Venture capital (VC) has become synonymous with innovation, risk-taking, and the pursuit of outsized returns. When most people think about startups—whether it’s Apple in a garage, Google at Stanford, or the latest AI unicorn—they’re often unknowingly thinking about venture capital. Behind many of the world’s most transformative companies stands a VC firm that provided early funding, guidance, and connections that turned ideas into global businesses.

Yet, for all the headlines about billion-dollar IPOs and splashy valuations, venture capital is not well understood outside of Silicon Valley and Wall Street. For investors—especially those interested in alternative assets—understanding how VC works is essential. Venture capital plays a unique role in portfolios: it’s risky, illiquid, and long-term, but it also offers exposure to the next generation of high-growth companies that could define the future.

This article takes a deep dive into venture capital, covering its history, how funds operate, strategies investors use, risk and return dynamics, and where the industry is heading. By the end, you’ll have a grounded, practical understanding of what VC is—and whether it fits in your investment playbook.

The Origins of Venture Capital

Venture capital as we know it today emerged in the mid-20th century, but its roots go further back. Wealthy individuals have always funded risky enterprises—think of European backers of overseas voyages in the 16th and 17th centuries. These early investors shared similarities with modern venture capitalists: they took on huge risk for the chance at equally huge returns.

The modern VC industry began after World War II. In 1946, Georges Doriot founded American Research and Development Corporation (ARDC), one of the first VC firms. ARDC’s most famous investment was in Digital Equipment Corporation (DEC), where a $70,000 stake grew to over $350 million by the time DEC went public in 1968. That single deal proved venture capital could be not just profitable, but transformative.

Through the 1970s and 1980s, the VC ecosystem expanded, particularly in California’s Silicon Valley. Firms like Sequoia Capital and Kleiner Perkins became synonymous with startup investing, funding companies such as Apple, Genentech, and later, Google and Amazon. Over time, the industry professionalized, with standardized fund structures, limited partnerships, and clearer performance benchmarks.

Today, venture capital is a global, multi-trillion-dollar industry. While Silicon Valley remains the epicenter, hubs have emerged in Boston, New York, London, Berlin, Bangalore, Shanghai, and beyond. VC funds now back everything from biotech to fintech, climate tech to consumer apps.

How Venture Capital Works

At its core, venture capital is about backing startups and high-growth companies at different stages of their development. Unlike private equity buyouts, which often target mature businesses, VC focuses on earlier stages when companies are unproven, often pre-profit, and sometimes even pre-revenue.

Here’s how the process typically works:

- Fundraising – VC firms raise money from investors, called limited partners (LPs). LPs might include pension funds, university endowments, sovereign wealth funds, family offices, or high-net-worth individuals. The VC firm itself, called the general partner (GP), manages the fund.

- Sourcing Deals – VC firms build networks of entrepreneurs, accelerators, universities, and angel investors to find promising startups. Deal flow—the steady stream of potential investments—is a critical factor in a VC firm’s success.

- Due Diligence – Startups are evaluated based on their team, market potential, product, technology, business model, and traction. Given the high risk, due diligence is both art and science.

- Investment – If the startup is a fit, the VC firm invests, typically in exchange for equity (shares) and often a board seat. Investments happen in “rounds”—Seed, Series A, B, C, and so on—each designed to fund the company to the next milestone.

- Value-Add – Beyond capital, VC firms provide guidance, mentorship, strategic advice, and access to networks of talent, customers, and future investors.

- Exit – After years of growth, the VC aims to exit the investment, typically through an IPO, acquisition, or secondary sale of shares. Profits (if any) are distributed back to LPs.

Venture capital funds usually have a 10-year lifespan: the first few years for investing, the middle years for building, and the later years for exiting.

The Fund Structure

A VC fund is usually set up as a limited partnership (LP):

- Limited Partners (LPs): Provide most of the capital but have limited liability and little say in day-to-day decisions.

- General Partners (GPs): Manage the fund, source deals, and support portfolio companies. They invest a small percentage (typically 1–5%) of the total capital to show commitment.

Compensation follows the classic “2 and 20” model:

- 2% Management Fee – Paid annually on assets under management, used to cover operating expenses.

- 20% Carried Interest – The GP’s share of profits above a certain return threshold, usually called the “hurdle rate.”

This model incentivizes GPs to generate big wins since most of their compensation comes from carry, not fees.

Stages of Venture Capital Investing

Startups don’t raise money all at once—they raise in stages, each designed to reduce risk as the company grows:

- Pre-Seed/Seed – Funding the idea, prototype, or very early traction. Often $100K–$2M. Extremely high risk.

- Series A – Funding product-market fit and scaling initial growth. Typically $2M–$15M.

- Series B and Beyond – Scaling operations, entering new markets, hiring extensively. Rounds can be $20M–$100M+.

- Late-Stage/Pre-IPO – Funding global expansion or prepping for an exit. Hundreds of millions of dollars are common.

Each stage carries different risks, returns, and investor profiles. Early rounds have higher upside but higher failure rates. Later rounds are safer but often priced at higher valuations, limiting returns.

The Risk–Return Profile

Venture capital is famously risky. Studies show that:

- Most startups fail. Roughly 65–70% of VC-backed startups fail to return capital.

- Power law dynamics apply. A small handful of “home runs” drive the vast majority of returns. For instance, one Uber or Airbnb can make up for dozens of failures.

- Returns are skewed. The median VC fund underperforms public markets, but the top quartile can deliver extraordinary gains.

Historically, VC funds have delivered 10–15% net annualized returns, though top-performing funds exceed 20–30%. But returns vary significantly depending on fund vintage, sector focus, and geography.

For LPs, VC is less about smooth annual returns and more about access to outsized winners. Missing out on a transformative company can mean underperformance.

The Value of Venture Capital Beyond Returns

While investors care about financial performance, venture capital plays a unique role in the broader economy:

- Innovation Engine: VC funding has driven breakthroughs in computing, biotech, fintech, renewable energy, and more.

- Job Creation: Startups funded by VC are significant job creators, often hiring rapidly as they scale.

- Economic Growth: Many of the world’s largest companies today—Apple, Amazon, Meta, Google—were once VC-backed startups.

- Social Impact: Increasingly, VC is funding solutions for climate change, healthcare access, financial inclusion, and other global challenges.

In short, venture capital isn’t just about returns—it’s about shaping the future.

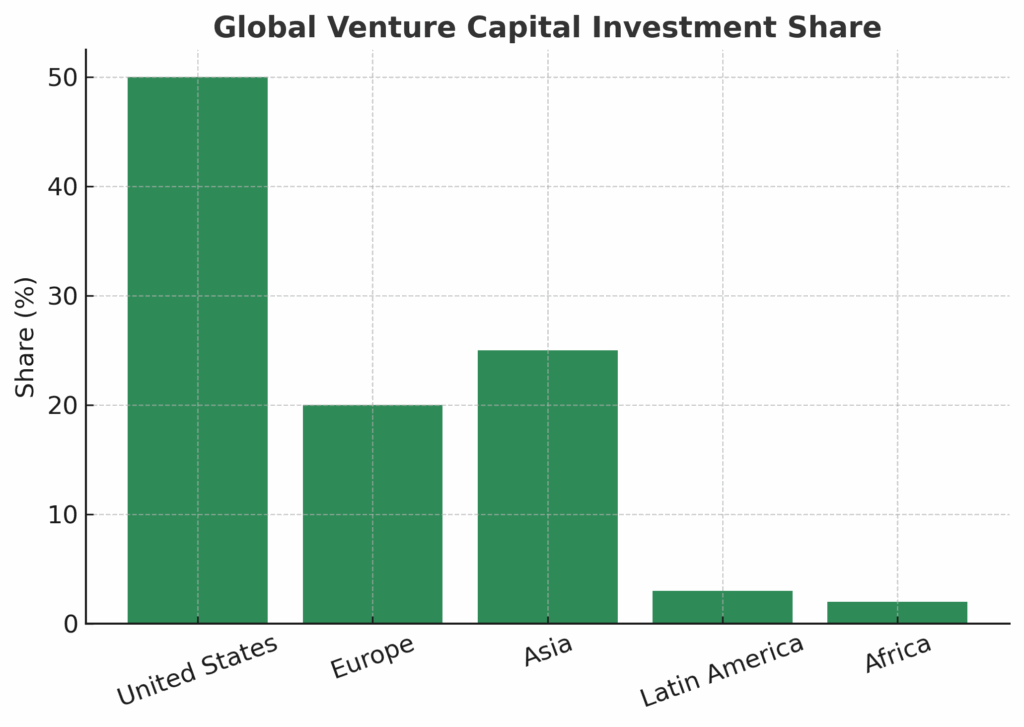

Global Venture Capital Trends

Venture capital has gone global. While the U.S. still accounts for the majority of VC activity, Europe, Asia, and emerging markets have grown rapidly.

- United States: Silicon Valley remains dominant, but hubs like Austin, New York, Boston, and Miami are gaining.

- Europe: London, Berlin, and Paris have become hotbeds for fintech, AI, and climate tech.

- Asia: China has built a massive VC ecosystem, backing companies like ByteDance and Didi. India’s startup scene, particularly in fintech and e-commerce, is booming.

- Africa and Latin America: Growing populations and mobile-first markets have created fertile ground for fintech, logistics, and healthtech startups.

Globalization means investors have more opportunities but also face more competition and geopolitical risk.

How Investors Can Access Venture Capital

For institutional investors like pension funds and endowments, investing in VC often means allocating to established funds. But for individual investors, the options are expanding:

- VC Funds: Traditional access, but usually limited to accredited investors with high minimums ($1M+).

- Fund of Funds: Provides diversification across multiple VC managers but with extra fees.

- Direct Angel Investing: Investing directly in startups, often via angel networks. Risky but rewarding for those with networks and expertise.

- Equity Crowdfunding: Platforms like SeedInvest and Republic allow smaller checks from non-accredited investors.

- Secondaries: Buying shares of late-stage startups from early employees or investors—less risky but also lower upside.

Each path has its own risk, liquidity, and return trade-offs.

Risks and Challenges in Venture Capital

Despite the allure, venture capital has challenges:

- Illiquidity: Capital is locked up for 7–10 years.

- High Failure Rate: Most startups won’t succeed.

- Valuation Risk: In hot markets, startups can be overvalued, reducing future returns.

- Access: Top-performing funds are often closed to new investors.

- Cyclicality: VC booms when capital is cheap and slows during downturns.

Investors must weigh whether VC’s high risk and illiquidity fit their portfolio goals.

The Future of Venture Capital

Looking ahead, several themes are shaping VC’s future:

- AI and Deep Tech: Artificial intelligence, quantum computing, and biotech remain hot targets.

- Climate Tech: Billions are flowing into carbon capture, renewable energy, and sustainable agriculture.

- Decentralized Finance (DeFi): Despite volatility, blockchain and crypto infrastructure attract long-term VC interest.

- Globalization: More capital is flowing into emerging markets, particularly India, Southeast Asia, and Africa.

- Diversity & Inclusion: LPs and GPs are pushing for more diverse founding teams and fund managers, which research shows improves performance.

Venture capital will continue to evolve, but its role as a driver of innovation is unlikely to diminish.

Final Thoughts

Venture capital is one of the most exciting, challenging, and misunderstood corners of the investment world. For investors, it represents both enormous opportunity and significant risk. The best VC investments can change industries and generate extraordinary returns. But success requires patience, access, diversification, and a tolerance for failure.

Whether you’re an institutional LP allocating to a billion-dollar fund, an angel investor writing small checks, or simply a curious observer, venture capital is worth understanding. It shapes the technologies, industries, and companies that will define our future.

For those who can stomach the risks, venture capital isn’t just an asset class—it’s a front-row seat to innovation.

{kind=link}