When it comes to saving for retirement, two of the most common tools you’ll hear about are the Traditional IRA and the Roth IRA. On the surface, they look similar: both are individual retirement accounts that allow you to save and invest money for the future with special tax advantages. But dig a little deeper, and you’ll find important differences in how contributions, withdrawals, and taxes work. Understanding these differences can help you choose the account that best fits your financial goals and situation.

If you’ve already read our complete guide on IRAs, you know the basics of how these accounts work. Now let’s zoom in and compare these two popular versions side by side.

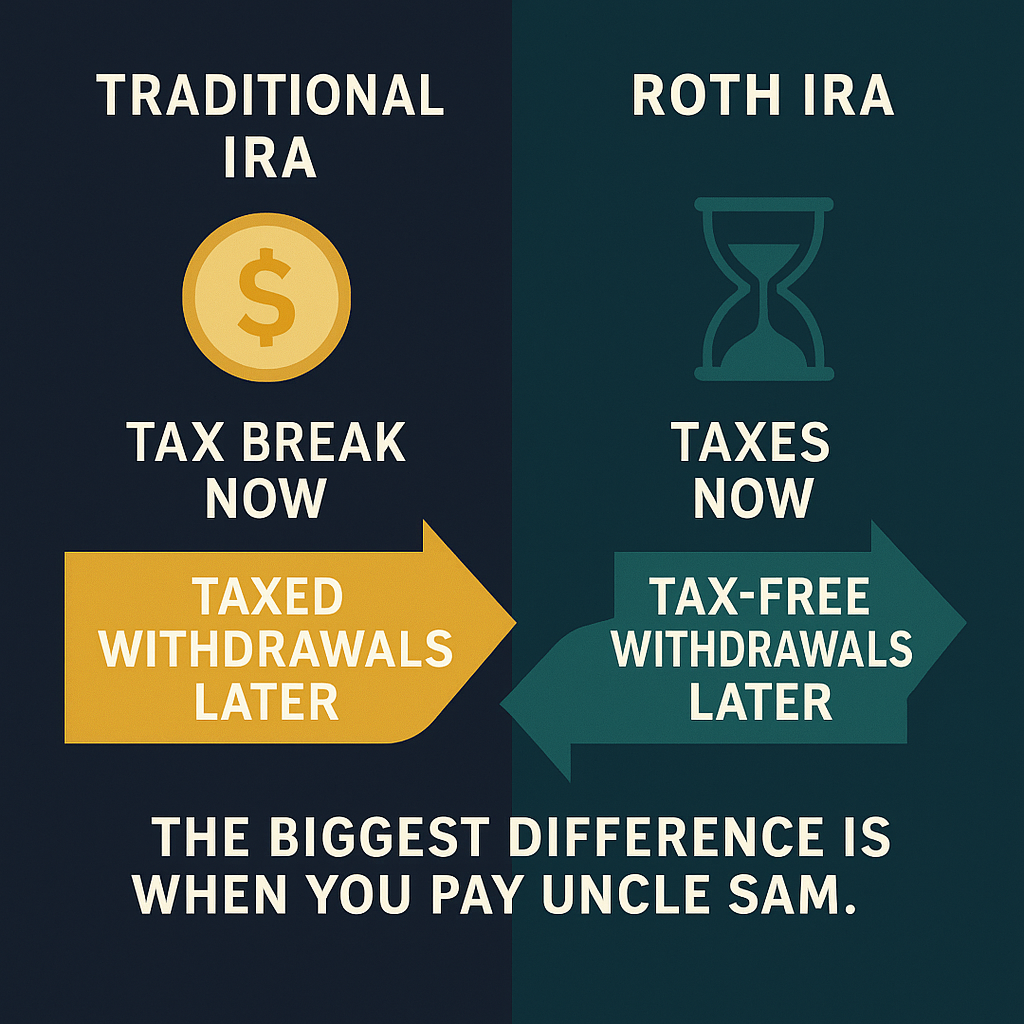

The Core Difference: When You Pay Taxes

The single biggest difference between a Traditional IRA and a Roth IRA comes down to when you pay taxes.

- Traditional IRA: You may be able to deduct your contributions from your taxable income today, lowering your current-year tax bill. The money grows tax-deferred, and when you take withdrawals in retirement, you pay taxes at your ordinary income rate.

- Roth IRA: Contributions are made with after-tax dollars (no deduction now). The money grows tax-free, and qualified withdrawals in retirement — including all investment gains — are completely tax-free.

Think of it this way:

- Traditional IRA = tax break today, taxes later.

- Roth IRA = taxes today, tax break later.

Contribution Rules

Both Traditional and Roth IRAs share the same annual contribution limits set by the IRS. For 2025, you can contribute up to $7,000 per year (or $8,000 if you’re 50 or older). But the rules on who can contribute differ.

- Traditional IRA: Anyone with earned income can contribute, but the ability to deduct those contributions on your taxes may be limited if you or your spouse has a retirement plan at work and your income is above certain thresholds.

- Roth IRA: Not everyone can contribute directly. Your eligibility depends on your income. If you earn above the IRS income limits, you may be phased out from contributing directly to a Roth IRA, though some investors use a “backdoor Roth” strategy to get around this.

Withdrawals in Retirement

Withdrawals are another area where Traditional and Roth IRAs differ significantly.

- Traditional IRA: Withdrawals are taxed as ordinary income. And starting at age 73, you must begin taking Required Minimum Distributions (RMDs), whether you need the money or not.

- Roth IRA: Qualified withdrawals are tax-free. Even better, Roth IRAs do not require RMDs during the owner’s lifetime. This gives Roth IRAs an edge in estate planning since you can let the account grow untouched and even pass it on to heirs tax-free.

Early Withdrawal Rules

IRAs are designed for retirement, so the government discourages early withdrawals. But the penalty rules are slightly different between the two accounts.

- Traditional IRA: If you withdraw before age 59½, you’ll generally owe both taxes and a 10% penalty. There are exceptions (for example, up to $10,000 for a first-time home purchase or certain education and medical expenses).

- Roth IRA: Contributions (the money you put in) can be withdrawn at any time, tax- and penalty-free. Earnings, however, are subject to the same 59½ rule and five-year rule. Withdraw too early, and you could face taxes and penalties on the earnings portion.

Who Benefits Most from Each?

The right choice depends on your current and expected future tax situation:

- Traditional IRA may be better if:

- You want to reduce your taxable income today.

- You expect to be in the same or a lower tax bracket when you retire.

- You don’t qualify for a Roth due to income limits.

- Roth IRA may be better if:

- You expect to be in a higher tax bracket later in life.

- You value tax-free income in retirement.

- You want flexibility to withdraw contributions without penalty.

- You like the idea of leaving tax-free assets to heirs.

A Quick Side-by-Side Comparison

| Feature | Traditional IRA | Roth IRA |

| Contributions | May be tax-deductible | Made with after-tax dollars |

| Annual Limit (2025) | $7,000 ($8,000 if 50+) | $7,000 ($8,000 if 50+) |

| Income Restrictions | None for contributions; limits apply to deduction eligibility | Income limits apply to contributions |

| Tax on Withdrawals | Taxed as ordinary income | Tax-free if qualified |

| Early Withdrawals | Taxes + 10% penalty (with exceptions) | Contributions always penalty-free; earnings subject to rules |

| RMDs | Required starting at age 73 | None during owner’s lifetime |

Making the Choice

For many savers, the decision between a Traditional IRA and a Roth IRA isn’t an all-or-nothing choice. You can have both, and in some cases, that balance makes sense. Having money in both types of accounts gives you flexibility in retirement to manage your taxable income year by year.

For example:

- During years when your taxable income is high, you might draw from Roth funds tax-free.

- In years when your income is lower, you could tap into Traditional IRA funds and pay less in taxes.

This kind of tax diversification can give you more control and stability in retirement.

Final Thoughts

Both Traditional and Roth IRAs offer powerful advantages compared to a standard taxable account. The key is understanding the timing of taxes and how that fits with your financial goals. If you’re unsure, you don’t have to make the decision alone. A financial advisor or tax professional can help you evaluate your situation and decide which type — or combination — is best.

Whichever you choose, the most important thing is to get started. Consistent contributions, smart investment choices, and time in the market matter more than choosing the “perfect” IRA type from day one. By taking action now, you set yourself on the path to a more secure and flexible retirement.

{kind=link}