This Content Is Only For Subscribers

Buying a business across borders is part finance, part diplomacy, and part logistics. The reward can be huge—new markets, talent, and cost advantages—but the rulebook gets thicker the minute a transaction crosses a border. If you’re newer to private equity (PE), this guide lays out the moving pieces in plain English so you can spot risks early and keep the deal on schedule.

Step 1: Map the deal perimeter

Start by drawing a simple picture:

- Where is the target incorporated? Company law drives shareholder approvals, financial statements, and board processes.

- Where does it operate? Each country adds employment, tax, privacy, and licensing rules.

- Who is buying? The identity and nationality of the acquiring entities (and their owners) matter for national security and foreign-investment screening.

- What percentage? Control vs. minority can flip which filings and approvals you need.

This one-page “deal map” becomes your checklist for merger control, foreign direct investment (FDI) screening, sector licenses, labor notifications, and tax.

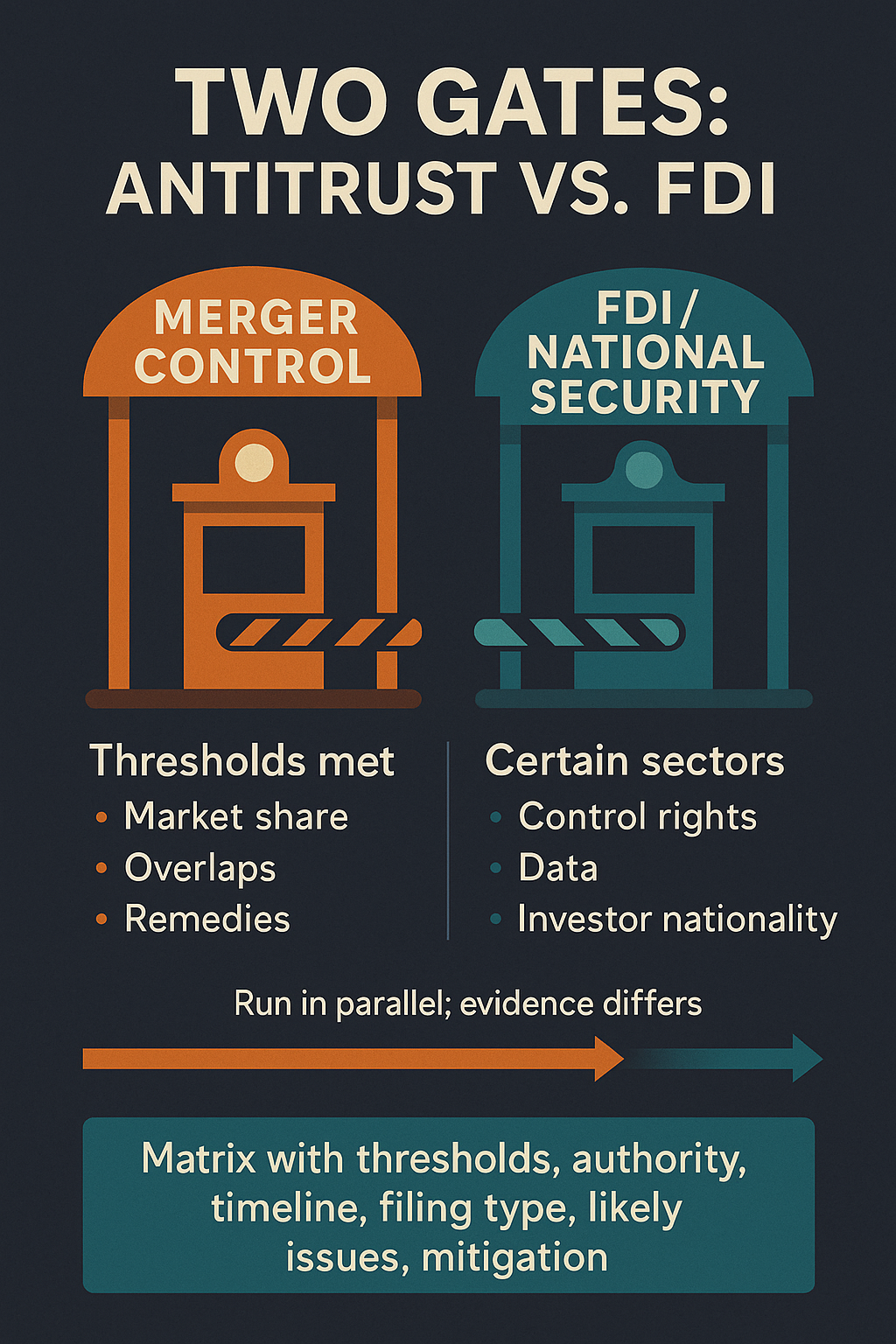

Step 2: Antitrust and FDI—two separate gates

Merger control (antitrust). Many countries require notification when deal size or revenue thresholds are met. Reviews focus on competition: market share, overlaps, and potential price effects. Approvals can be quick or require remedies (e.g., divestitures, behavioral commitments).

FDI/national security. Separately, governments examine whether foreign ownership threatens security or national interests—especially in tech, energy, healthcare, data-heavy businesses, or critical infrastructure. Triggers can include control, board seats, access to sensitive data, or certain investor nationalities. In practice, you often run antitrust and FDI reviews in parallel, but their clocks and evidence needs differ.

Practical tip: Build an approval matrix with filing thresholds, decision makers, statutory timelines, and whether a mandatory or voluntary filing makes sense. Add two columns: “likely issues” and “proposed mitigation.”

Step 3: Data, sanctions, and export controls—hidden tripwires

Data and privacy. Targets with consumer, health, or geolocation data may trigger rules that affect diligence (clean-team protocols), transfer of personal data between countries, and post-close obligations. Expect cross-border data-transfer assessments and sometimes a separate remediation plan (anonymization, minimization, or new vendor contracts).

Sanctions and restricted parties. You’ll screen investors, lenders, and counterparties and check where products go. If the target sells into sanctioned regions or customers, you may need carve-outs, new compliance systems, or a different go-to-market model.

Export controls. Advanced tech, encryption, dual-use goods, and telecom can require licenses for shipments or “deemed exports” (e.g., access by foreign nationals). This is often what turns a “low-risk” deal into a “high-process”one.

Step 4: Employment, works councils, and culture

Outside the U.S., labor law can drive the timeline. In parts of Europe and Latin America, works councils or unions must be informed or consulted before closing or before implementing post-close changes. Some jurisdictions require that employee liabilities transfer automatically in a business sale. Bake in time for these steps and align messaging early—regulators notice when workforce issues are an afterthought.

Step 5: The tax box diagram

Cross-border tax isn’t a footnote—it’s the model. Common elements:

- Holding company location to access treaty benefits and reduce withholding on dividends, interest, and gains.

- Financing mix (debt vs. equity) considering interest-limitation rules and thin-cap tests.

- Step-up in basis to create future amortization where possible.

- Blockers to manage UBTI/ECI for certain investors or to simplify local filings.

- Exit paths modeled upfront (asset sale, share sale, or merger) with expected character and withholding.

Ask for a sources & uses that includes all taxes and fees—stamp duties, transfer taxes, withholding, local advisors, and regulatory charges—so the real IRR is visible.

Step 6: Documentation strategy—one story, many languages

Your U.S. purchase agreement won’t fit everywhere. Expect:

- Local-law SPAs tailored to mandatory rules (price adjustment mechanisms, financial statement norms, liability caps).

- Representations and warranties insurance (RWI/W&I)—often helpful to bridge seller/ buyer risk appetites, but it won’t cover known issues or certain regulatory risks.

- Conditions precedent for antitrust/FDI approvals, sector licenses, and financing. Treat them like a Gantt chart with critical paths.

Clean teams for competitively sensitive data and ring-fenced diligence for export-controlled material keep regulators comfortable and reduce gun-jumping risk.

Step 7: Integration (start now, not “after close”)

Integration planning is a regulatory tool, not just an ops exercise. Build a Day-1/Day-100 plan that respects gun-jumping limits (no control before approvals) yet lines up the moves you can make immediately: change-of-control notifications, contract novations, IT access, data-mapping, and compliance upgrades. Have a short list of pre-clearancesteps for high-risk markets (licenses, data gateways, supply-chain rerouting).

Control, minority, and joint ventures

Control deals trigger the most filings and give you the most levers post-close. Minority investments can still be high-friction if they confer board seats, vetoes, or access to sensitive data. Joint ventures add governance complexity: who controls budgets, IP, hiring, and exits; what happens if partners deadlock; and how you manage information sharing across competitors.

If you’re investing in markets with foreign-ownership limits or variable-interest structures, expect extra scrutiny and plan for enforceable contractual protections plus an escalation path if laws shift.

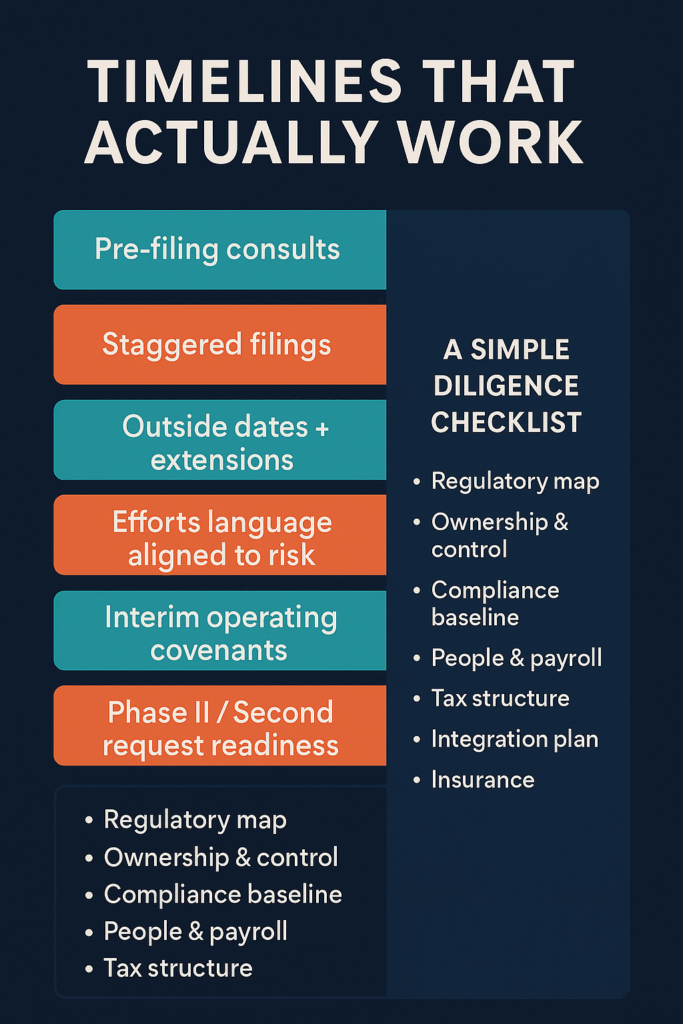

Timelines that actually work

A credible timetable includes:

- Regulatory pre-filing consults (where allowed) to test theories and mitigation.

- Staggered filings prioritized by the longest-lead jurisdictions.

- Outside dates with automatic extensions for slow reviews.

- Hell-or-high-water vs. efforts language aligned with your risk tolerance.

- Interim operating covenants that keep the business steady without straying into control.

Budget time for second requests/Phase II reviews in at least one key jurisdiction—plan the team and data rooms before the letter arrives.

A simple cross-border diligence checklist

- Regulatory map: Antitrust thresholds, FDI triggers, sector licenses, data/export issues; expected mitigation.

- Ownership & control: Ultimate beneficial owners, investor nationalities, board rights, information rights.

- Compliance baseline: Sanctions, anti-corruption, export, privacy—policies, audits, incidents, remediation.

- People & payroll: Works-council steps, retention plans, key contracts, immigration topics.

- Tax structure: Holding company, funding mix, step-ups, blockers, treaty positions, expected exit route.

- Contracts & IP: Change-of-control clauses, IP ownership and registries, software export or encryption issues.

- Financial plumbing: Cash management, trapped cash, transfer-pricing, intercompany agreements.

- Integration plan: Day-1 controls, IT and data access, customer and vendor communications, brand strategy.

- Insurance: RWI/W&I scope and exclusions; local insurance lines (D&O, cyber) post-close.

Bottom line

Cross-border PE deals succeed when teams sequence the approvals, control sensitive data, design the tax and financing box early, and build integration plans that regulators trust. You don’t need to memorize every statute; you need a map, a calendar, and advisors who can justify the plan in plain terms. Get those right, and the world gets smaller—without your closing timetable doing the same.

{kind=link}