This Content Is Only For Subscribers

Private credit may feel like one big asset class, but it’s actually a patchwork of distinct regional markets. The United States dominates in size and maturity, Europe has become a formidable second engine, and Asia-Pacific plus select emerging markets are the growth frontier. For investors, those differences matter: they shape risk, return, documentation, and how you actually access deals.

Below is a field guide to the similarities and contrasts—organized around the things investors care about most.

1) Market Structure and Maturity

United States.

The U.S. is the epicenter of private credit: deep manager rosters, large pools of institutional capital, and a long track record in sponsor-backed lending. Direct lenders routinely finance multi-hundred-million and even multi-billion dollar transactions, sometimes replacing entire bank syndicates. Competition is intense, but underwriting and monitoring practices are highly institutionalized, with robust sponsor relationships and specialized sector teams.

Europe (UK, DACH, Benelux, Nordics, France, Italy, Spain).

Europe is the clear number two. Bank lending remains important, but regulatory capital pressures and a shift toward club deals have opened the door for direct lenders. Activity is concentrated in the mid-market and upper mid-market, and ESG-linked features are more common in loan documentation. Complexity rises because each country has its own legal nuances, insolvency regimes, and labor protections.

Asia-Pacific (Japan, Australia, India, Southeast Asia) & Emerging Markets.

APAC private credit is expanding from a smaller base. Japan and Australia are the most institutionalized; India and Southeast Asia have strong demand but uneven legal enforcement and data transparency. In Latin America and parts of Africa, opportunity often comes with higher political, currency, and documentation risk. Quality local partners and careful structuring are essential.

Investor takeaway: The U.S. offers scale and standardization; Europe provides breadth with stronger ESG integration; APAC/EM can add growth and yield—but require more selectivity and partner diligence.

2) Borrower Profile and Deal Flow

U.S.: Predominantly sponsor-backed mid-market companies (EBITDA typically $25–$200M), but large-cap unitranche and structured solutions are now common. Sector diversity is high: software, healthcare services, business services, industrials, consumer, specialty finance.

Europe: Similar sponsor-backed core with a tilt to cross-border platforms and carve-outs. More frequent inclusion of margin ratchets tied to sustainability KPIs. Local bank relationships still influence capital structures—direct lenders often co-exist with banks.

APAC/EM: Mix of sponsor-backed and founder-owned borrowers; more asset-backed and trade-linked opportunities; growing NAV-loan and structured credit usage by regional PE managers. Deal flow can be episodic and concentrated in specific corridors (e.g., Australia infrastructure-adjacent corporates; Indian mid-market growth).

Investor takeaway: Sponsor ecosystems drive repeatable flow in the U.S. and Europe; in APAC/EM, origination is more relationship-driven and “lumpier,” favoring managers with strong local sourcing.

3) Instruments, Terms, and Documentation

U.S.: Senior secured unitranche loans dominate larger sponsor deals, with SOFR-based floating coupons, call protection, covenants (often “cov-lite” but tighter than syndicated markets), MFN protections, and robust reporting. Intercreditor and security packages are familiar and relatively standardized.

Europe: Senior/holdco mixes and unitranche are common. Documentation often embeds ESG-linked margin ratchets, information undertakings, and sometimes tighter maintenance covenants relative to equivalent U.S. credits. Enforcement paths vary by country, so lenders often emphasize security packages and local counsel opinions.

APAC/EM: Wider variety—senior secured loans, receivables-backed facilities, export/trade finance, and structured solutions (including NAV loans to local PE). Documentation quality ranges from top-tier to bespoke; enforcement and step-in rights depend heavily on jurisdiction and collateral type.

Investor takeaway: Expect the strongest standardization in the U.S., increasing harmonization in Europe, and bespoke/asset-backed structures in APAC/EM. Country legal risk is not a footnote—price it.

4) Pricing, Fees, and Return Drivers

U.S.: Competition among mega-managers can compress spreads at the top end, but lenders often recapture economics via OID (original issue discount), fees, and call protection. Floating-rate coupons pass through central-bank moves, creating attractive income in higher-rate environments.

Europe: Spreads are often a touch wider on comparable risk, reflecting cross-border complexity and tighter covenant packages. ESG margin ratchets can shave pricing for borrowers who hit sustainability milestones—an upside for outcomes, a small drag on nominal yield.

APAC/EM: Headline yields can be higher, but adjust for FX, legal, and execution risk, plus higher monitoring intensity. Asset-backed deals may carry attractive coupons but require specialist underwriting and active collateral management.

Investor takeaway: U.S. for efficient carry; Europe for slightly higher spreads with stronger covenants; APAC/EM for enhanced yields—if you have the right manager and risk controls.

5) Regulation, Oversight, and Systemic Considerations

U.S.: Post-GFC bank rules contributed to nonbank growth; current conversations focus on data transparency, leverage, and the interlinkages between banks and private funds. Publicly listed BDCs (business development companies) provide one retail-accessible channel with their own regime.

Europe: Regulatory dialogue is shaped by EU and UK frameworks. Disclosure expectations around sustainability are more developed, influencing how managers report ESG metrics and how borrowers commit to improvements.

APAC/EM: Patchwork. Australia and Japan offer clarity; India has active credit-market reforms; Southeast Asia and Latin America vary widely. Policy shifts can be material to underwriting and exits.

Investor takeaway: Oversight is heaviest (and most codified) in the U.S. and EU/UK; elsewhere, rely on manager governance and legal structuring to bridge gaps.

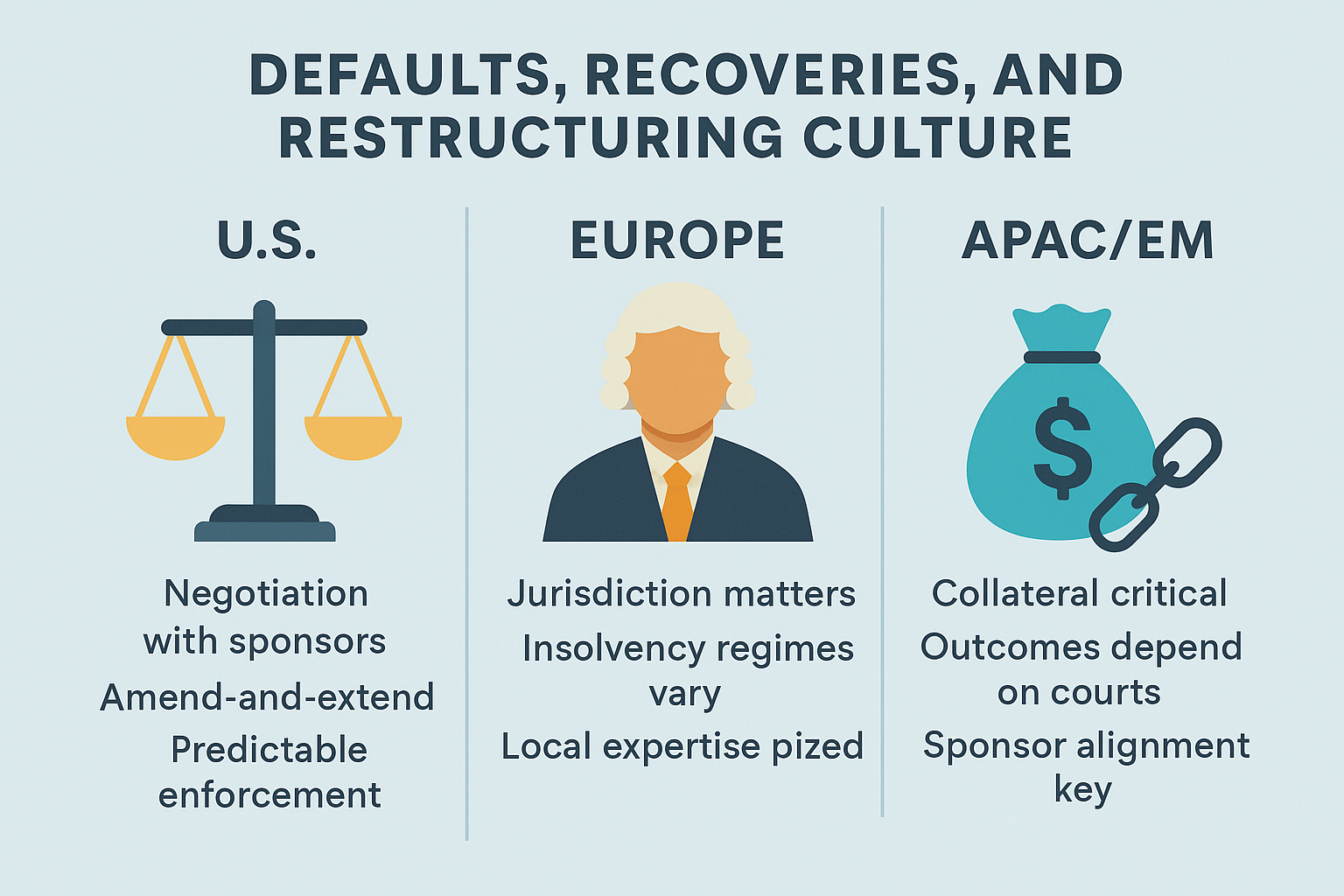

6) Defaults, Recoveries, and Restructuring Culture

U.S.: Restructuring playbooks are well-trodden. Private lenders often negotiate directly with sponsors, using amendment-and-extend, additional equity, or priming facilities to preserve value. Recoveries benefit from predictable bankruptcy courts and lien enforcement.

Europe: Tools vary by jurisdiction (e.g., UK schemes/Part 26A plans; different insolvency regimes across EU). Lenders prize early engagement and local expertise; recoveries depend heavily on forum and collateral.

APAC/EM: Outcomes hinge on collateral type, courts, and sponsor alignment. Asset-based structures with strong control features (cash dominion, share pledges, offshore holding structures) can materially improve recovery prospects.

Investor takeaway: The same credit can have different recovery profiles purely because of where it is domiciled. Jurisdiction is a risk factor—treat it as such.

7) ESG Integration

U.S.: ESG adoption is manager-specific—widely practiced, but not uniform. Many lenders incorporate negative screens and basic KPI tracking; sustainability-linked pricing is growing, but not yet universal.

Europe: ESG is more deeply embedded. Margin ratchets tied to emissions, energy intensity, or governance milestones are common, as are standardized reporting templates. Borrowers increasingly expect it.

APAC/EM: Mixed. Australia and Japan are advanced; other markets show rapid progress from a lower base. Data availability and verification can be challenges.

Investor takeaway: If ESG integration is a priority, Europe currently leads on documentation and reporting depth; top global managers are raising the bar elsewhere.

8) Currency, Hedging, and Liquidity

Currency (FX). Outside the U.S., FX can dominate realized returns—positively or negatively. Many funds hedge back to the investor’s base currency, but hedging costs eat carry and vary over time.

Liquidity. Closed-end funds are standard globally. “Evergreen” and semi-liquid vehicles are growing in the U.S. and Europe, but redemption gates and proration can apply. In APAC/EM, secondary markets for fund interests can be thinner.

Investor takeaway: Ask precisely how the manager hedges, at what tenor, and who bears basis risk. For liquidity, read the fine print—not just the brochure.

9) Access Vehicles and Manager Selection

- Public BDCs / listed vehicles (U.S., some Europe): Daily liquidity, mark-to-market volatility.

- Private drawdown funds: Classic 5–10 year life; vintage diversification matters.

- Evergreen/interval/tender-offer funds: Periodic liquidity with constraints; rising in wealth channels.

- Co-investments/SMAs: Scale and governance benefits for large allocators.

Manager questions to ask globally:

- Origination edge (sponsor relationships, sector depth, local sourcing).

- Underwriting discipline (leverage, covenants, stress tests).

- Monitoring & workout capabilities across jurisdictions.

- FX and liquidity policies.

- ESG process and data quality.

- Fund-level leverage and risk budgeting.

Putting It Together: Portfolio Construction Ideas

- Core income: U.S. senior direct lending for scale and predictability.

- Diversified Europe sleeve: Similar risk with slightly wider spreads and stronger covenants; add UK/Benelux/Germany exposure.

- Opportunistic growth: Select APAC/EM via top-tier local partners—focus on asset-backed or sponsor-backed structures with strong security and hedging.

- Structured solutions: A measured allocation to NAV lending or specialty finance (trade finance, royalties) for diversification—via managers with real track records.

- Vehicle mix: One closed-end fund per year for vintage spread, plus a small evergreen allocation for smoother pacing.

Final Thoughts

Private credit is not a monolith. The U.S. offers depth and speed; Europe brings discipline and ESG rigor; Asia-Pacific and emerging markets offer growth and yield—with added complexity. The best portfolios reflect that reality: they balance scale with selectivity, income with downside protection, and global reach with local expertise.

If you match the right manager to the right region and structure, the differences between markets aren’t a hurdle—they’re your edge.

{kind=link}