This Content Is Only For Subscribers

Crypto funds can look and feel like traditional hedge or venture funds, but their tax footprints can be very different. If you’re evaluating an allocation, here’s a clear, non-jargony guide to what typically shows up on your tax forms, what can change the character of income, and the questions to ask before you wire. (This isn’t tax advice—use it as a map for a smarter conversation with your advisor.)

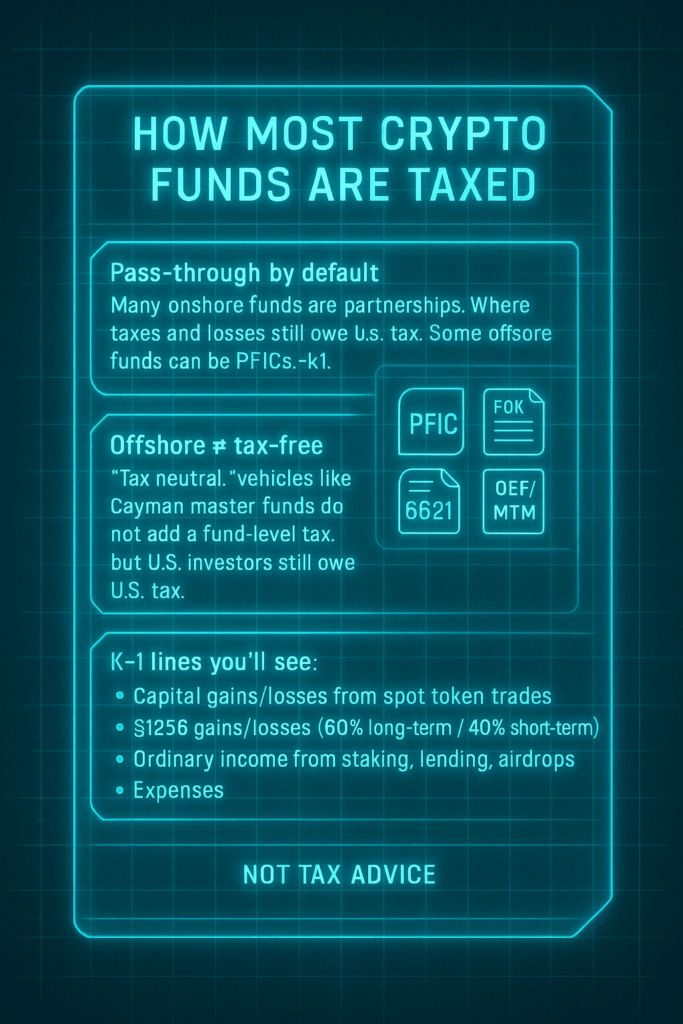

How most crypto funds are taxed

Pass-through by default.

Many onshore funds are partnerships for tax purposes. Instead of the fund paying tax, income and losses pass throughto you, usually reported on a Schedule K-1. You may owe tax even if the fund didn’t distribute cash (classic “phantom income”), so build that into your liquidity plan.

Offshore ≠ tax-free.

“Tax neutral” vehicles (e.g., Cayman master funds) generally don’t add a fund-level tax. But U.S. investors still have U.S. tax, and some offshore corporate feeders can be PFICs—triggering Form 8621 reporting and elections (QEF/mark-to-market). Ask the manager whether your feeder is a partnership or corporation and what forms they issue.

What shows up on the K-1.

- Capital gains/losses from spot token trades.

- Section 1256 gains/losses if the fund trades regulated crypto futures (e.g., on CME)—typically 60% long-term / 40% short-term, with year-end mark-to-market.

- Ordinary income from things like staking rewards, lending interest, or airdrop receipts.

- Expenses (management fees and certain fund costs) that affect your net.

What changes the character of income

Spot trading vs. derivatives.

Spot buys/sells typically produce capital gain/loss. Regulated futures (if used) often fall under §1256 (60/40). Unregulated derivatives or perpetual swaps can have different outcomes—ask the fund how those are treated on the K-1.

Staking, airdrops, and protocol “emissions.”

Rewards are commonly treated as ordinary income when you have dominion and control (i.e., you can transfer or sell them). Later, when you sell the rewarded tokens, you may also have a capital gain/loss relative to the value you recognized at receipt.

Lending and “yield.”

Off-chain lending income is usually ordinary. On-chain lending may also be ordinary, but details can vary with the instrument. The key for you is how the fund categorizes it—and whether any withholding or information reportingapplies to your situation.

Hard forks and token migrations.

Some events can trigger taxable income at receipt; others are non-events. A good fund explains its policy for forks, mergers, and token swaps and how basis is tracked.

Wash sale rules.

As of now, wash sale rules generally don’t apply to many digital assets the way they do to stocks, but proposals come and go. Sensible managers document their approach in case rules tighten.

Tax-exempt and non-U.S. investors: special angles

Tax-exempt (foundations, endowments, IRAs).

Leverage or certain income can create UBTI (unrelated business taxable income). To avoid that, many tax-exempts invest through an offshore blocker corporation (accepting some corporate tax “leakage”). Ask whether the feeder you’re using blocks UBTI and how much drag that adds.

Non-U.S. investors.

Capital gains from trading may be outside the U.S. net, but ECI (effectively connected income) is different and triggers §1446 withholding by partnerships. Many global funds rely on trading safe harbors and/or an offshore master to manage ECI risk. Ask the manager for a one-page memo on ECI/withholding posture and what forms you’ll receive (often W-8 series plus capital statements).

State taxes and multi-jurisdiction issues

Even if the fund is pass-through, you could have state filing obligations (e.g., if the fund has nexus to multiple states). Internationally, you may face FATCA/CRS information reporting and local rules if you’re outside the U.S. Expect to complete W-9/W-8 forms and occasional residency certificates.

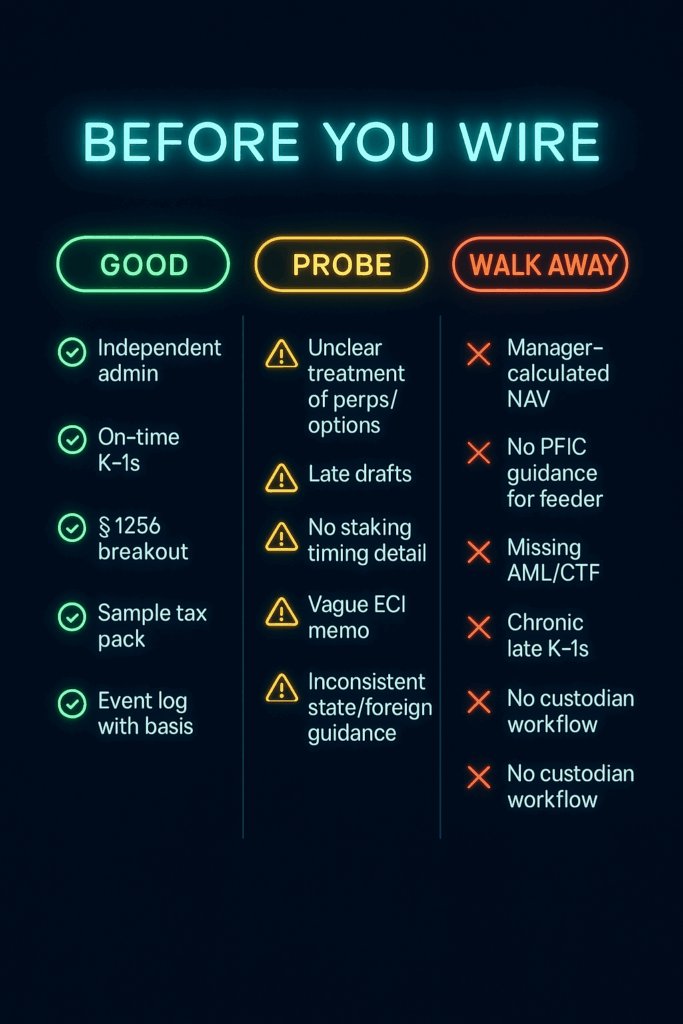

Reporting quality matters (more than you think)

Crypto creates messy basis and lot tracking, plus odd lots from airdrops, staking, and fee rebates. The smoothest tax seasons come from managers who:

- Provide timely K-1s (or Form 8621 packages) with clear footnotes.

- Break out 1256 vs. non-1256 items.

- Spell out staking/airdrop timing and fair values used.

- Document token events (forks, migrations) and how basis was carried forward.

- Offer a sample tax package during diligence, not in April.

Questions to ask your manager (copy/paste)

- Entity & forms: Is my feeder a partnership or corporation? Will I receive a K-1 or PFIC Form 8621 (or both)?

- Income mix: What portion of expected P&L is capital vs. ordinary (staking, lending, airdrops)? Any §1256exposure?

- Staking policy: When do you treat rewards as realized income, and how do you determine fair value?

- Derivatives: Which venues and instruments? How do you report perpetuals and options?

- UBTI/ECI: For tax-exempt/non-U.S. investors, how do you manage UBTI and ECI? Is there a blocker and what’s the expected tax drag?

- State & foreign filings: Do investors commonly need state returns? Any local withholding in other countries?

- Timing: When are draft and final tax packs delivered? Any history of late K-1s?

- Changes: What changed in your tax approach after audits, rule updates, or new products (e.g., staking providers, futures usage)?

Practical takeaways

- Expect pass-through complexity. Crypto strategies mix capital and ordinary income. Plan for cash to pay taxeseven without distributions.

- Derivatives can help or hurt. §1256 can be favorable, but unregulated products can complicate character and sourcing—make sure you understand the mix.

- Yield isn’t “free.” Staking and lending create ordinary income now and capital gains later—two bites of the apple.

- Structures matter. Offshore feeders and blockers can solve UBTI/ECI problems but add reporting and potential tax drag.

- Documentation is destiny. Choose managers who can show their work on valuations, token events, and categorization. Your CPA will thank you—and your April will be calmer.

With the right questions upfront and a manager who treats tax as part of risk management, you can keep surprises to a minimum and let the investment thesis, not the paperwork, drive your decision.

{kind=link}