This Content Is Only For Subscribers

In private credit, returns are built one loan at a time—and so are losses. The single biggest driver of outcomes is whether a borrower pays on time and in full. That’s “default risk.” The antidote is lending to the right companies, with the right structures, at the right prices. Here’s a clear, investor-friendly playbook for judging borrower quality and the probability and severity of default.

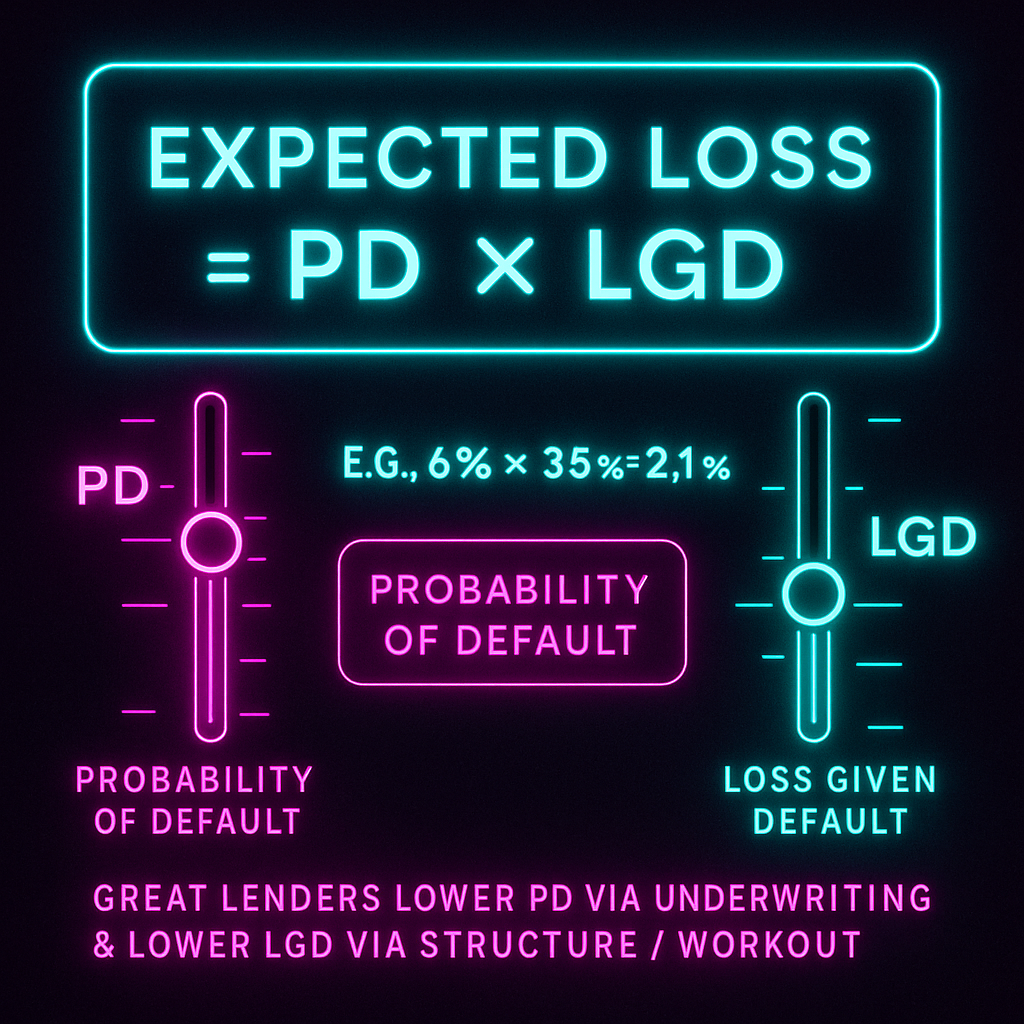

Default risk in two numbers: PD and LGD

Think of expected loss as Probability of Default (PD) × Loss Given Default (LGD).

- PD: How likely is the borrower to miss payments or breach covenants?

- LGD: If that happens, how much do you lose, after collateral and recoveries?

Great lenders work both sides: lower PD through underwriting and lower LGD through collateral, covenants, and workout plans.

The core pillars of borrower quality

1) Cash flow that persists.

Quality starts with repeatable, diversified cash flow. Look for subscription-like or contracted revenue, high customer retention, and pricing power. Ask how the business performed in past slowdowns, not just last quarter.

2) Leverage and coverage.

Debt relative to earnings (leverage) and earnings relative to interest (coverage) tell you how much shock the borrower can absorb. Strong borrowers have headroom: if base rates rise or margins compress, they can still pay.

3) Liquidity and working capital.

Healthy borrowers carry cash buffers, unused revolver capacity, and efficient working capital. Early red flags include rising DSO (customers paying slower), swelling inventory, and shrinking vendor terms.

4) Industry structure and cyclicality.

Borrowers in markets with high barriers to entry, limited substitutes, and favorable regulation handle stress better. Cyclical sectors (construction, discretionary retail, ad-supported media) need extra cushion.

5) Customer and supplier concentration.

One customer at 30% of sales? That’s risk. Quality borrowers show diversification and contingency plans if a top account churns.

6) Management, governance, and reporting.

Experienced teams, clean audits, timely reporting, and a willingness to share data matter. A high-quality borrower treats lenders as partners—no surprises.

7) Sponsor strength and alignment (in sponsor-backed deals).

A credible equity sponsor can inject capital, recruit talent, and drive cost actions. Look for meaningful equity at risk and a history of supporting portfolio companies in downturns.

Documentation can raise or lower real risk

A solid borrower can still become a problem if the loan agreement is porous. Quality shows up in:

- Maintenance covenants that bite early (leverage, interest or fixed-charge coverage, minimum liquidity).

- Negative covenants that fence off risks (limits on additional debt, liens, asset sales, dividends, affiliate deals).

- Information covenants for frequent, detailed reporting (monthly financials, KPI dashboards, borrowing-base certificates).

- Intercreditor clarity if multiple lenders are involved—who enforces, when, and how proceeds are shared.

- Cash control that springs into effect if metrics slip (blocked accounts, sweeps).

Good paper doesn’t guarantee payment, but it buys time and options when performance wobbles.

Stress testing: assume things go wrong

Underwriting should answer: “What breaks first?” Quality analysis tests scenarios such as:

- Rates up 300 bps: What happens to coverage if base rates spike?

- Revenue down 15–25%: Does cash flow still cover fixed charges after a margin squeeze?

- Working-capital shock: Can the business fund a sudden inventory build or a big customer delay?

- Refinancing wall: If credit is tight at maturity, can the company amend and extend, sell assets, or de-lever?

Managers who show downside cases with specific actions (cost cuts, capex deferrals, asset sales, sponsor equity) demonstrate control.

Warning signs you can spot early

- Accounting red flags: aggressive revenue recognition, large “one-time” add-backs that never end, or unexplained changes in capitalized costs.

- Operational slippage: missed product milestones, rising customer churn, or delayed launches.

- Covenant drift: repeated “one-off” waivers that become routine.

- Cash strain: elevated PIK interest usage where it wasn’t expected; growing reliance on vendor financing.

- Management turnover: key departures without credible replacements.

A single flag isn’t a verdict; clusters of flags deserve intervention.

How collateral interacts with borrower quality

Great borrowers with poor collateral can still create high LGD if things unravel. Conversely, average borrowers with hard, frequently tested collateral (e.g., receivables/inventory under an asset-based structure) can deliver acceptable outcomes. Ask three simple questions:

- What exactly secures the loan and how is it valued?

- How fast can it be monetized in a stress?

- What does the last cycle’s recovery data say for similar assets?

A simple scoring checklist

Use this quick rubric (1 = weak, 5 = strong):

- Revenue durability (1–5)

- Leverage & coverage headroom (1–5)

- Liquidity/working-capital discipline (1–5)

- Industry structure/cyclicality (1–5)

- Customer/supplier concentration (1–5)

- Management quality/reporting cadence (1–5)

- Sponsor alignment (if applicable) (1–5)

- Documentation strength/cash control (1–5)

- Collateral quality/speed to cash (1–5)

Scores aren’t a substitute for judgment, but they force consistency across deals.

Diligence questions to copy/paste

- How did this business perform in the last downturn? Provide monthly data if possible.

- What’s your leverage and coverage with rates +300 bps and EBITDA −20%?

- Who are the top five customers and what are their contract terms?

- What are the maintenance covenants and reporting frequency?

- If the loan can’t refinance on time, what’s the Plan B?

- What’s the sponsor’s history of writing checks in stress (amounts, timing)?

- What’s the collateral and how quickly can it be realized?

Bottom line

Borrower quality is more than a credit score—it’s the durability of cash flow, the headroom in metrics, the discipline of management and sponsors, and the teeth in your documents. If you can explain those elements in one page—and the lender can back them with data—you’ve turned default risk from a black box into a set of levers you can actually pull.

{kind=link}