Liquidity has long been one of the biggest challenges in real estate investing. Traditional property ownership requires substantial capital, and selling a property can take months—or even years—depending on market conditions. Investors seeking quick access to cash or portfolio flexibility often find themselves constrained by the illiquid nature of physical real estate.

Enter tokenization, a blockchain-based innovation that transforms how property ownership is represented and traded. Tokenization enables fractional ownership through digital tokens, effectively turning real estate into a liquid asset class that can be bought, sold, or transferred with far greater ease than traditional property transactions. This article explores how tokenization enhances liquidity, the mechanisms involved, the benefits for investors, and key considerations to keep in mind.

What Is Tokenization in Real Estate?

Tokenization is the process of converting ownership rights in a property into digital tokens recorded on a blockchain. Each token represents a fractional interest in the underlying asset, which could be a single-family home, apartment building, commercial office, or even a portfolio of properties.

By creating these digital representations, tokenization allows multiple investors to hold a share of a property without requiring full ownership. Smart contracts govern token rights, including income distribution, voting rights, and transferability, making ownership transparent, secure, and programmable.

This concept connects directly to the broader discussion in The Rise of Tokenized Real Estate: How Blockchain Is Reshaping Ownership, which outlines the transformative impact of blockchain on property investing.

How Tokenization Enhances Liquidity

1. Fractional Ownership

Traditional real estate requires a buyer to acquire 100% of the property. Fractional ownership, made possible through tokenization, allows investors to purchase smaller portions. Lower entry costs broaden the investor base and make properties more marketable.

For example, a $2 million commercial building can be divided into 20,000 tokens priced at $100 each. Instead of finding a single buyer for the full building, the platform can facilitate thousands of smaller transactions, increasing the speed and flexibility of investment transfers.

2. Secondary Market Access

Many tokenized real estate platforms provide secondary markets where investors can trade tokens. Unlike traditional real estate, which requires listing with brokers, contract negotiation, and often lengthy closing periods, tokenized assets can be exchanged quickly and with transparent pricing.

This secondary market reduces the typical liquidity constraints associated with property investment and enables investors to rebalance portfolios, access cash, or respond to market changes more rapidly.

3. Smart Contracts and Automation

Smart contracts automate the transfer of tokens and the distribution of rental income or other cash flows. This automation reduces operational friction and delays, making ownership transfers faster and more reliable. Investors no longer need to wait for manual processing or lengthy legal procedures to execute transactions.

Benefits of Increased Liquidity

- Portfolio Flexibility: Investors can diversify holdings more easily, allocate capital to new opportunities, or exit positions without waiting for a full property sale.

- Reduced Capital Lock-Up: Tokenization lowers the barrier to entry and reduces the duration that capital is tied to a single asset.

- Broader Investor Access: Fractional ownership attracts retail and global investors, expanding demand and enhancing market activity.

- Market Transparency: Blockchain records provide clear, verifiable ownership history, reducing the friction and risk associated with private transactions.

Real-World Applications

Several platforms exemplify how tokenization drives liquidity:

- RealT: Offers fractional ownership of U.S. rental properties with automated rental income distributions. Secondary markets allow investors to trade tokens easily.

- Slice RE: Focuses on commercial property tokenization with legal compliance and secondary trading capabilities, making global investors’ participation more efficient.

- SolidBlock: Facilitates international luxury and commercial property investments, offering secondary trading to improve exit options for investors.

These platforms demonstrate that tokenization is not just theoretical—it provides tangible liquidity benefits that improve investor flexibility.

Considerations and Risks

Despite its advantages, investors should be mindful of certain risks:

- Regulatory Environment: Laws surrounding tokenized real estate are evolving. Compliance with securities regulations is crucial.

- Market Liquidity: While tokenization improves liquidity, secondary markets may still be limited, especially for niche or high-value properties.

- Valuation and Pricing: Accurate pricing depends on market demand and quality of information provided on the platform.

- Technology Risks: Smart contracts and blockchain systems must be secure; bugs or hacks could impact ownership or liquidity.

Investors should carefully vet platforms, understand regulatory protections, and consider asset type and market demand before participating.

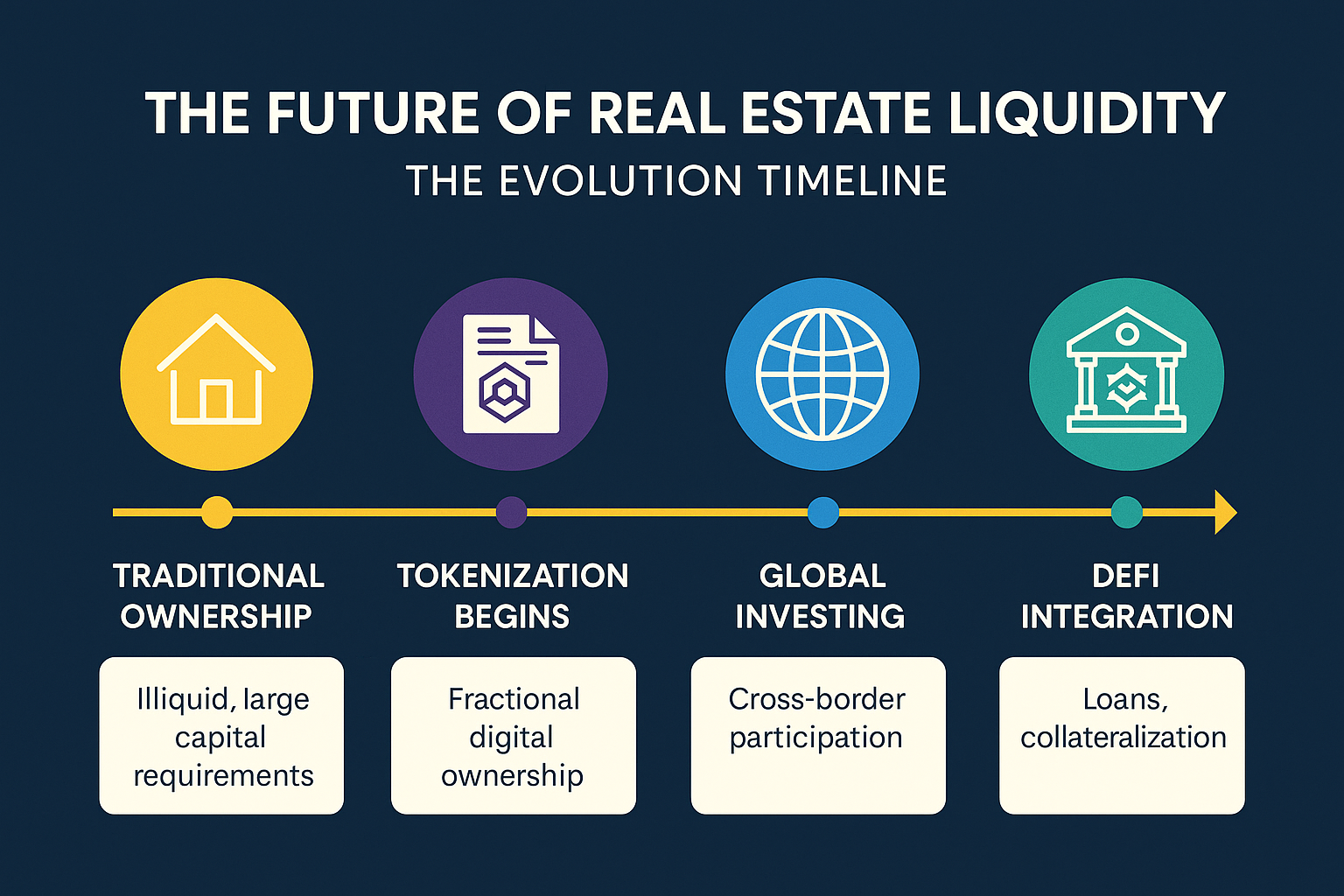

The Future of Liquidity in Real Estate

As technology matures, tokenized real estate is expected to significantly enhance liquidity across property markets:

- Integration with DeFi: Investors could use tokenized properties as collateral for loans, unlocking additional financial flexibility.

- Global Investment Access: Tokenization allows cross-border participation, expanding the pool of buyers and sellers.

- Portfolio Management Tools: Enhanced analytics and automated management will streamline secondary trading and improve market efficiency.

Ultimately, tokenization represents a paradigm shift in how investors approach real estate, bridging the gap between traditional property ownership and the speed, transparency, and flexibility of digital markets.

{kind=link}