This Content Is Only For Subscribers

Real estate investment trusts (REITs) look simple—own properties, collect rent, pay dividends—but behind the scenes they sit at the intersection of securities regulation (the SEC’s world) and tax regulation (the Internal Revenue Code’s REIT rules). If you’re new to REITs, here’s a clear, investor-friendly primer on how the pieces fit and what to watch.

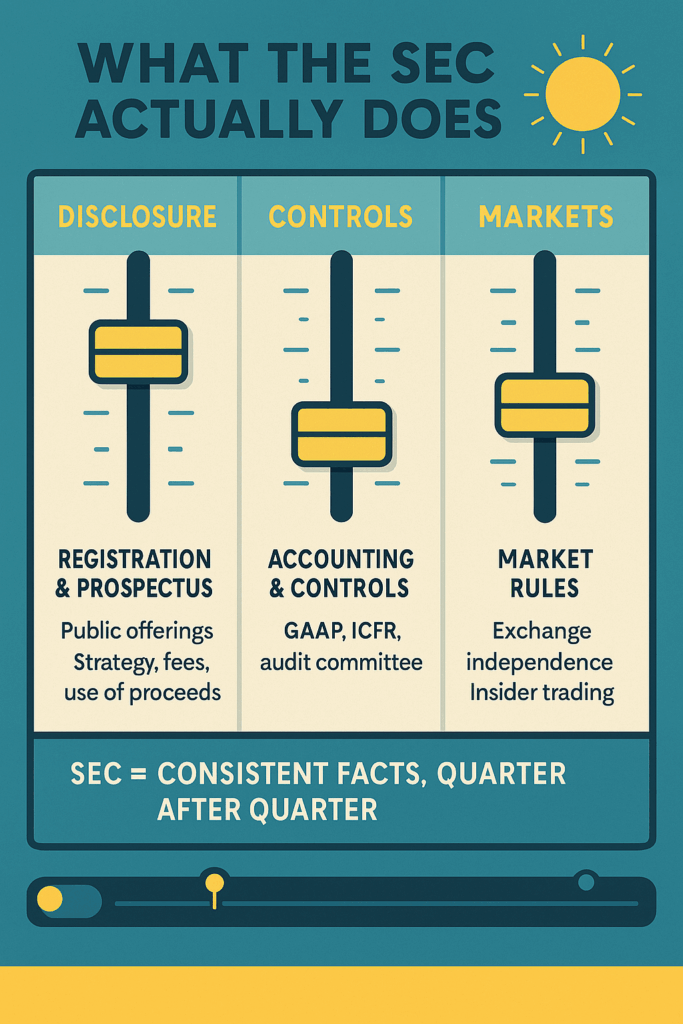

What the SEC actually does

Think of the SEC as the disclosure and market-conduct referee. It doesn’t tell a REIT what to buy, but it does require that investors get a consistent picture of what they’re buying and how it’s performing.

- Registration & prospectus. Public REITs sell shares via a registered offering with a prospectus that lays out strategy, fees, risks, conflicts, and use of proceeds.

- Ongoing reporting. After listing (or registering), a REIT files 10-Ks, 10-Qs, and 8-Ks—plus proxy statements for annual meetings and compensation votes.

- Accounting & controls. Public REITs follow GAAP, maintain internal controls over financial reporting, and have independent audit committees.

- Market rules. Listed REITs must meet exchange rules (e.g., independence standards for boards and committees) and comply with insider-trading and market-abuse prohibitions.

Investor takeaway: The SEC’s job is sunlight. When you evaluate a REIT, you should be able to find the same key facts, presented the same way, quarter after quarter.

Where tax law comes in (why REITs pay out so much)

“REIT regulation” often means tax rules that a company must satisfy to be treated as a REIT. The big ideas:

- Asset & income tests. Most assets and income must come from real estate (properties, mortgages, certain related investments).

- Distribution rule. A REIT must distribute at least 90% of its taxable income to shareholders each year.

- Shareholder & organizational rules. Broad ownership and other structural requirements apply.

Investor takeaway: The 90% rule is why REITs are known for dividends. It also means retained cash is limited, so growth often relies on external capital (debt or new equity).

Public REITs vs. non-traded and private REITs

Not all REITs live on a stock exchange.

- Exchange-listed REITs. Fully public, liquid shares, SEC reporting, exchange governance standards, and real-time pricing.

- Non-traded REITs. Registered with the SEC but not exchange-listed. They publish NAVs and periodic reports, often provide share-repurchase plans (which can be suspended), and typically carry upfront selling or ongoing distribution fees.

- Private REITs. Offered via private placements to qualified investors. They may still follow REIT tax rules but have limited public disclosure and no exchange liquidity.

Investor takeaway: The further you move from listed REITs, the more you must lean on offering documents and manager reputation. Liquidity, fees, and transparency can vary widely.

Equity REITs vs. Mortgage REITs (mREITs)

- Equity REITs own and operate properties (apartments, warehouses, data centers, healthcare facilities, etc.). Returns come from rent (cash yield) and property appreciation.

- Mortgage REITs invest in mortgages and mortgage-backed securities; returns are driven by net interest spreadand leverage. They’re more rate-sensitive and often more volatile.

Both must meet REIT tax tests, but risk drivers differ. Equity REITs hinge on occupancy, rents, cap rates, and capex. mREITs hinge on funding costs, prepayments, credit, and hedging.

External management, fees, and conflicts

Some REITs are externally managed by an affiliated advisor; others are internally managed with employees on the REIT’s payroll. External models can work, but read the fee math carefully:

- Base fees (often tied to equity or assets) and incentive fees (tied to performance).

- Related-party services (property management, development, leasing).

- Change-of-control or termination fees that can make strategy shifts costly.

Investor takeaway: The proxy and prospectus should explain every fee and who earns it. Look for independent directors, a real conflicts policy, and clear disclosure of related-party transactions.

The disclosures that matter most

When you skim a REIT’s filings, focus on:

- FFO and AFFO. Non-GAAP metrics widely used in the sector. Make sure adjustments are explained and consistent over time.

- Leverage & liquidity. Net debt to EBITDA, secured vs. unsecured mix, covenants, and laddered maturities. For mREITs, look at repo counterparties, haircuts, and hedges.

- Portfolio KPIs. Occupancy, same-store NOI growth, lease expirations, tenant concentrations, and development pipelines.

- Dividend coverage. Is the dividend supported by recurring cash flow (AFFO/earnings), or is it leaning on asset sales or leverage?

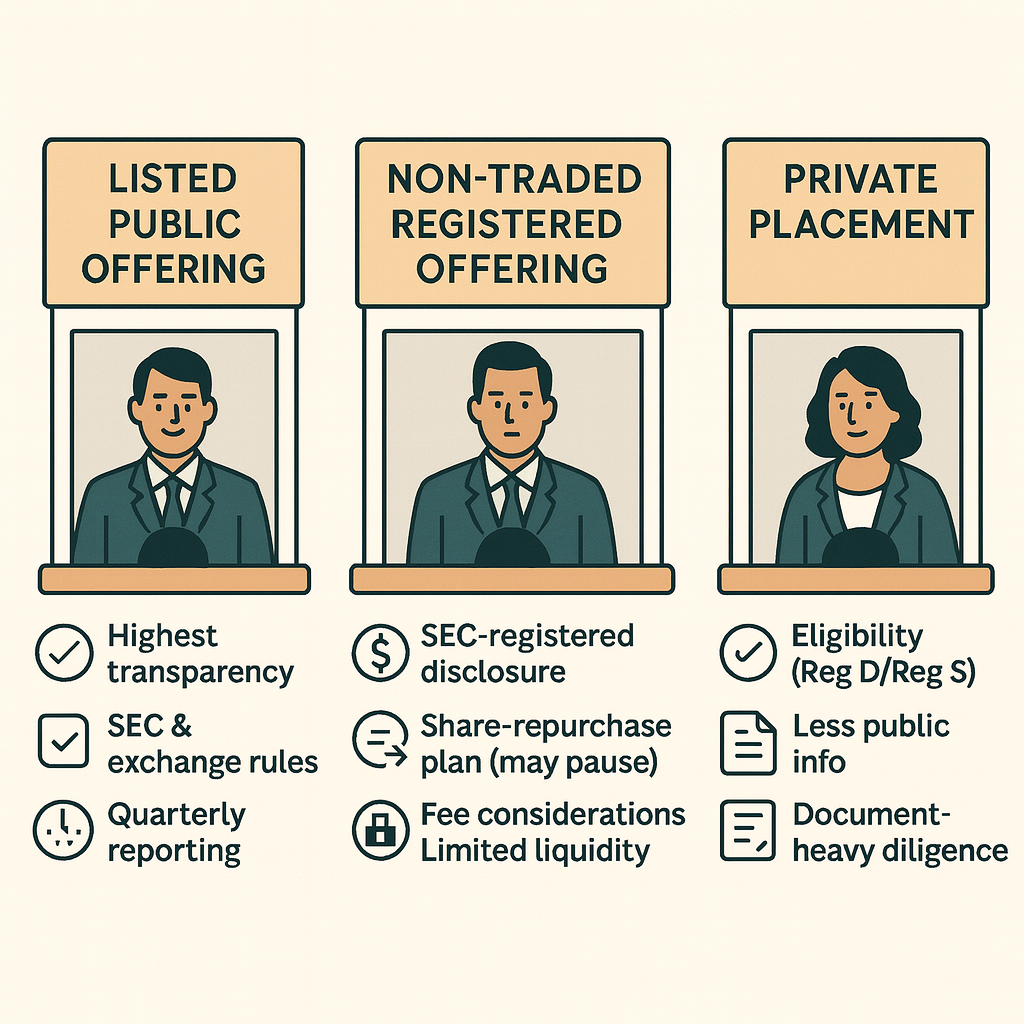

How the offering route changes your experience

- Listed public offering: Highest transparency and liquidity; live under SEC and exchange rules.

- Non-traded registered offering: SEC-registered disclosure but limited liquidity; watch fees, share-repurchase program terms, and valuation policy.

- Private placement (Reg D/Reg S): Limited eligibility and marketing; less public information; diligence is document-heavy.

Your rights, reporting cadence, and exit options flow directly from this choice.

A quick diligence checklist

- Structure: Equity REIT or mREIT? Internal or external management?

- Governance: Independent board majority? Audit and compensation committees fully independent?

- Fees & related parties: Full schedule, offsets/caps, and recent related-party transactions.

- Balance sheet: Debt metrics, covenants, maturity ladder, and hedging.

- Portfolio health: Occupancy, lease roll, tenant/borrower concentrations, and development risk.

- Dividend quality: Payout ratio vs. AFFO; history through cycles.

- Liquidity & exits: For non-traded/private, repurchase plan mechanics, gates, and historical fulfillment rates.

Bottom line

SEC regulation makes REITs disclosure-heavy; tax regulation makes them dividend-heavy. Blend those two facts and you get a clear investor playbook: read the filings for consistency, trace the fee stack and conflicts, test leverage and dividend coverage, and understand how your liquidity matches the vehicle you choose. Do that, and you’ll separate shiny marketing from durable, well-governed real estate income.

{kind=link}