If you’ve read What Is Venture Capital? A Deep Dive into Startup Investing, you already know that venture capital is a powerful engine for funding startups and fueling innovation. But venture capital also comes with its own language—terms that are often tossed around in pitch meetings, term sheets, and fund documents.

For new investors (or even founders raising money), not knowing these terms can be like trying to play chess without knowing how the pieces move. To help, here’s a breakdown of 10 essential venture capital terms that every investor should know—and why they matter in real-world investing.

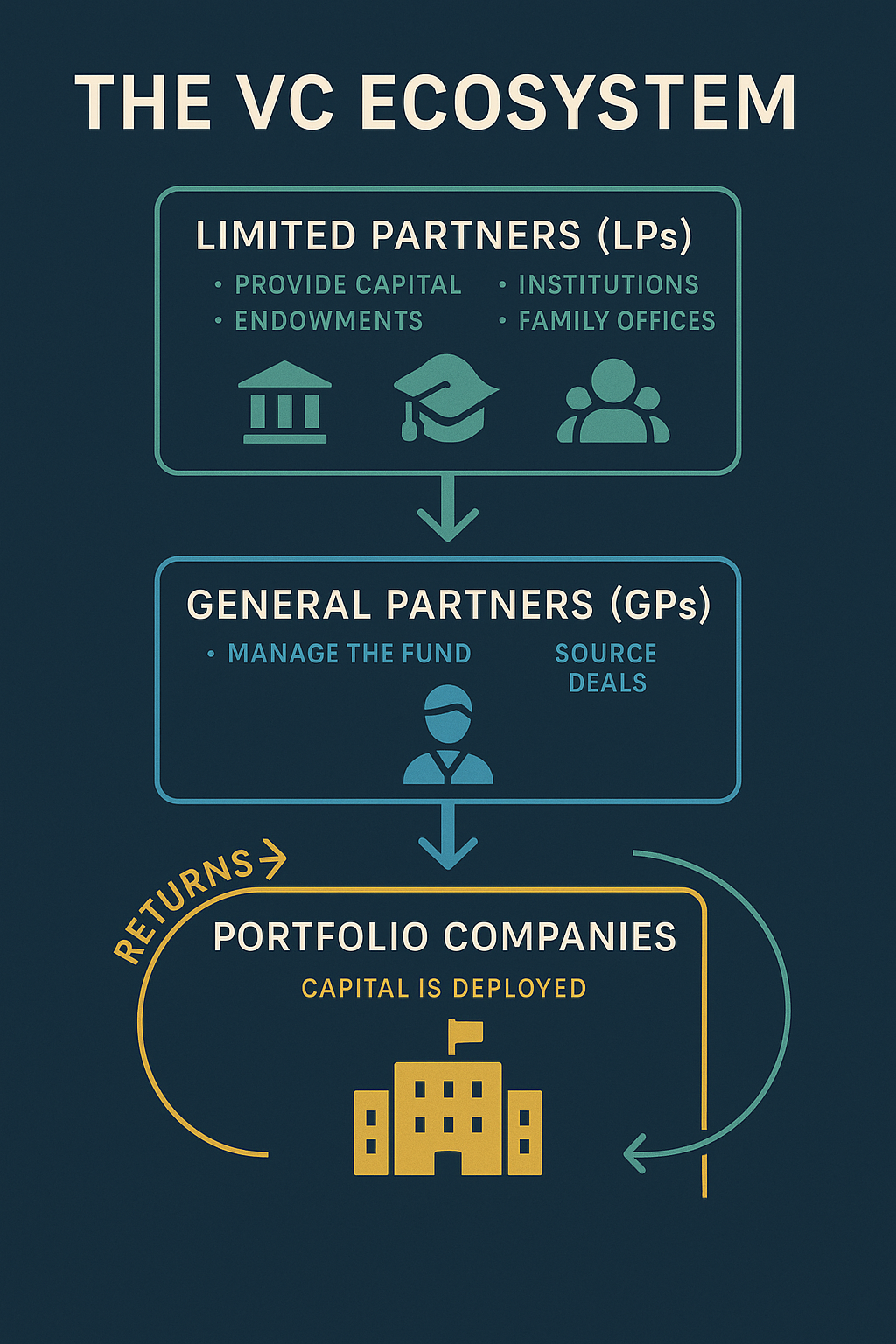

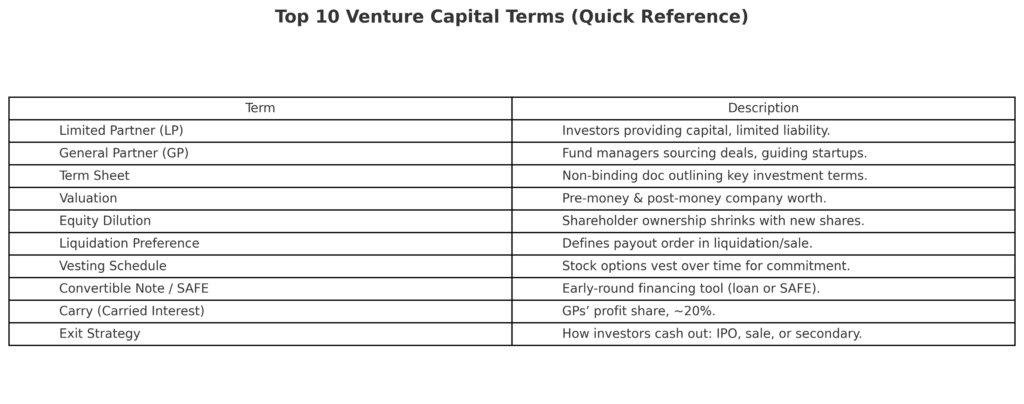

1. Limited Partner (LP)

LPs are the investors who commit capital to a VC fund. They can be pension funds, university endowments, family offices, or wealthy individuals. Their liability is limited to the amount they invest, and they rely on the fund managers to deploy capital wisely. Without LPs, VC firms wouldn’t exist, since LPs provide the majority of the funding behind deals.

2. General Partner (GP)

The GP is the manager of the venture fund. GPs source deals, conduct due diligence, negotiate term sheets, and guide portfolio companies. They also invest some of their own money in the fund to align interests with LPs. A strong GP with a history of successful exits can make or break a fund’s performance.

3. Term Sheet

This is the non-binding document that outlines the key terms of an investment. It covers valuation, ownership percentage, liquidation preferences, governance rights, and more. While most provisions are negotiable, certain clauses—like confidentiality and exclusivity—are binding. A term sheet is often compared to an engagement before marriage: it’s not the final contract, but it sets the stage for the legal agreements to come.

4. Valuation (Pre-Money & Post-Money)

Valuation defines how much a startup is worth.

- Pre-money valuation: the company’s value before new investment.

- Post-money valuation: the company’s value after new investment is added.

For example, if a startup has a pre-money valuation of $8M and raises $2M, the post-money valuation is $10M. Understanding valuation is crucial for investors, because it dictates how much ownership they get for their money.

5. Equity Dilution

When new shares are issued, existing shareholders own a smaller percentage of the company. While dilution is normal in the startup journey, investors care about how much their stake shrinks as more funding rounds occur. Smart investors look not only at current ownership but also at how dilution will affect their return if the company raises additional rounds.

6. Liquidation Preference

This determines who gets paid first if a company is sold or liquidated. For instance, a “1x liquidation preference” means investors get back at least their original investment before common shareholders (like founders or employees) receive anything. Preferences can sometimes be stacked or include multiples (like 2x), which dramatically changes payout scenarios.

7. Vesting Schedule

To encourage long-term commitment, founders and employees typically receive stock options that vest over time—often four years, with a one-year “cliff.” If they leave early, they may forfeit unvested shares. For investors, vesting ensures that the team is motivated to stick around and build the business.

8. Convertible Note / SAFE

These are financing instruments often used in early rounds:

- Convertible Note: A loan that converts into equity later, usually at a discount or with a valuation cap.

- SAFE (Simple Agreement for Future Equity): A contract that grants the right to future equity without accruing interest like debt.

Both instruments allow startups to raise money quickly without negotiating a full valuation.

9. Carry (Carried Interest)

Carry is the share of profits that GPs earn, usually around 20%. For example, if a $100M fund returns $200M, the $100M profit may be split with $20M going to the GPs as carry and the rest distributed to LPs. Carry is a big reason why successful GPs can build enormous personal wealth.

10. Exit Strategy

Exits are how investors make money. Common exits include:

- Initial Public Offering (IPO): The company lists shares on a public exchange.

- Acquisition: Another company buys the startup.

- Secondary Sale: Investors sell their shares to another investor before an IPO or acquisition.

Without an exit, paper gains don’t turn into real returns. That’s why exit opportunities are central to every VC investment decision.

Why These Terms Matter

For VCs and founders alike, these terms define the rules of the game. They determine ownership stakes, investor protections, payout order, and ultimately, how much money everyone makes if the startup succeeds.

Investors who understand this language are better equipped to evaluate opportunities, spot risks, and negotiate fair terms. Founders who master these basics are more likely to earn trust—and funding—from investors. In short, fluency in VC jargon isn’t just about sounding smart; it’s about protecting your capital and maximizing your upside.

{kind=link}