For the eventual buyer, the rising price was dangerous. Private equity returns depend on buying at a sensible price, improving operations, and exiting at a higher valuation. Overpay on day one and the math gets tough.

Leverage: Superpower or Kryptonite?

The RJR Nabisco deal became famous as a leveraged buyout—meaning the acquirer used a significant amount of borrowed money (debt) alongside investor equity to fund the purchase. Debt magnifies outcomes. If the company grows and generates cash, the equity holders can earn outsized returns once the debt is paid down. But if growth stalls or conditions deteriorate, that same debt becomes a millstone.

For RJR Nabisco, the final price tag—about $25 billion, the largest LBO of its time—left the company with a heavy debt burden. Even with dependable brands, servicing that debt would require disciplined execution, cost control, and a fair amount of luck.

Why the Deal Became a Cultural Touchstone

Two things made RJR Nabisco legendary beyond finance circles:

- The personalities. Executives, bankers, and buyout titans were cast like characters in a movie. The story had ambition, rivalry, and jaw-dropping sums of money—irresistible to the public.

- The narrative. The book Barbarians at the Gate etched the image of private equity as aggressive raiders. It captured the anxiety of the era: Were LBOs productive capitalism—or just clever financial engineering that saddled companies with dangerous debt?

The reality, as usual, was more nuanced. Buyouts can create value through focus and operational improvement. They can also destroy value if the price is too high or the debt too heavy.

Aftermath: Lessons from the Numbers

In the years after the takeover, RJR Nabisco’s debt load constrained flexibility. Servicing interest limited the company’s ability to invest freely, and asset sales followed. Over time, parts of the business were separated or sold, and the once-sprawling conglomerate was reshaped. The episode didn’t end in a dramatic collapse, but it didn’t deliver a fairy-tale outcome either. It was messy, complicated—and educational.

The key economic lesson is simple: price matters. Even a high-quality company can become a poor investment if bought too expensively. And leverage, while powerful, reduces margin for error.

What Novice Investors Can Learn

You don’t need to run a buyout fund to benefit from RJR Nabisco’s lessons. Here are practical takeaways you can use today:

- Don’t chase bidding wars—of any kind. Whether it’s a hot stock, a house in a frenzied market, or a trendy collectible, competitive bidding can push prices beyond intrinsic value. Winning the auction can mean overpaying.

- Debt is a tool, not a plan. Borrowing can speed up progress—think of a modest mortgage on a home or a carefully used business loan. But too much debt turns normal bumps into crises. Ask, “What if things go mildly wrong?” If the answer is “I’d be forced to sell at the worst time,” the leverage is too high.

- Management incentives matter. In an MBO, managers are effectively on both sides of the table—as buyers and as stewards of the seller. That’s why boards form independent committees, hire advisors, and run auction processes to protect shareholders. As a public-market investor, pay attention to incentives: executive compensation plans, insider ownership, and governance can meaningfully affect outcomes.

- Quality is not a free pass. Great brands and cash flow can support debt—but they don’t immunize a company from overpaying or mis-executing. Always ask what’s being paid today for tomorrow’s potential.

- Narratives can mislead. The “barbarians” storyline made for gripping reading, but investing rewards math and discipline, not bravado. Try to separate story from numbers.

Why the Deal Still Matters

RJR Nabisco crystallized the debate around private equity: value creation vs. value extraction. On one hand, buyouts can bring focus, reduce waste, and align owners with outcomes. On the other, heavy debt and aggressive financial engineering can stress companies and stakeholders. The truth isn’t binary. It depends on entry price, capital structure, and operational execution.

For modern investors, the enduring relevance is in process:

- Diligence: Understand what you’re buying and why it’s mispriced.

- Discipline: Set guardrails—on price, position size, and risk—and respect them.

- Duration: Give improvements time to work; don’t demand instant payoff from long-term plans.

A Simple Mental Model

When evaluating any investment—be it a blue-chip stock or a private business—try the RJR Nabisco checklist:

- Price vs. value: If competition pushes the price up, does the future still justify it?

- Leverage tolerance: Could the cash flows comfortably cover debt in a “normal bad year”?

- Execution path: What specific changes unlock value (costs, growth, focus)?

- Incentives: Do leaders win alongside you—or regardless of what happens?

If you can’t answer these clearly, the safest move might be to pass—or at least size the bet conservatively.

Final Thoughts

The KKR–RJR Nabisco buyout isn’t just an artifact from the 1980s. It’s a timeless reminder that discipline beats drama. Prices matter. Debt is powerful—and perilous. Incentives drive behavior. And stories, no matter how compelling, don’t repay loans.

For novice investors, the takeaway is refreshingly down-to-earth: Build a process you trust, avoid bidding frenzies, respect leverage, and let the numbers—not the noise—guide your decisions.

{kind=link}