This Content Is Only For Subscribers

Real estate funds can look straightforward—buy buildings, collect rent, share profits—but the rules that protect you as an investor live in several layers. Think of it as a safety net made from securities law, fund documents, governance and audits, and property-level law. Here’s a clear, practical guide to what that net includes and how to use it.

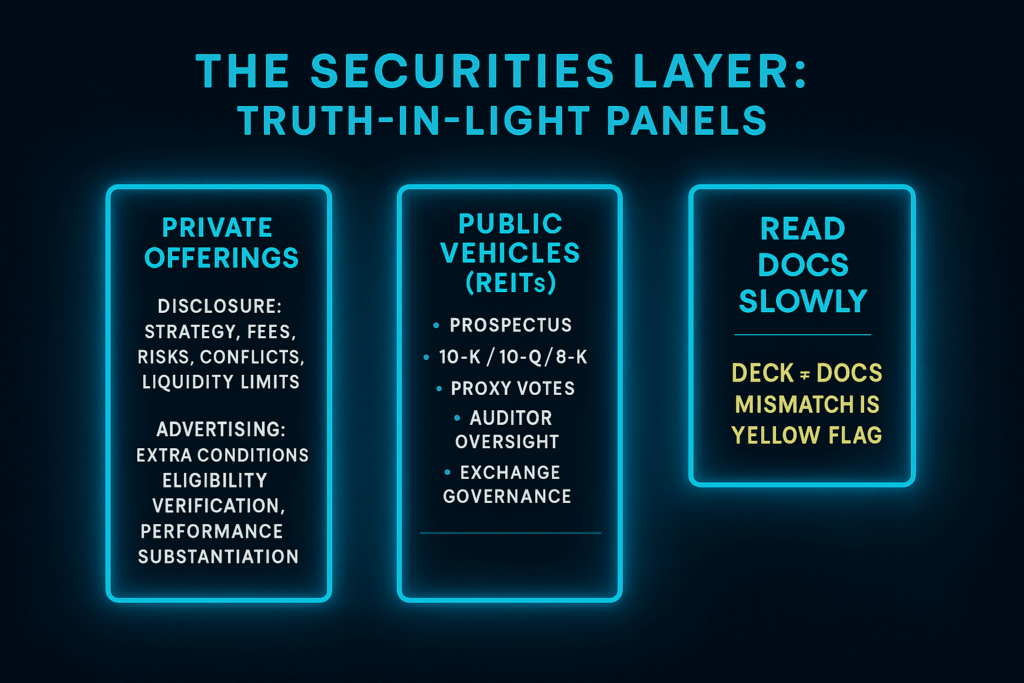

1) The securities layer: how money is raised and promises are made

Most real estate funds raise capital through private offerings. Investor-protection here centers on truthful, complete disclosure and who may invest. Managers must accurately describe strategy, fees, risks, conflicts, and liquidity limits. If a fund advertises, additional conditions kick in (for example, verifying investor eligibility and substantiating performance claims). For public vehicles—like listed REITs—there’s a higher bar: prospectuses, ongoing 10-K/10-Q reporting, proxy votes, auditor oversight, and exchange governance rules.

What to do: Read the offering documents slowly. If the slide deck and the legal docs don’t match word-for-word, treat that as a yellow flag.

2) The adviser layer: fiduciary duty, marketing, and records

Investor protection doesn’t stop at the fund—it extends to the adviser (the manager that runs it). Advisers owe a fiduciary duty: act in your best interest, disclose conflicts, and keep accurate books and records. Modern marketing rules require that performance be fair and balanced, testimonials or third-party ratings carry clear disclosures, and claims be backed by workpapers. Regulators examine whether fees were charged according to the documents and whether expense allocations (travel, research, deal costs) were fair.

What to do: Ask the manager to “show the math” behind any performance chart, and request one anonymized expense-allocation example the auditor has reviewed.

3) The fund-document layer: your real rulebook

Three documents control your life as an LP:

- Private Placement Memorandum (PPM): strategy, risks, conflicts.

- Limited Partnership/Operating Agreement: economics, voting, removal rights, and waterfall.

- Subscription & side letters: your eligibility, reporting, and any negotiated rights.

Key protections to look for:

- Fee transparency: management fee, promote (carried interest), and offsets for related-party property-management or development fees.

- Valuation policy: appraisal cadence, independence, and how development assets are marked.

- Liquidity terms: capital calls, recycling, and (for open-ended vehicles) gates/queues and suspension mechanics.

- Conflicts controls: co-investment, cross-fund trades, and allocation rules when two funds want the same deal.

- Removal/voting: when LPs can replace the manager for cause; LP advisory committee (LPAC) approvals for conflicts and valuation overrides.

What to do: Build a one-page “term sheet” from the LPA with numbers (fees, hurdle, catch-up, offsets) and process triggers (who approves what, and when).

4) Governance, audits, and independent eyes

Investor protection improves when independent people check the numbers:

- Independent administrator tracks capital accounts and calculates NAVs.

- Independent auditor reviews year-end financials and fee/waterfall calculations.

- Valuation committee or external appraisers provide checks on marks.

- Independent directors (for some vehicles) add oversight on conflicts, gates, and side pockets.

What to do: Ask whether the administrator—not the manager—calculates NAV and capital accounts, and whether auditors re-perform the waterfall each year.

5) Custody, controls, and cash handling

At the fund and property level, controls protect cash:

- Bank and escrow controls: dual approvals, segregation of operating and capital accounts, vendor onboarding procedures.

- Debt compliance: covenant monitoring (DSCR, LTV), interest-rate hedge policies, and early-warning triggers.

- Insurance: property, liability, flood/wind, builder’s risk, and business interruption.

What to do: Request the cash-movement policy (who can wire, with what approvals) and a sample bank reconciliation signed by the administrator.

6) Property-level protections you might overlook

Compliance at the asset level is investor protection in disguise:

- Landlord-tenant and fair-housing rules protect tenants and reduce legal risk.

- Building codes, life-safety, and accessibility protect occupants and preserve value.

- Environmental diligence (Phase I/II, remediation plans) prevents unpleasant surprises.

What to do: In quarterly reports, look for an ESG/compliance dashboard: inspections passed, permits obtained, accessibility fixes completed, and open issues with due dates.

7) AML, sanctions, and beneficial ownership

Funds must know their investors and counterparties. Expect KYC/AML screening, sanctions checks, and—in many jurisdictions—beneficial-ownership reporting for entities in the structure. These controls reduce the risk of frozen accounts, rejected wires, or reputational damage.

What to do: Ask how often the manager refreshes investor and vendor screenings, and which third-party tools they use.

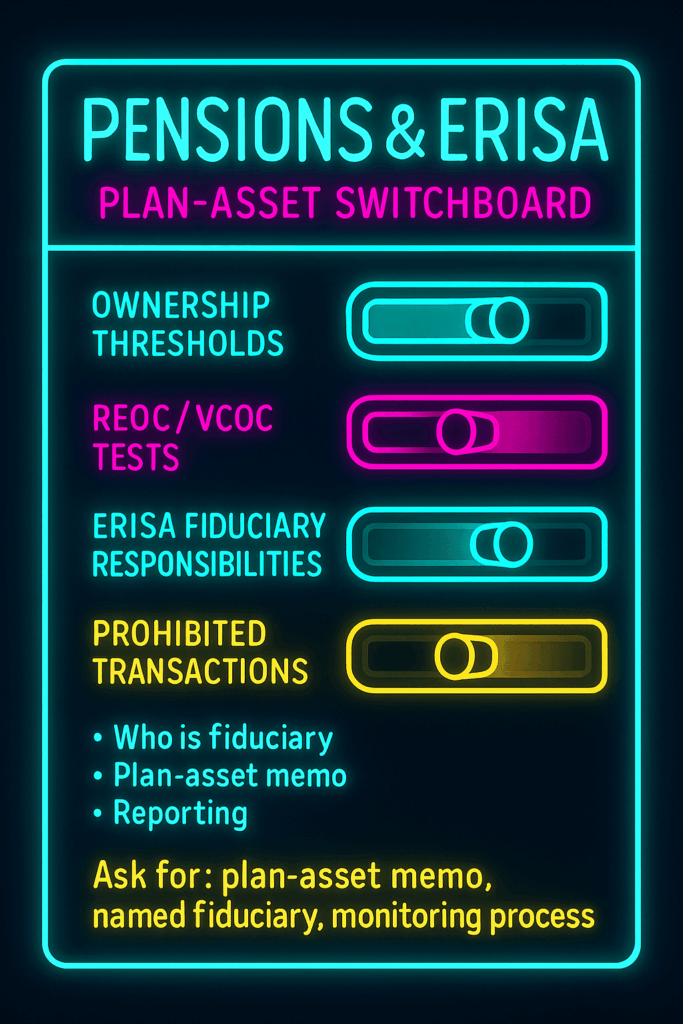

8) Pensions and ERISA money

When retirement plans invest, plan-asset rules and fiduciary responsibilities can apply. Many funds manage this by qualifying as a REOC/VCOC, staying under certain ownership thresholds, or structuring governance to handle ERISA duties.

What to do: If your dollars are plan dollars, ask for the fund’s plan-asset memo and who is on the hook as an ERISA fiduciary.

Red flags (and green lights)

Red flags: fees not spelled out in the LPA; performance shown only gross of fees; manager-calculated NAVs without an administrator; related-party deals with no offsets; vague appraisal policies; no covenant dashboard.

Green lights: independent admin calculating NAV and capital accounts; audited waterfalls; LPAC minutes showing real oversight; appraisal variance analysis; clear wire-approval workflows; timely, consistent reporting.

Bottom line

Investor protection in real estate funds isn’t one rule—it’s a system. Read the documents, verify the controls, and insist on independent eyes where money moves and values are set. Do that, and you’ll distinguish polished marketing from durable stewardship—so your capital is treated with the care a long-lived property deserves.

{kind=link}