If you’ve spent any time in the investing world, you’ve probably heard the term “hedge fund” tossed around like it’s part of some exclusive club. And in many ways, it is. Hedge funds occupy a unique space in the financial landscape—part investment vehicle, part mystique. They’ve been credited with eye-popping gains, blamed for market chaos, and even mythologized in movies and books.

But behind the hype, what exactly is a hedge fund? How do they work? And most importantly: are they something everyday investors should care about—or are they only for Wall Street insiders and billionaires?

This article is here to strip away the jargon and give you a clear, comprehensive view of hedge funds: where they came from, how they’re structured, what strategies they use, and what risks and opportunities they present. Think of it as your one-stop guide to understanding hedge funds from the ground up.

The Origins of Hedge Funds

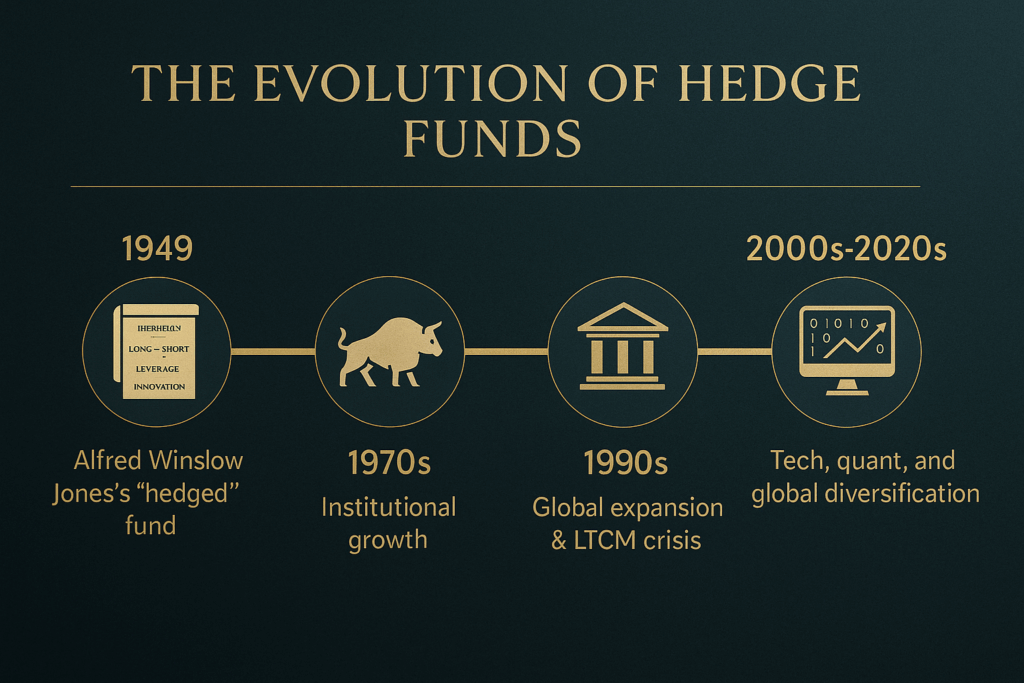

The hedge fund story begins in 1949, when Alfred Winslow Jones, a former sociologist and financial journalist, decided to try something new. Instead of simply buying stocks he thought would go up, Jones combined those bets with short-selling stocks he expected to fall. He then added leverage—borrowing money to amplify his positions.

The result was a portfolio that wasn’t as dependent on the overall direction of the stock market. If the market went up, his long positions could make money. If the market went down, his shorts could profit. This balancing act—“hedging” his risk—gave birth to the modern hedge fund.

Jones’ innovation worked. His fund consistently outperformed traditional mutual funds during the 1950s and 1960s, attracting attention and imitation. Over time, the industry exploded. What began as a niche strategy for wealthy investors grew into a global business managing trillions of dollars.

The term “hedge fund” stuck, even though many modern hedge funds don’t do much actual hedging. Instead, the name now refers broadly to private investment funds that pursue flexible, often complex strategies.

What Exactly Is a Hedge Fund?

At its simplest, a hedge fund is a private pool of capital managed by professionals who aim to deliver high returns using a wide range of investment strategies.

Several features set hedge funds apart from more familiar vehicles like mutual funds or ETFs:

- Flexibility: Hedge funds can invest in virtually anything—stocks, bonds, currencies, commodities, real estate, derivatives, even cryptocurrencies.

- Leverage: They often borrow money to increase their exposure, which can magnify both gains and losses.

- Short Selling: Hedge funds can bet against assets, profiting when prices fall.

- Derivatives: Options, futures, and swaps are common tools, allowing for complex strategies and hedging.

- Limited Access: They’re typically open only to accredited or institutional investors who meet income or net-worth thresholds.

- Private Structure: Hedge funds are usually organized as limited partnerships (LPs) or limited liability companies (LLCs), avoiding many of the regulations that govern public funds.

- Fee Models: The famous “2 and 20” arrangement charges investors a 2% annual management fee plus 20% of profits.

Taken together, these features give hedge funds a level of freedom that traditional funds lack. That freedom is both the source of their allure and the root of their risks.

How Hedge Funds Are Structured

The structure of hedge funds reflects their private nature. Most are set up as limited partnerships. Here’s how it typically works:

- General Partner (GP): The hedge fund manager, who makes investment decisions and runs the fund. The GP may also invest their own money in the fund, aligning interests with investors.

- Limited Partners (LPs): The investors—often institutions like pension funds, endowments, and insurance companies, as well as ultra-high-net-worth individuals. LPs provide the bulk of the capital but don’t participate in daily management.

This GP-LP structure comes with specific terms:

- Minimum Investment: Often $250,000 to $1 million or more.

- Lock-Up Periods: Investors may not be able to withdraw funds for a set time (often one to three years).

- Redemption Windows: Withdrawals may only be allowed quarterly or annually, with advance notice.

- High-Water Marks: A performance-based rule ensuring managers only collect incentive fees on new profits, not on regaining lost ground.

These terms create stability for managers, allowing them to pursue longer-term or less liquid strategies without fear of sudden investor withdrawals. But they also mean investors sacrifice liquidity in exchange for potential returns.

Hedge Fund Strategies

The term “hedge fund” covers a wide variety of approaches. Broadly, strategies fall into several categories:

1. Long/Short Equity

The most traditional approach. Managers buy stocks they believe are undervalued (long positions) and short stocks they think are overvalued (short positions). The goal is to generate returns regardless of whether the market rises or falls.

2. Global Macro

These funds make big bets on economic and geopolitical trends. They might trade currencies, commodities, or interest rates based on views about inflation, central bank policy, or political events. George Soros’ famous bet against the British pound in 1992 is a classic global macro play.

3. Event-Driven

Event-driven funds profit from corporate events such as mergers, acquisitions, spinoffs, or bankruptcies. A common tactic is merger arbitrage, where a fund buys the stock of a company being acquired while shorting the acquirer’s stock.

4. Relative Value/Arbitrage

These funds seek to exploit pricing inefficiencies between related securities. For example, convertible bond arbitrage involves buying a company’s convertible bonds while shorting its stock, capturing small mispricings.

5. Distressed Debt

These funds invest in the bonds of companies in financial distress or bankruptcy. The strategy bets on successful restructuring or asset recovery. While risky, it can deliver outsized gains if the company rebounds.

6. Quantitative (Quant)

Quant funds rely on mathematical models, algorithms, and big data to identify patterns and trade automatically. Firms like Renaissance Technologies have pioneered this space, often producing market-beating results.

7. Multi-Strategy

Some funds combine multiple approaches under one roof. By diversifying strategies, they aim to smooth returns and reduce volatility.

Each strategy has its own risk-return profile. Some aim for steady, low-volatility gains, while others swing for the fences.

Why Investors Choose Hedge Funds

So why would an institution or wealthy individual choose to put money into a hedge fund instead of just buying a diversified stock index fund?

- Diversification: Hedge funds often pursue strategies uncorrelated with traditional stocks and bonds, reducing overall portfolio risk.

- Absolute Return Focus: Unlike mutual funds, which aim to beat a benchmark index, hedge funds often aim for positive returns in any market environment.

- Access to Specialized Expertise: Hedge fund managers may have unique insights, research capabilities, or trading systems unavailable to the average investor.

- Crisis Performance: Certain hedge funds have thrived during downturns. For example, some global macro funds profited during the 2008 financial crisis by betting against housing and financial stocks.

For large institutions managing billions, these benefits can be significant—especially when the goal is long-term stability across market cycles.

The Risks of Hedge Funds

Of course, hedge funds come with risks that shouldn’t be underestimated:

- Leverage: Borrowing magnifies losses as well as gains. Hedge funds can unravel quickly if positions move against them.

- Liquidity Risk: Investors may not be able to withdraw money for years. Meanwhile, underlying assets (like distressed debt) may be hard to sell in a crisis.

- Fee Burden: The “2 and 20” fee structure means managers are well compensated, even in mediocre years. High fees can significantly eat into net returns.

- Manager Risk: Hedge fund success is often tied to the skill (or luck) of the manager. If they lose their edge—or leave the firm—performance can suffer.

- Opacity: Unlike mutual funds, hedge funds aren’t required to disclose holdings regularly. Investors may know little about what’s happening day-to-day.

There’s also systemic risk. The collapse of Long-Term Capital Management in 1998 showed how a heavily leveraged hedge fund could threaten the broader financial system. More recently, Archegos Capital’s implosion in 2021 wiped out billions from major banks.

Hedge Funds in Today’s Market

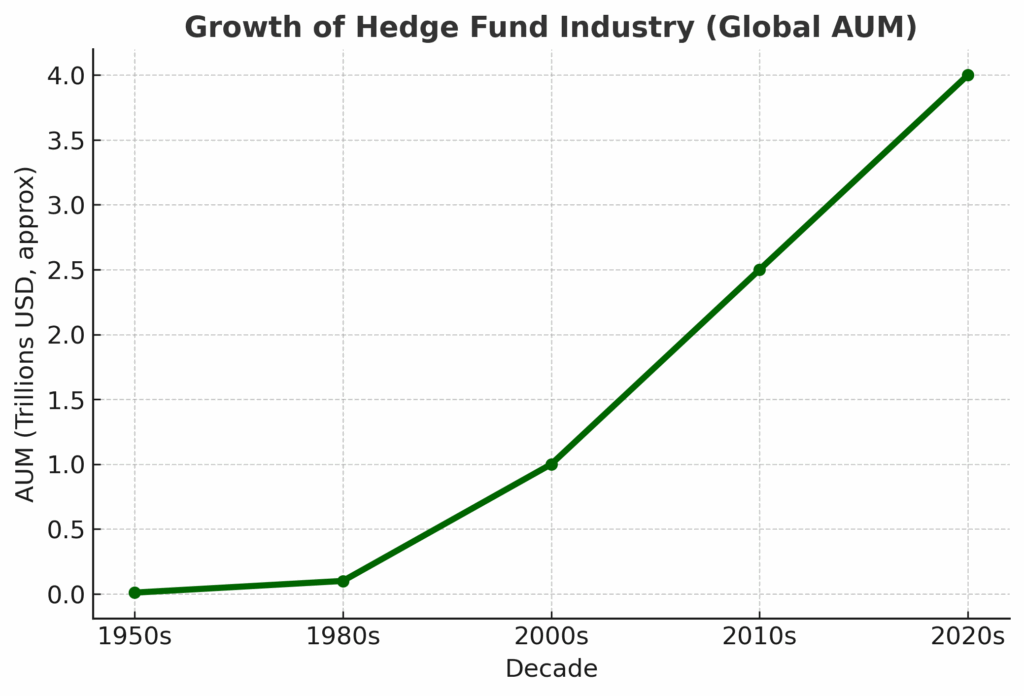

The hedge fund industry has matured considerably since Jones’ first fund in 1949. Today, hedge funds collectively manage over $4 trillion globally. But their role has shifted.

- Institutional Investors Dominate: Pension funds, sovereign wealth funds, and endowments now supply much of the capital, seeking diversification and alternatives to stocks and bonds.

- Alpha vs. Beta: With so many funds chasing opportunities, finding true “alpha” (market-beating returns) has grown harder. Many critics argue hedge funds underperform after fees.

- Regulatory Scrutiny: Hedge funds remain less regulated than public funds but face far more oversight than in the past. Reporting requirements to the SEC have increased.

- Innovation: Strategies evolve constantly, from quant funds using machine learning to funds dabbling in cryptocurrencies and ESG-related plays.

- Global Reach: Hedge funds are no longer a U.S.-only phenomenon. London, Hong Kong, and Singapore have become hubs, reflecting the globalization of finance. This cross-border presence means hedge funds are exposed to international politics, currency swings, and regulatory differences that can both create opportunity and add complexity.

What hasn’t changed is their ability to influence markets. A large hedge fund taking a position in oil futures, technology stocks, or even government bonds can ripple across sectors and borders, shaping outcomes for other investors whether they realize it or not.

Should You Consider Hedge Funds?

For most individual investors, hedge funds remain out of reach. Accreditation requirements and high minimums limit access to the wealthy. But there are reasons to understand them even if you never invest directly.

- Market Impact: Hedge funds are large, active players. Their trades can move currencies, commodities, and stock markets, affecting everyday portfolios indirectly.

- Educational Value: Studying hedge fund strategies can sharpen your understanding of risk, diversification, and market dynamics.

- Broader Access Emerging: “Liquid alternatives” and interval funds are now offering hedge fund–like strategies to retail investors, albeit with differences in structure and risk.

Whether or not you invest, hedge funds are part of the ecosystem shaping global finance.

Key Takeaways

- Hedge funds are private, actively managed pools of capital, accessible mainly to accredited investors.

- They pursue a wide range of strategies, from traditional long/short equity to complex arbitrage and quantitative trading.

- Benefits include diversification, absolute return potential, and access to specialized expertise.

- Risks include leverage, illiquidity, high fees, and heavy reliance on manager skill.

- While not available to most, hedge funds exert significant influence on financial markets.

The Bottom Line

Hedge funds sit at the intersection of ambition and risk. They aren’t designed for everyone—and for most retail investors, they aren’t even an option. But understanding them matters, because hedge funds shape markets in ways that affect us all.

At their best, hedge funds provide diversification, expertise, and the potential for extraordinary returns. At their worst, they amplify volatility and collapse spectacularly.

The hedge fund story is still evolving. In the years ahead, technology, artificial intelligence, and data science may reshape how funds operate, just as globalization and regulation have already done. New players may emerge while old giants fade, but the industry will remain an engine of financial innovation—and controversy.

For investors, the lesson is simple: hedge funds aren’t magic, and they’re not inherently evil. They are tools, powerful ones, that can deliver both tremendous value and devastating loss. Knowing how they work allows you to view them with clear eyes, whether you ever invest in one directly or simply navigate markets influenced by their actions.

{kind=link}