This Content Is Only For Subscribers

Private equity (PE) can seem like a club with its own language: GP/LP, HSR, AIFMD, Form PF, VCOC. But beneath the acronyms sits a clear idea: long-term investors buying meaningful stakes in companies to create value and eventually sell. If you’re a novice investor curious about how PE is actually regulated—who the referees are, what disclosures exist, where the tripwires hide—this guide gives you the big picture in plain English.

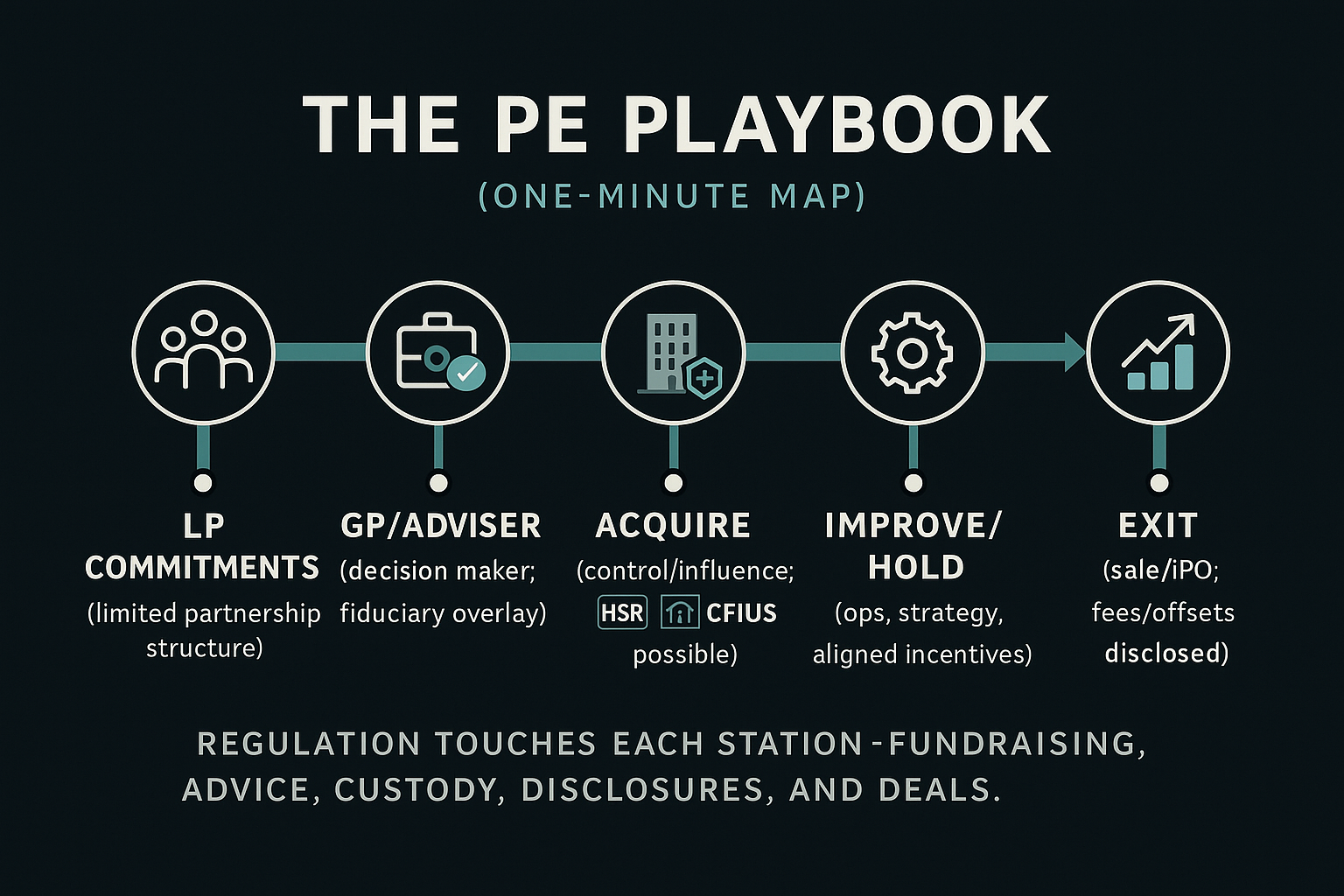

The PE Playbook, in One Minute

Most PE funds are limited partnerships. Investors (limited partners, or LPs) commit capital to a general partner (GP) who makes investment decisions, usually advised by a management company (the investment adviser). Funds buy controlling or influential stakes, hold them for several years, then exit via a sale or IPO. The value proposition: operational improvements, strategic focus, and aligned incentives.

Regulation touches every part of that journey—how funds raise money, how advisers behave, how fees are charged, how companies are bought and sold, and how cross-border risks are handled. It’s not one rulebook; it’s a stack.

The U.S. Core: Advisers Act Oversight

In the United States, regulation of private equity largely flows through the Investment Advisers Act of 1940—which governs the adviser (the management company behind the GP), not the fund entity itself.

Registration (or Exempt Reporting)

Most sizable PE advisers register with the U.S. Securities and Exchange Commission (SEC) as investment advisers. Some smaller or narrowly scoped advisers use exemptions and register on a limited basis as Exempt Reporting Advisers (ERAs). Either path brings obligations—especially around anti-fraud, truthful marketing, and managing conflicts.

Fiduciary Duty

Registered advisers owe clients (including pooled vehicles) a fiduciary duty of care and loyalty. In practice: act in investors’ best interests, disclose and manage conflicts, and maintain accurate books and records. This duty underpins everything else—valuation, fees and expenses, co-investments, and marketing claims.

Policies, CCO, and Exams

Advisers must adopt written policies and procedures, appoint a Chief Compliance Officer (CCO), and expect periodic SEC examinations. Examiners test whether controls work in real life—reviewing emails, marketing materials, expense allocations, valuation memos, and more. Exams often end with a deficiency letter that the adviser must remediate.

Marketing and Performance

Today’s marketing rules allow testimonials, endorsements, and third-party ratings with conditions, and require fair, balanced performance presentation. Hypothetical/model performance demands extra safeguards and audience controls. If a manager states a statistic, they should be able to prove it.

Custody and Audits

Because PE advisers typically have authority over fund assets, custody safeguards apply. Many funds satisfy these by delivering annual audited financial statements to investors through an independent public accountant; others undergo surprise exams. The aim is simple: protect investor money.

Form ADV and Form PF

- Form ADV (public) describes the adviser’s business, fees, conflicts, and key people in plain English.

- Form PF (non-public) gives regulators risk data across private funds—leverage, liquidity, and exposures. You won’t read it as an LP, but it feeds systemic-risk monitoring.

What Regulators Watch Inside a PE Firm

Fees and Expenses

PE has plenty of line items: management fees, carried interest, monitoring or transaction fees at portfolio companies, broken-deal costs, fund-level expenses (legal, admin, cyber, data). Regulators focus on what investors were toldversus what actually happened. Expect scrutiny of:

- Allocation of shared costs across funds and co-investments

- Fee offsets and rebates (e.g., offsetting portfolio-company fees against management fees)

- Accelerated monitoring fees or termination fees at exits

- Expense caps and disclosures

Valuation

Fair value matters because it drives performance reporting and, sometimes, fees. PE valuation policies typically cover methodology, use of third-party inputs, calibration to transaction prices, and oversight via a valuation committee. Back-testing (comparing realized exits to prior marks) is a healthy sign.

Conflicts of Interest

Conflicts are normal in PE—multiple funds pursuing similar deals, GP-owned service providers, cross-fund investments, stapled secondaries, and co-investments. The standard isn’t “no conflicts,” it’s identify, disclose, monitor, and mitigate. Look for documentation: conflict memos, allocation policies, committee minutes.

Co-Investments and Side Letters

LPs often negotiate co-investment rights (investing directly alongside the fund) and side letters (special terms like reporting or fee breaks). Many managers use most-favored-nation (MFN) processes so similarly situated investors can elect comparable terms. The keys are transparency and clean administration.

Cybersecurity and Vendor Risk

Advisers rely on administrators, cloud providers, and data vendors. Mature programs include multi-factor authentication, access reviews, vendor due diligence (e.g., SOC reports), incident-response plans, and tabletop exercises. Cyber is no longer “IT’s problem”; it’s an investor-protection issue.

Deal-Level Rules: Buying and Selling Companies in the U.S.

Antitrust: HSR Act

Mergers and acquisitions above certain thresholds require a pre-merger filing under the Hart-Scott-Rodino (HSR) Act and a waiting period while the FTC and DOJ review potential competition issues. Thresholds are adjusted annually. “Gun-jumping” (acting as owner before clearance) is a real risk—clean teams and integration planning protocols help.

National Security: CFIUS

The Committee on Foreign Investment in the United States (CFIUS) can review deals that could pose national-security concerns, especially when a foreign investor is involved and the target touches critical technologies, infrastructure, or sensitive personal data. Mandatory filings can be triggered in some tech areas. Even U.S.-led funds with non-U.S. LPs should consider governance structures that keep foreign “control” below sensitive thresholds.

Public-to-Private Transactions

Taking a public company private triggers additional securities-law obligations (tender-offer rules, going-private disclosures). Timing, financing certainty, and conflicts (e.g., management rollovers) receive close attention.

Sector-Specific Rules

Healthcare, financial services, energy, telecom, and defense bring added licensing or ownership restrictions. Good counsel will map these early; surprises late in a process are expensive.

Investors with Special Rules: ERISA and the “Plan Asset” Puzzle

U.S. pension plans and other ERISA investors bring their own layer of regulation. Funds commonly structure themselves to avoid being deemed to hold “plan assets” (which would subject the GP to ERISA fiduciary obligations) by relying on the VCOC (venture capital operating company) or REOC (real estate operating company) exceptions, or by keeping benefit-plan investor participation below regulatory thresholds. If a fund does become a plan-asset vehicle, the adviser must follow ERISA’s fiduciary and prohibited-transaction rules—serious commitments requiring specialized controls.

Beyond the U.S.: The Global PE Map

Private equity is global, so are the rulebooks. Three themes dominate abroad: who can market to whom, how managers are supervised, and what approvals a deal needs.

Europe and the UK

- AIFMD (EU). The Alternative Investment Fund Managers Directive governs managers of alternative funds (including PE) across the EU. It covers authorization, capital, risk management, valuation oversight, depositaries (akin to custodians), disclosure to investors, and regulatory reporting. EU-based managers generally need full authorization; non-EU managers often rely on national private placement regimes (NPPR) to market to professional investors country by country.

- MiFID adjacency. While MiFID focuses on investment firms and conduct of business rules, it shapes distribution practices and investor classification (e.g., professional vs. retail).

- UK (post-Brexit). The UK runs a similar but separate regime for alternative managers, with familiar concepts on authorization, disclosure, and reporting.

- Merger control & FDI screening. The European Commission and national authorities run merger control. Many countries (France, Germany, Italy, Spain, among others) also screen foreign direct investment (FDI) in sensitive sectors. Expect filings and remedies on both competition and national-interest grounds.

Asia-Pacific

- China. Foreign investments can trigger antitrust review (SAMR), national-security review, and sector caps; outbound investments by Chinese parties face separate oversight. Data and cybersecurity rules add complexity for targets handling personal or important data.

- India. Sectoral caps and approval routes apply under the FDI policy; merger control thresholds apply under the Competition Act.

- Singapore & Hong Kong. Both operate sophisticated fund regimes (e.g., Singapore’s VCC structure; Hong Kong’s LPF regime) and are popular hubs for Asia strategies. Marketing is typically limited to professional investors with local filings or licenses.

- Australia, Japan, Korea, others. Each runs its own mix of merger control and FDI screening; filings can be mandatory even for minority stakes if sensitive sectors are involved.

Canada and Other Jurisdictions

Canada blends Competition Act merger control with Investment Canada Act reviews (net benefit or national security). In Latin America and the Middle East, merger control and FDI screening are evolving quickly; local counsel is essential.

Universal Threads Across Borders

AML/KYC and Sanctions

No matter the jurisdiction, expect anti-money-laundering and know-your-customer checks on investors, plus sanctions screening on investors, portfolio companies, and counterparties. Documentation of source of funds is routine. Sanctions regimes (U.S., EU, UK, UN and others) change frequently; screening is continuous, not one-and-done.

Anti-Corruption

Cross-border deals bring exposure to the U.S. Foreign Corrupt Practices Act and the UK Bribery Act, among others. Diligence around intermediaries, state-owned counterparties, gifts and hospitality, and charitable contributions matters—especially in high-risk markets. Strong compliance programs train portfolio-company leadership and embed controls post-close.

Privacy and Data Protection

Target companies that process personal data can trigger GDPR in Europe, UK GDPR, CCPA/CPRA in California, and a growing list of state or national privacy laws. Data-room redactions, clean teams, and data-transfer assessments are now standard workstreams in diligence.

ESG and Sustainability Expectations

Even when not mandated, investors often ask managers to report on climate, workforce, governance, and supply-chain risks. Europe’s SFDR and related rules influence disclosures globally because many LPs allocate worldwide. The trend line: more standardized reporting, clearer claims, and careful use of ESG data in marketing.

How Funds Raise Capital: Offering and Distribution Rules

United States

PE funds typically raise capital through private placements under the Securities Act (e.g., Regulation D). Some offerings ban general solicitation (506(b)) and rely on pre-existing relationships; others allow broader marketing (506(c)) but require verification that investors meet eligibility standards (often “accredited” or institutional). Managers also comply with state “blue sky” notice filings.

Europe/UK and Elsewhere

Marketing to professional investors is regulated. In the EU, the AIFMD framework dictates how, when, and to whom a manager can market; many non-EU managers use NPPR. The UK has its own regime. In Asia-Pacific and the Middle East, “professional investor” or “institutional” categories control the playbook, and pre-marketing/marketing notifications are often required.

The practical takeaway: distribution is local. Big global raises are staged, with counsel coordinating filing calendars and investor communications across regions.

Accounting, Reporting, and Governance: What Good Looks Like

- Fair-Value Accounting. U.S. GAAP ASC 820 and IFRS fair-value standards anchor valuation. Policies describe methodologies, calibration, and frequency; controls include independent reviews and committee oversight.

- Independent Administration and Audit. Many PE funds use third-party administrators for capital accounts and cash controls, and deliver annual audits to investors through recognized audit firms.

- LP Reporting Rhythm. Quarterly letters, capital account statements, fee and expense disclosures, and an annual meeting or ESG review are common. Many managers reference industry templates to standardize how fees, expenses, and performance are shown.

- Governance Discipline. Board or LP advisory committee (LPAC) minutes, conflict logs, valuation committee records, and incident-response reports are part of a healthy paper trail.

Practical Investor Questions to Ask

- Registration status: Are you SEC-registered or an ERA? What does your compliance program look like (CCO, annual review, testing)?

- Fees and offsets: How do portfolio-company fees (monitoring, transaction) flow back to the fund? What’s the offset policy?

- Valuation: Who sits on the valuation committee? How do you calibrate to transaction prices and perform back-testing?

- Conflicts: How do you allocate deals among funds and manage cross-fund transactions and co-investments?

- Cyber and privacy: What’s your incident-response plan? Do you conduct tabletop exercises? How do you assess vendor risk?

- Deal approvals: On a typical control deal, what merger control, FDI, or national-security filings do you anticipate?

- LPAC and side letters: How are side letters administered? Do similarly situated investors have MFN options?

- Global marketing: In which jurisdictions are you authorized to market? What reporting do you provide to non-U.S. LPs?

- ERISA: Do you rely on VCOC/REOC or another approach to manage plan-asset risk?

- Audit and admin: Who is your auditor and administrator? How long have they served, and how do you evaluate them?

You’re listening for fluency, documents to back up claims, and policies that match practice.

The Big Picture

Regulation of private equity isn’t a single gate—it’s a network. In the U.S., the Advisers Act sets the tone: fiduciary duty, exams, marketing discipline, custody safeguards, and clear disclosures. Around the world, AIFMD-style regimes, merger control, FDI screening, anti-corruption laws, sanctions, and privacy rules shape how deals are done and how managers raise capital. The through-line for investors is simple: look for alignment (between disclosures and behavior), controls (that actually operate), and clarity (in fees, valuation, conflicts, and reporting).

Get those right, and the acronyms start to make sense—not as barriers, but as the scaffolding that lets private equity do what it does best: concentrate effort, compound improvements, and create value over time.

{kind=link}