When it comes to saving for retirement, the Individual Retirement Account (IRA) is one of the most flexible and accessible tools available. But while opening an account is straightforward, understanding who is actually eligible to contribute can feel murky. Rules about earned income, spousal contributions, and income-based limits vary by IRA type — and the details matter, especially if you want to avoid penalties or missed opportunities.

This guide walks through IRA contribution eligibility in plain English so you can confidently determine whether (and how much) you can put aside for your future.

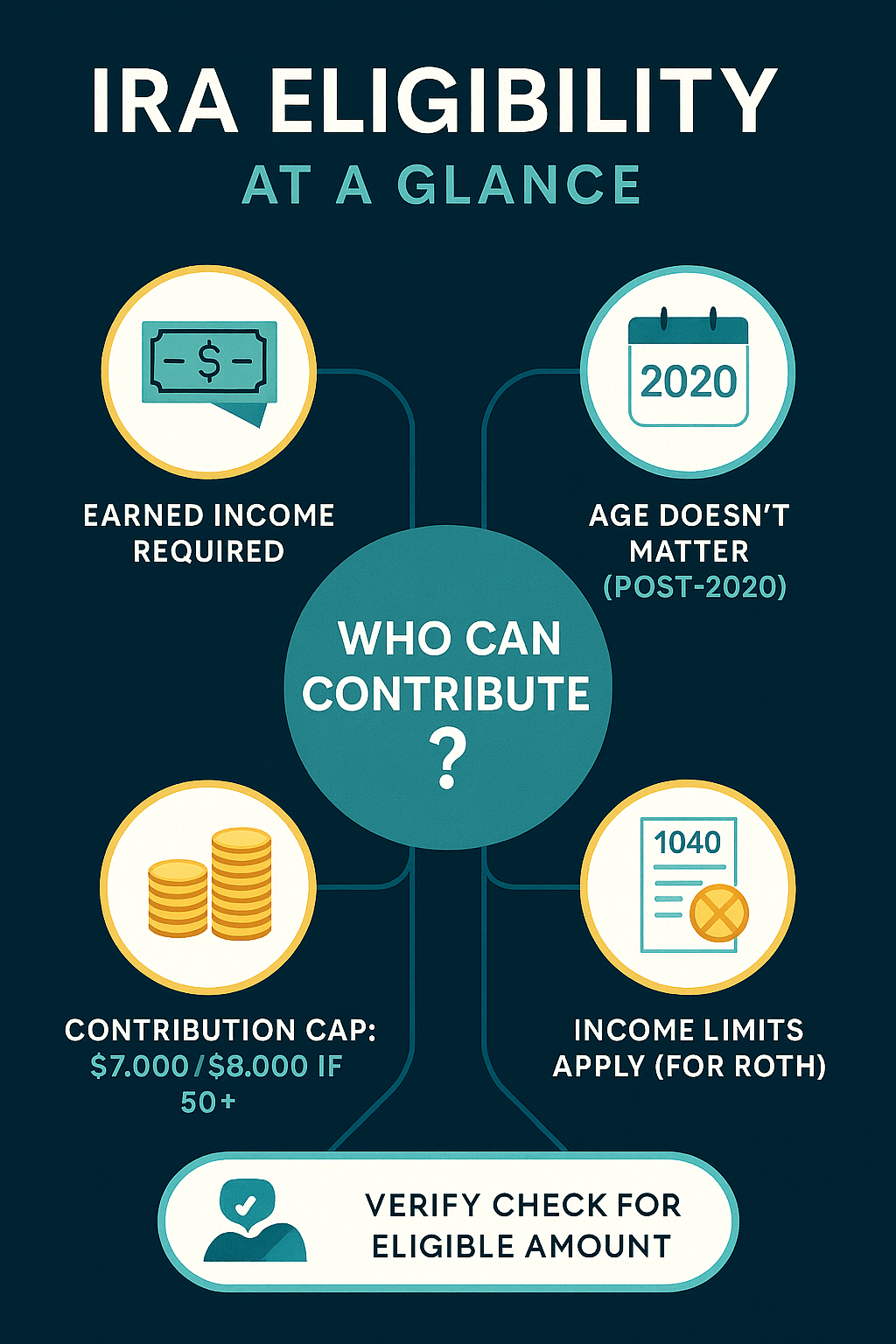

The Basic Rule: You Need Earned Income

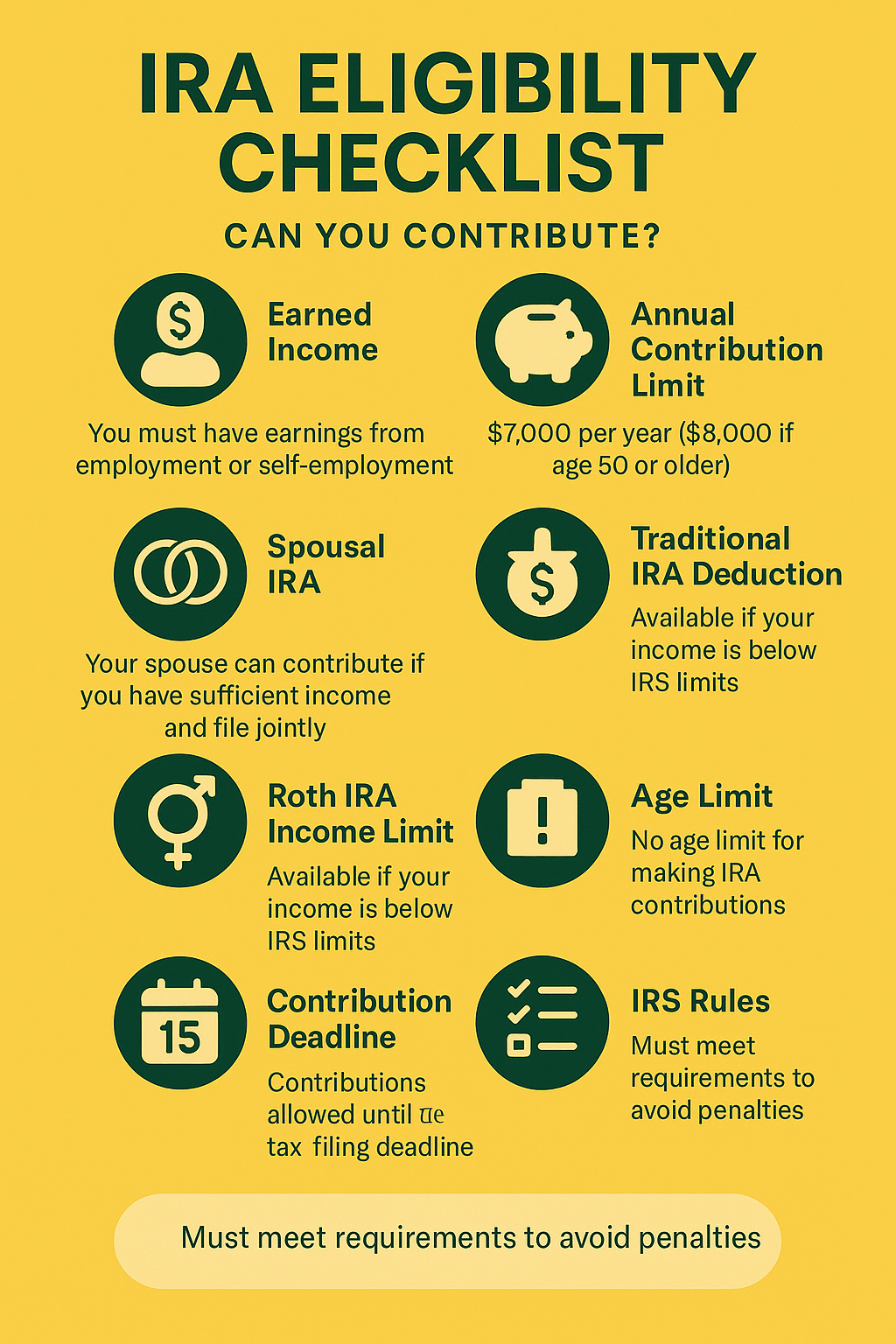

At the simplest level, you can only contribute to an IRA if you have earned income. That means money you make from work — wages, salary, tips, commissions, or self-employment income. Investment earnings, rental income, pensions, or gifts don’t count.

For 2025, the maximum annual contribution is:

- $7,000 if you’re under age 50

- $8,000 if you’re age 50 or older (thanks to a $1,000 “catch-up” provision)

You can’t contribute more than you earn. For example, if you made $4,000 in part-time wages, that’s the most you can put into an IRA for the year.

Spousal IRAs: A Special Exception

What if you don’t have earned income at all? Married couples filing jointly can use a spousal IRA, where the working spouse’s income is used to fund contributions for both spouses. The working partner needs enough earned income to cover both contributions, but otherwise, both IRAs follow the same rules. This provision ensures that stay-at-home parents or caregivers can still build retirement savings.

Traditional IRA Contribution Rules

Anyone with earned income can contribute to a traditional IRA, regardless of how much they make. However, your ability to deduct those contributions on your tax return depends on whether you (or your spouse) are covered by a workplace retirement plan and how much you earn.

For 2025, the IRS sets deduction phase-out ranges based on Modified Adjusted Gross Income (MAGI). For example:

- If you’re single and covered by a workplace retirement plan, your deduction begins to phase out in the mid-$70,000s and disappears in the high-$80,000s.

- If you’re married filing jointly and covered at work, the phase-out starts around the low-$120,000s and ends in the low-$140,000s.

- If only your spouse is covered by a plan, the phase-out is higher, generally in the mid-$200,000s.

Because these ranges change yearly, it’s best to confirm the exact thresholds on the IRS website or with your tax advisor before filing.

Roth IRA Contribution Rules

Roth IRAs come with income restrictions that determine whether you can contribute at all.

For 2025, the income thresholds are:

- Single / Head of Household:

- Full contribution allowed if your MAGI is less than $150,000

- Partial contribution if your MAGI is between $150,000 and $165,000

- No contribution if your MAGI is $165,000 or more

- Married Filing Jointly:

- Full contribution allowed if your MAGI is less than $236,000

- Partial contribution if your MAGI is between $236,000 and $246,000

- No contribution if your MAGI is $246,000 or more

If your income is too high for a Roth IRA, you may still have options through a backdoor Roth strategy, which involves contributing to a traditional IRA and then converting it. This approach is perfectly legal but comes with extra tax reporting requirements and potential complications if you already hold other pre-tax IRA balances.

Age Isn’t a Barrier Anymore

Before 2020, contributions to a traditional IRA stopped at age 70½. That rule is gone. Thanks to the SECURE Act, you can now contribute to a traditional or Roth IRA at any age, as long as you have earned income.

Contribution Deadlines

IRA contributions for a given tax year can be made up until the tax-filing deadline of the following year (usually April 15). For example, you can contribute for the 2025 tax year until April 15, 2026.

Final Thoughts

IRA contribution rules aren’t designed to trip you up — they’re meant to make sure the tax advantages go to people actively saving for retirement. Once you understand the basics — earned income, contribution limits, spousal IRAs, and the income thresholds for Roths and deductions — it becomes much easier to see where you fit.

If you’re just starting out, the most important step is simple: open an account and begin contributing, even if you can only put away a modest amount. Over time, the combination of steady deposits, tax advantages, and compounding can make a world of difference in your retirement security.

{kind=link}