This Content Is Only For Subscribers

Cross-border real estate can diversify income, hedge inflation, and tap growth that doesn’t move in lockstep with your home market. The catch: you’re not only underwriting buildings—you’re underwriting jurisdictions. Here’s a clean, investor-friendly map of what changes when a fund buys or operates property abroad, and how to diligence a manager doing it well.

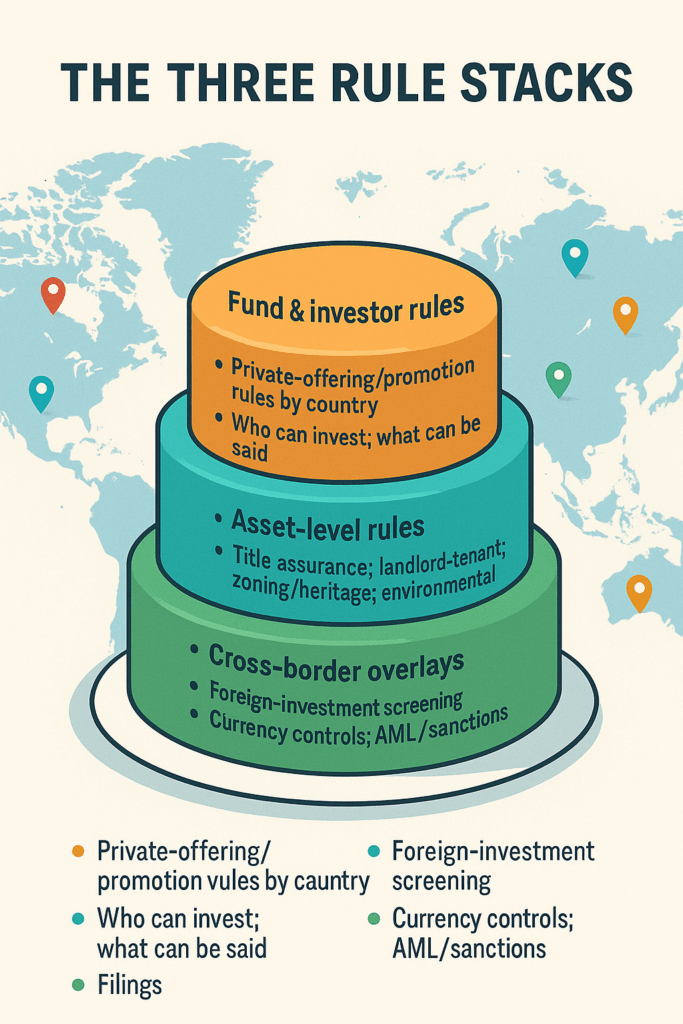

The three rule stacks to track

1) Fund & investor rules.

A fund may be domiciled in one country and marketed in several others. That triggers local private-offering or promotion rules—who can invest, what can be said publicly, and what filings are needed. Investor categories (accredited, professional, qualified purchaser equivalents) and verification standards vary.

2) Asset-level rules.

Each country’s property law DNA is unique: title assurance (land registry vs. title insurance), transfer taxes (stamp duty/notaries), landlord-tenant rules, zoning/heritage approvals, and environmental standards. These shape timelines, capex, and exit liquidity.

3) Cross-border overlays.

Expect foreign-investment screening (especially near ports, data centers, or critical infrastructure), currency controls, AML/sanctions expectations, data-privacy obligations, and sometimes economic-substance requirements for holding companies.

Domicile and structure: don’t chase acronyms—follow the cash

Cross-border funds often use a tax-neutral domicile (with seasoned administrator, auditor, and counsel) and local SPVs to hold each property. Focus on function:

- Does the structure avoid a second layer of tax at the fund level?

- Do local SPVs qualify for treaty benefits to reduce withholding on rents, interest, or dividends?

- Are substance measures (local directors, meetings, records) in place to support those treaty claims?

Ask for: a one-page structure chart with arrows for cash flows (rents → SPV → holding company → fund → investor) and notes where tax and withholding bite.

Taxes you actually feel

Cross-border real estate blends local taxes with withholding when cash moves up the chain.

- Entry: Transfer taxes/stamp duty/notary fees—often several percent of purchase price.

- Hold: Property taxes, municipal levies, payroll taxes for local staff, VAT/GST on services.

- Exit: Capital-gains or land-appreciation taxes; in some markets, selling shares of a property-rich SPV is taxed like selling the asset.

- Withholding: Outbound dividends/interest often face withholding; treaties can lower rates, but only if the structure actually qualifies.

Investor takeaway: Demand a sources-and-uses and cash waterfall that include local taxes and withholding, plus a sensitivity to treaty rates stepping up.

Capital, currency, and liquidity

Financing norms differ. Leverage levels, covenants, and lender types vary by country. Some markets rely on notarial mortgages or require lender consent for routine actions; others are more flexible.

Currency is portfolio risk. If leases or exits are in foreign currency, you own FX risk. Strong managers publish an FX policy: what’s hedged (income, equity, or both), instruments, counterparties, coverage ratios, and re-hedge triggers. Also check for repatriation rules and hard-currency access in the target country.

Liquidity isn’t universal. Permitting timelines, tenant customs, and legal formalities stretch leasing and exits in some jurisdictions. For open-end funds, redemption terms should match those realities (think gates/queues).

Compliance you won’t see in the brochure

- Foreign-investment reviews: Filings, timelines, and potential conditions for sensitive assets or locations.

- KYC/AML & sanctions: Enhanced onboarding, beneficial-owner checks, and vendor/tenant screening across borders.

- Data & privacy: Tenant systems (access control, payments, IoT) may trigger local privacy rules and cross-border transfer controls.

- Anti-corruption: Documented policies for gifts/hospitality, vendor vetting, and permit interactions.

Property-law realities to price in

- Title & transfer: Some countries rely on registries and notaries, not title insurance.

- Leases: Indexation (e.g., CPI), “triple-net” norms, break clauses, and eviction timelines vary—so will capex obligations.

- Construction & ESG: Environmental impact assessments, energy-performance standards, and penalties can shift budget and exit value.

Ask for: a brief jurisdiction memo per country—title mechanics, lease norms, transfer taxes, environmental/ESG standards, and any foreign-ownership caps.

Green flags vs. red flags

Green flags

- A jurisdiction matrix listing marketing permissions, foreign-investment approvals, and timelines.

- Structure chart with tax/withholding footnotes and treaty-rate sensitivities.

- Written FX policy (coverage ratios, triggers, counterparties) and lender term sheets.

- Local operating partners with references from lenders and anchor tenants.

- Evident substance where treaty benefits are claimed (board minutes, local directors, records).

Red flags

- Returns that depend on aggressive treaty positions without substance.

- No plan for FX or repatriation risk in controlled-currency markets.

- Vagueness on foreign-investment screening or ownership limits.

- Thin vendor diligence in higher-risk markets; no anti-corruption logs.

- Open-end liquidity that ignores long local exit timelines.

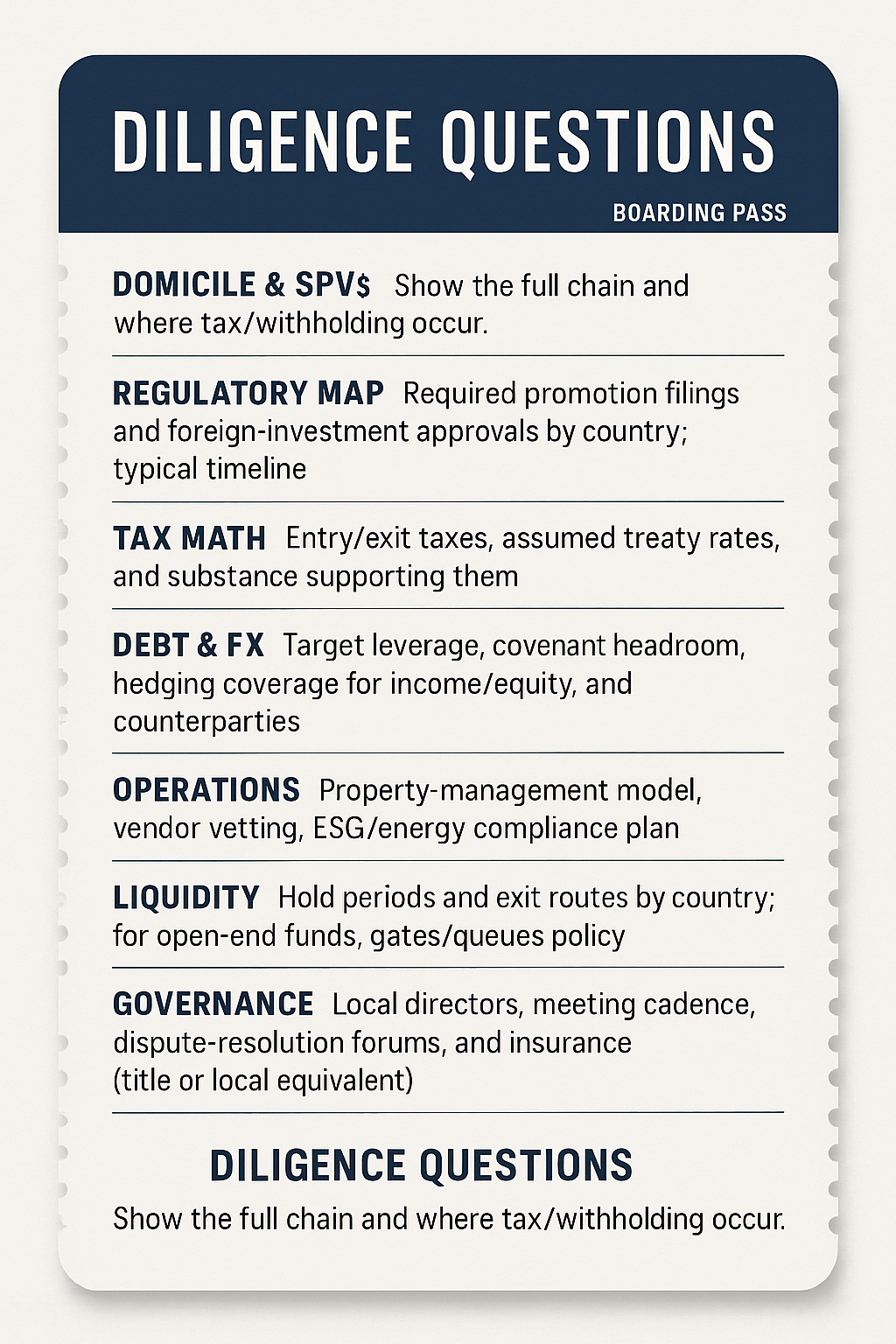

Diligence questions to copy/paste

- Domicile & SPVs: Show the full chain and where tax/withholding occur.

- Regulatory map: Required promotion filings and foreign-investment approvals by country; typical timeline.

- Tax math: Entry/exit taxes, assumed treaty rates, and substance supporting them.

- Debt & FX: Target leverage, covenant headroom, hedging coverage for income/equity, and counterparties.

- Operations: Property-management model, vendor vetting, ESG/energy compliance plan.

- Liquidity: Hold periods and exit routes by country; for open-end funds, gates/queues policy.

- Governance: Local directors, meeting cadence, dispute-resolution forums, and insurance (title or local equivalent).

Bottom line

Cross-border real estate can add resilient income and uncorrelated growth—but only if the jurisdictional plumbing is as sturdy as the asset story. Focus on structure (tax and substance), FX and financing, screening and permits, and the everyday realities of property law. If a manager can walk you through those specifics calmly and clearly, you’ve found a strategy that’s built to travel.

{kind=link}