This Content Is Only For Subscribers

Hedge funds live in a “private market” neighborhood with locked gates. Those gates aren’t about snobbery; they’re built from SEC rules that limit who can invest in private offerings. If you’re curious about whether you qualify—and how access actually works—this guide breaks it down in plain English.

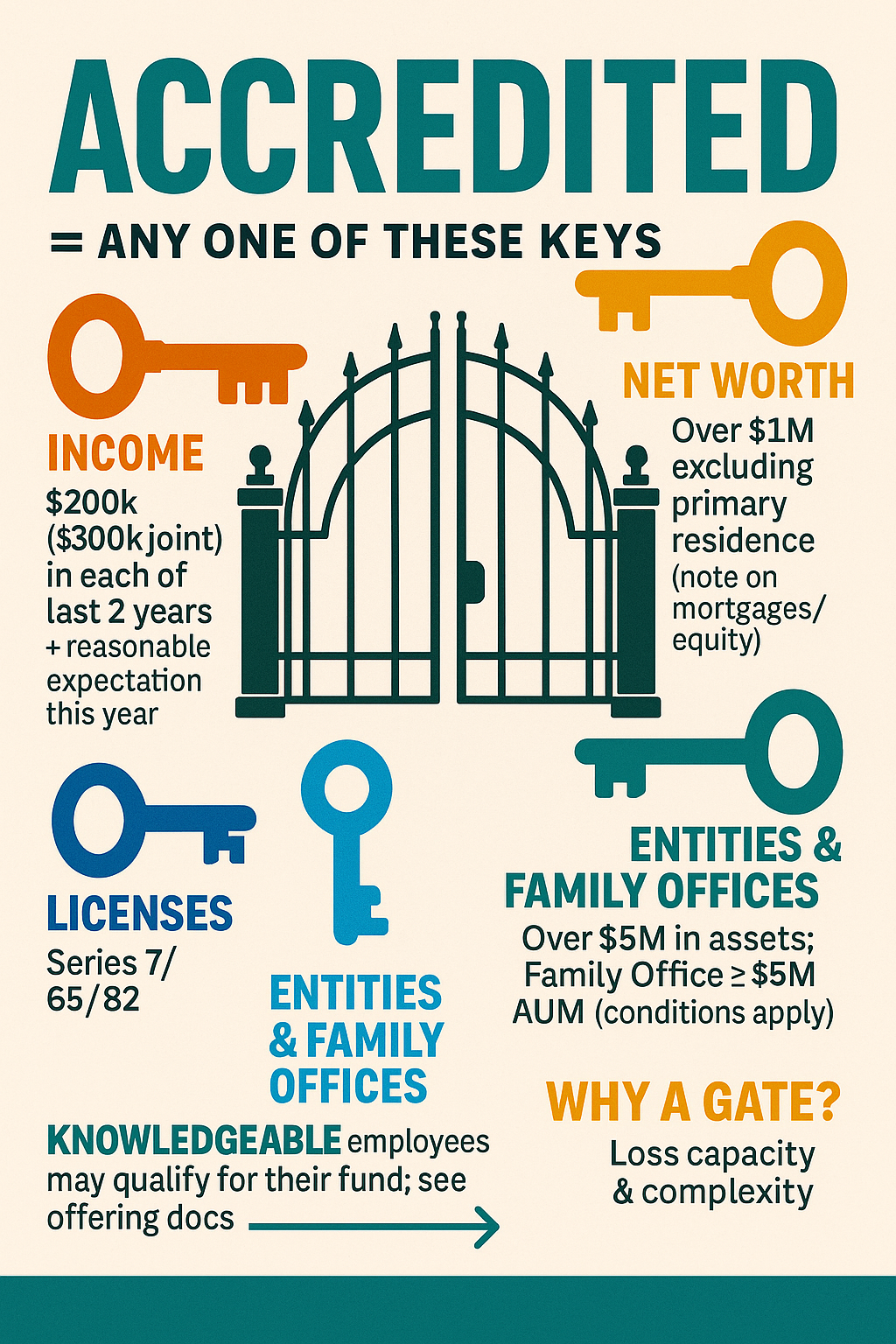

What “Accredited Investor” Means (in practice)

The SEC’s “accredited investor” definition sits inside Regulation D and spells out who’s eligible to buy into most private fund offerings. You don’t need to meet all of the criteria—one pathway is enough. The most common:

- Income test: Individual income of $200,000 (or $300,000 joint with a spouse or spousal equivalent) in each of the last two years, with a reasonable expectation of the same this year.

- Net-worth test: Over $1 million in net worth excluding your primary residence (mortgage details matter; the home’s equity doesn’t count).

There are also non-wealth routes:

- Licenses: Certain professional certifications (e.g., Series 7, Series 65, Series 82) qualify you personally.

- Entities: Corporations, LLCs, or trusts with over $5 million in assets may qualify; Family Offices with $5 million under management (and their family clients) can qualify too, subject to conditions.

- Knowledgeable employees: In a private fund context, certain employees may invest on preferential eligibility grounds (this helps with employee alignment—details live in fund docs).

Why the gate exists: Private funds aren’t sold like mutual funds. They can use complex strategies and disclose risks differently. The accredited standard is meant to ensure investors can bear losses and understand the tradeoffs.

How Qualification Gets Checked

How your status is verified depends on how the fund markets:

- Quiet raise (Rule 506(b)): The fund can’t generally solicit the public. It often relies on your self-certification(typically a signed questionnaire), and the manager must have a “pre-existing, substantive relationship.”

- Public-facing raise (Rule 506(c)): The fund can market broadly, but must take reasonable steps to verifyyou’re accredited. Expect document requests—W-2s, K-1s, brokerage statements, a letter from a CPA/attorney, etc. A simple checkbox isn’t enough under 506(c).

Pro tip: If privacy matters, ask whether a third-party verification service can review documents instead of the manager. Most serious platforms use them.

“Accredited” ≠ “Qualified Purchaser” (and why that matters)

You’ll sometimes hear “qualified purchaser” (QP) mentioned alongside accredited investor. They’re not the same. QP status (under the Investment Company Act) generally requires $5 million (individuals) or $25 million (institutions) in investments and ties to a different exemption hedge funds use to avoid mutual-fund-style registration. Some funds accept only QPs; others accept accredited investors. Read the term sheet carefully so you’re not surprised at the last step.

Paths to Hedge Fund Access

Once you’re accredited, how do you actually get in? Common routes:

- Direct subscription into a private fund

Classic path: you subscribe to a partnership or LLC interest, often with a minimum (e.g., $250k, sometimes lower/higher). Expect lockups, notice periods for redemptions, and the possibility of gates or suspensions in stressed markets. - Feeder funds and platforms

Aggregator vehicles (“feeders”) collect capital from many accredited investors and invest into a master hedge fund, sometimes lowering minimums. Online platforms curate feeders or direct allocations, handle verification, and centralize subscription paperwork. - Registered “interval” or tender-offer funds (’40 Act alternatives)

A growing slice of strategies are packaged in semi-liquid, registered funds with periodic repurchase windows. They won’t mirror a classic hedge fund’s freedom, but they broaden access and improve reporting cadence. Minimums can be lower and may be open to non-accredited investors depending on structure—but fees and liquidity terms still vary widely. - Secondary interests

You may buy existing investor interests from someone seeking liquidity, typically via specialized brokers or platform auctions. Discounts and transfer restrictions apply; documents are dense. - Private wealth channels

Many private banks and RIA networks offer lists of diligenced funds, often negotiating better terms (or at least better information flow). Minimums and eligibility still apply.

What the Subscription Process Feels Like

Expect a PPM (private placement memorandum), LPA/LLC agreement, and subscription docs. You’ll fill out an investor questionnaire, complete AML/KYC, and provide tax forms (e.g., W-9 or W-8BEN). Capital may be called on specific dates, with the first valuation cut after month-end. Ongoing, you’ll receive monthly or quarterly statements, capital account reports, K-1s at tax time, and annual audited financials if the fund uses that custody pathway.

Fees, Liquidity, and Other Tradeoffs

Hedge funds typically charge a management fee (e.g., 1–2% annually) and a performance fee (e.g., 10–20% of profits, often with a high-water mark). Fees should align with the strategy’s complexity and expected alpha.

Liquidity is not daily. Common setups include:

- Lockups: No redemptions for an initial period (e.g., 12–24 months).

- Redemption windows: Quarterly or semiannual with advance notice (30–90 days).

- Gates/side pockets: Tools for unusual market stress or illiquid assets; they must be disclosed in advance.

Make sure asset liquidity matches investor liquidity. It’s a red flag if a fund with hard-to-sell assets promises easy exits.

Risks You Should Actually Underwrite

- Strategy drift: Is the manager sticking to the stated playbook? Read the risk and “use of leverage/derivatives” sections closely.

- Valuation: For illiquid positions, how are marks set? Independent pricing? Valuation committee?

- Conflicts of interest: Multiple funds, cross-trades, affiliated service providers—how are conflicts disclosed and handled?

- Operational strength: Who’s the administrator and auditor? Are financials audited annually and delivered on time?

- Cybersecurity/vendor risk: Ask (briefly but directly) about MFA, data access reviews, and vendor diligence.

Taxes and Account Fit

Many hedge funds are partnerships that issue Schedule K-1s. That can mean late-arriving tax documents and pass-through items (including potential unrelated business taxable income if leverage is used, depending on structure). If you’re allocating through a retirement account, ensure the vehicle is designed for it and ask about UBTI. Always align allocations with your overall plan—hedge funds should complement, not dominate, a diversified portfolio.

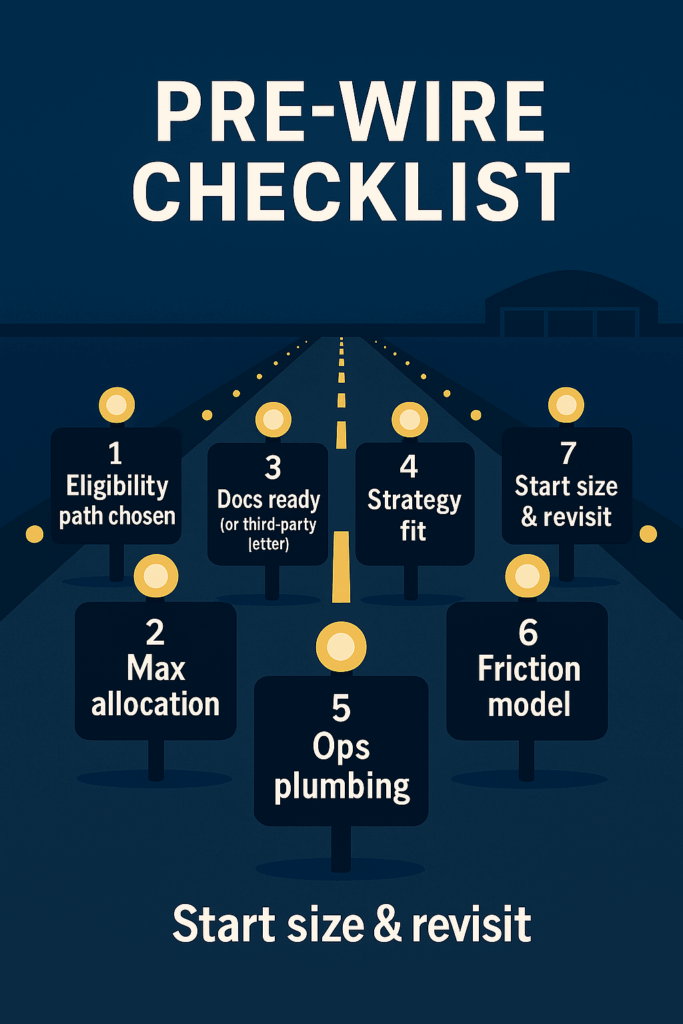

How to Prepare (a mini-checklist)

- Confirm eligibility: Decide whether you’ll qualify via income, net worth, or license, and line up documentation.

- Set a max allocation: Decide your private-fund sleeve before you look at glossy decks.

- Screen for fit: Strategy, volatility tolerance, liquidity terms, and reporting cadence.

- Diligence the plumbing: Administrator, auditor, custody pathway, valuation controls, and recent exam history.

- Model the frictions: Fees, gates, tax reporting, and operational timelines (capital calls, K-1s).

- Start small, learn fast: Consider beginning at the lower end of minimums (via feeders or platforms) while you build comfort.

Bottom Line

“Accredited investor” status is just the key—it doesn’t guarantee a great house behind the gate. The real edge comes from matching your goals to the right structure, understanding liquidity and fees, and verifying that a manager’s operations are as strong as the slide deck. Do that, and hedge fund access can be a useful tool—not a leap into the unknown.

{kind=link}