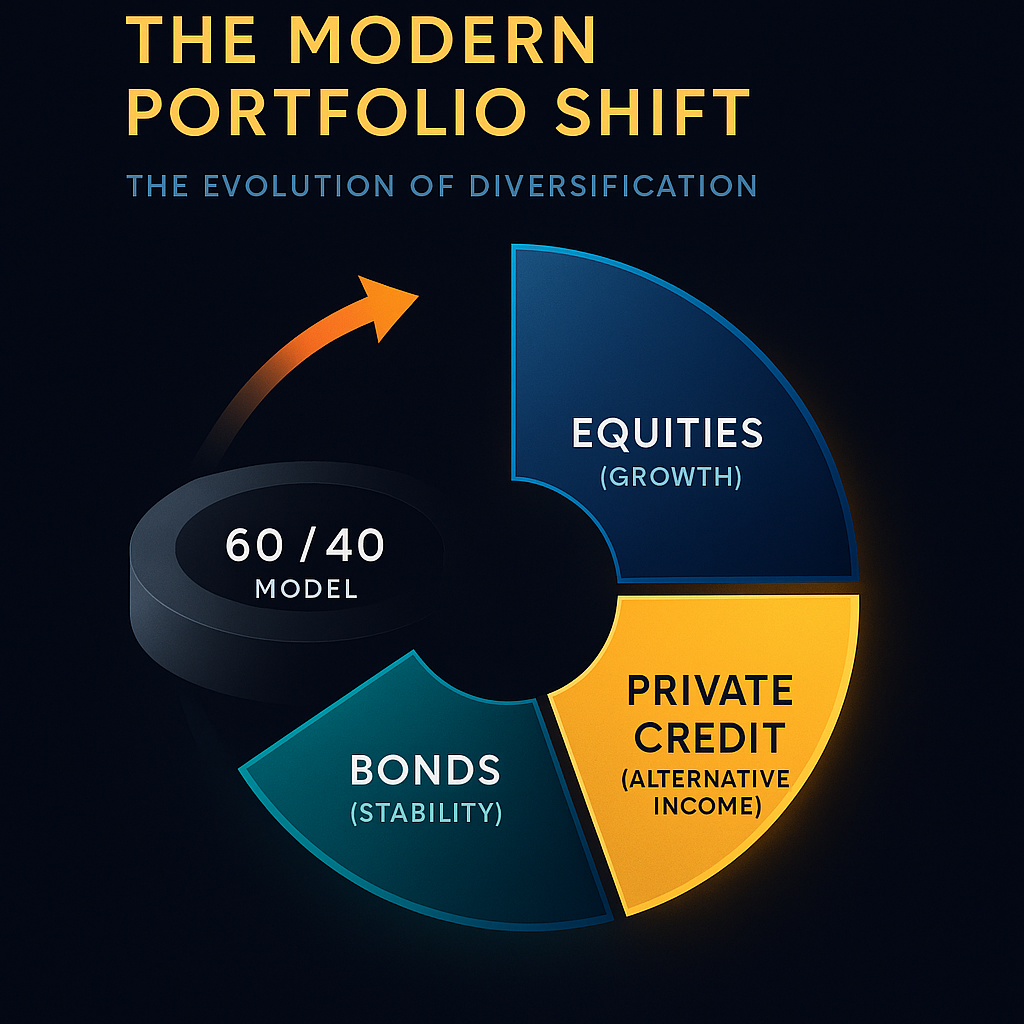

For most investors, the phrase “portfolio diversification” conjures images of a classic 60/40 split between stocks and bonds. The idea is simple: equities provide growth, while bonds provide stability and income. But the investment world has changed. Bond yields have been historically low for much of the past two decades, equity markets have been more volatile, and inflation has complicated the role of traditional fixed income. As a result, investors are increasingly exploring alternative asset classes to build more resilient portfolios.

One of the most prominent alternatives gaining traction is private credit—lending that occurs outside the traditional banking system and public bond markets. For those looking to diversify, private credit offers unique characteristics that complement, rather than replace, traditional holdings.

Why Diversification Matters More Than Ever

Diversification isn’t just about owning “a lot of things.” It’s about owning different things that behave differently under stress. When one part of the portfolio struggles, another can help offset losses.

The challenge is that many traditional asset classes have become more correlated over time. During major downturns—think the global financial crisis or the early COVID-19 crash—stocks and bonds often moved in the same direction, leaving investors exposed. That’s where alternatives like private credit come in: they can add sources of return that don’t always move in sync with public markets.

The Case for Private Credit as a Diversifier

Private credit provides diversification benefits in several ways:

1. Lower Correlation to Public Markets

Private credit returns are not determined by daily market trading. Instead, they are tied to negotiated loan agreements, contractual interest payments, and borrower performance. As a result, they tend to move independently of stock prices or bond yields, offering a stabilizing effect in turbulent times.

2. Attractive Yield Potential

Because private credit is less liquid and carries additional risks, borrowers typically pay higher interest rates. This “illiquidity premium” can be appealing in a diversified portfolio, especially when traditional fixed income yields are low. Investors can earn steady cash flows without depending solely on public debt markets.

3. Floating-Rate Structures

Many private loans are structured with floating rates tied to benchmarks like SOFR. This means yields can rise in a higher-rate environment, protecting investors from inflation-driven erosion of returns. In contrast, traditional bonds with fixed coupons often lose value when rates rise.

4. Customized Protections

Private loans often include covenants and collateral, giving lenders additional safeguards. These protections can reduce downside risk compared to public debt securities, where investor influence is limited.

Where Private Credit Fits in a Portfolio

Most institutional investors—pension funds, endowments, and insurance companies—allocate 5% to 15% of their portfolios to private credit. For individual accredited investors, the right allocation depends on factors like liquidity needs, time horizon, and overall risk tolerance.

- For income seekers: Private credit can serve as a higher-yielding replacement for part of the bond allocation.

- For growth-focused investors: It can act as a stabilizer, generating steady returns that balance the volatility of equities.

- For risk-aware investors: The asset class offers downside protections through covenants and collateral, though it still carries default risks.

The key is balance. Private credit should be viewed as a complement to, not a substitute for, equities or public fixed income.

Risks to Keep in Mind

No diversification tool is perfect, and private credit comes with its own set of risks:

- Illiquidity: Capital may be locked up for years, making it unsuitable for investors who need quick access to funds.

- Manager Risk: Performance depends heavily on the expertise of the private credit manager. Poor underwriting or weak borrower relationships can lead to losses.

- Default Risk: During economic downturns, defaults may rise, especially in industries sensitive to business cycles.

- Valuation Opacity: Unlike public bonds, private credit positions are not priced daily, so investors must rely on periodic reports.

Diversification works best when investors understand not only how assets can help—but also how they might fail under stress.

How Private Credit Has Performed in Practice

Recent history highlights the role of private credit in diversified portfolios:

- Post-2008 Financial Crisis: With banks reducing lending, private credit filled the gap, delivering attractive returns at a time when public credit markets were struggling.

- COVID-19 Pandemic: Many feared widespread defaults, but private credit proved resilient, thanks to covenant protections and active management. In fact, investor demand surged after 2020, as private loans generated income even while public markets seesawed.

- Rising-Rate Environment (2022–2023): Private credit’s floating-rate structures meant investors saw higher yields as central banks raised rates. Public bond investors, meanwhile, suffered steep losses as fixed coupons lost value.

These examples show why many investors view private credit as a ballast in portfolios—able to both protect during turbulence and capitalize on dislocations.

The Bottom Line for Investors

Diversification is no longer just about splitting between stocks and bonds. Today’s environment calls for creative approaches that add resilience and return potential. Private credit, with its combination of contractual income, low correlation to public markets, and structural protections, offers a compelling case for inclusion.

That said, it’s not for everyone. Investors must be comfortable with illiquidity, willing to commit capital for years, and confident in the managers they select. For those who can meet those conditions, private credit has the potential to play an important role in a diversified, modern portfolio.

In other words, when the traditional playbook feels outdated, private credit can be the “alternative chapter” investors didn’t know they needed.

{kind=link}