This Content Is Only For Subscribers

In the years since the global financial crisis, one of the most remarkable shifts in finance has been the rise of private credit. Once a small, specialized corner of the alternative investment world, it has grown into a trillion-dollar market, rivaling traditional high-yield bonds and syndicated loans.

How did private credit get here? The story is one of regulation, opportunity, investor appetite, and innovation. Understanding that history helps investors see where the market might go next.

The World Before 2008

Before the financial crisis, corporate lending—especially for mid-sized or leveraged companies—was dominated by banks and the public markets. Companies seeking debt financing often went to:

- Commercial banks, which provided syndicated loans.

- Bond markets, where high-yield debt was sold to institutional investors.

- Mezzanine lenders, usually niche players offering subordinated debt for buyouts.

Private credit did exist, but it was small and fragmented. Specialized mezzanine funds and insurance companies participated, but most companies still relied on banks for their core financing.

The 2008 Global Financial Crisis

The collapse of Lehman Brothers, the subprime mortgage meltdown, and the ensuing credit crunch reshaped global finance. Banks were hit with losses, liquidity dried up, and regulators scrambled to stabilize the system.

For corporate borrowers, especially those below investment grade, the result was clear: bank lending dried up.Companies that had once relied on bank syndicates suddenly found the doors closed.

At the same time, regulators introduced sweeping reforms:

- Basel III (international): Higher capital requirements for banks, making risky loans more expensive to hold.

- Dodd-Frank (U.S.): Tighter oversight of bank activities and leverage.

These changes limited banks’ ability (and willingness) to lend aggressively, particularly to mid-market companies and leveraged buyouts.

Private Credit Steps In

Into that gap stepped private funds. Private equity firms, hedge funds, and independent managers saw the opportunity to lend directly to companies. Investors—hungry for yield in a world of near-zero interest rates—poured capital into these strategies.

Direct lending became the flagship product. Instead of waiting for banks to organize syndicated loans, companies could borrow directly from funds. The benefits:

- Faster execution.

- More flexible structures.

- Confidential, negotiated terms.

For lenders, the appeal was simple: attractive yields (6–10%+), floating-rate income, and diversification away from public bonds.

The 2010s: A Decade of Expansion

Through the 2010s, private credit expanded rapidly:

- AUM growth: From under $300 billion in 2010 to more than $800 billion by 2018.

- Institutionalization: Large pensions and endowments began allocating systematically to private credit.

- New strategies: Beyond direct lending, funds moved into distressed debt, specialty finance, and structured solutions.

- Private equity synergy: PE firms built captive credit arms, financing their own buyouts and deals.

By the late 2010s, private credit was no longer an experiment—it was a permanent fixture of global capital markets.

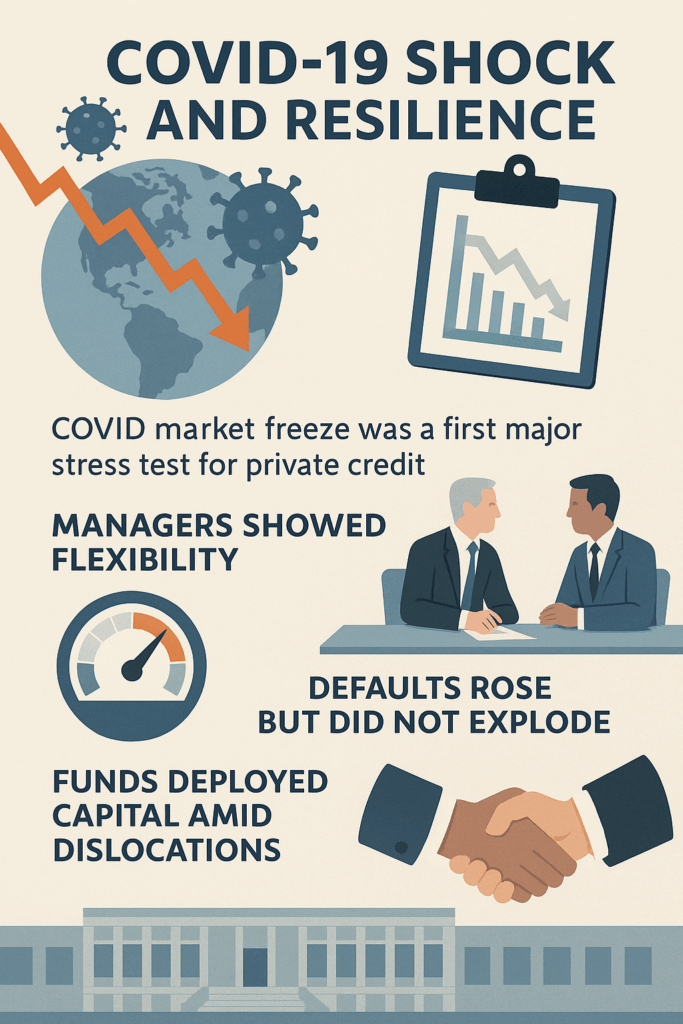

The COVID-19 Shock (2020)

The pandemic created the first major stress test for private credit at scale. In early 2020, markets froze and borrowers faced cash-flow collapses. For a moment, some feared widespread defaults.

Instead, private credit proved resilient:

- Managers worked directly with borrowers to amend terms.

- Defaults rose but did not explode.

- Many funds took advantage of market dislocation to deploy capital at attractive terms.

The lesson: private credit, though illiquid, could provide stability in turbulent times.

The 2022–2023 Rate Hike Cycle

The next big test came with the fastest interest-rate hikes in decades. For private credit, floating-rate loans became more profitable—yields jumped into double digits.

But not all was smooth sailing:

- Borrower stress: Higher debt costs strained weaker companies.

- Selective defaults: Some highly leveraged borrowers struggled to refinance.

- Fundraising divergence: Top-tier managers thrived, while smaller funds found raising capital more difficult.

Despite the challenges, investor demand remained strong. Many institutions saw private credit as one of the few places to earn attractive yields without taking equity risk.

Structural Shifts Since 2008

Several long-term shifts have defined private credit’s rise:

- Disintermediation of banks: Non-bank lenders now finance deals once handled by bank syndicates.

- Institutional mainstreaming: Pensions, insurers, and sovereign wealth funds allocate billions to the asset class.

- Mega-managers dominate: Firms like Ares, Apollo, and Blackstone manage multi-billion-dollar platforms, while boutiques carve out niches.

- Global spread: Europe has embraced private credit as banks pulled back; Asia is emerging as the next frontier.

- Product innovation: From unitranche loans to NAV-based lending and evergreen retail funds, the menu has expanded.

Opportunities and Risks Today

The evolution of private credit since 2008 has created both opportunities and new challenges:

- Opportunities:

- Attractive yields versus traditional fixed income.

- Direct exposure to corporate growth.

- Diversification across geographies and strategies.

- Risks:

- Crowding as more capital chases similar deals.

- Illiquidity (funds lock up capital for years).

- Uncertainty about how the market performs in a deep, prolonged recession.

- Regulatory scrutiny as the asset class grows.

Looking Ahead

Private credit has come a long way in just over a decade. From a niche post-crisis solution, it has matured into a global asset class, integral to corporate finance and institutional portfolios.

The key question for investors now is how the next chapter unfolds. Will private credit weather economic cycles as smoothly as it did COVID-19? Will regulation tighten? Will growth in Europe and Asia rival the U.S.?

What’s certain is that private credit has moved from the margins to the mainstream. Its story since 2008 is a case study in how crises reshape markets—and how investors adapt.

{kind=link}