This Content Is Only For Subscribers

When people say a crypto fund is “offshore,” they usually mean it’s domiciled in a cross-border fund hub such as Cayman Islands, British Virgin Islands (BVI), Bermuda, Jersey, Guernsey, or sometimes Bahamas. Offshore doesn’t mean unregulated; it typically means tax-neutral fund vehicles, specialist regulators, and a service-provider ecosystem built for institutions. Here’s a tighter, investor-friendly guide to why managers go offshore, how the pieces fit, and what to check before you wire.

Why go offshore?

Tax neutrality.

No local income/capital-gains tax at the fund level, so each investor is taxed at home—avoiding a second layer.

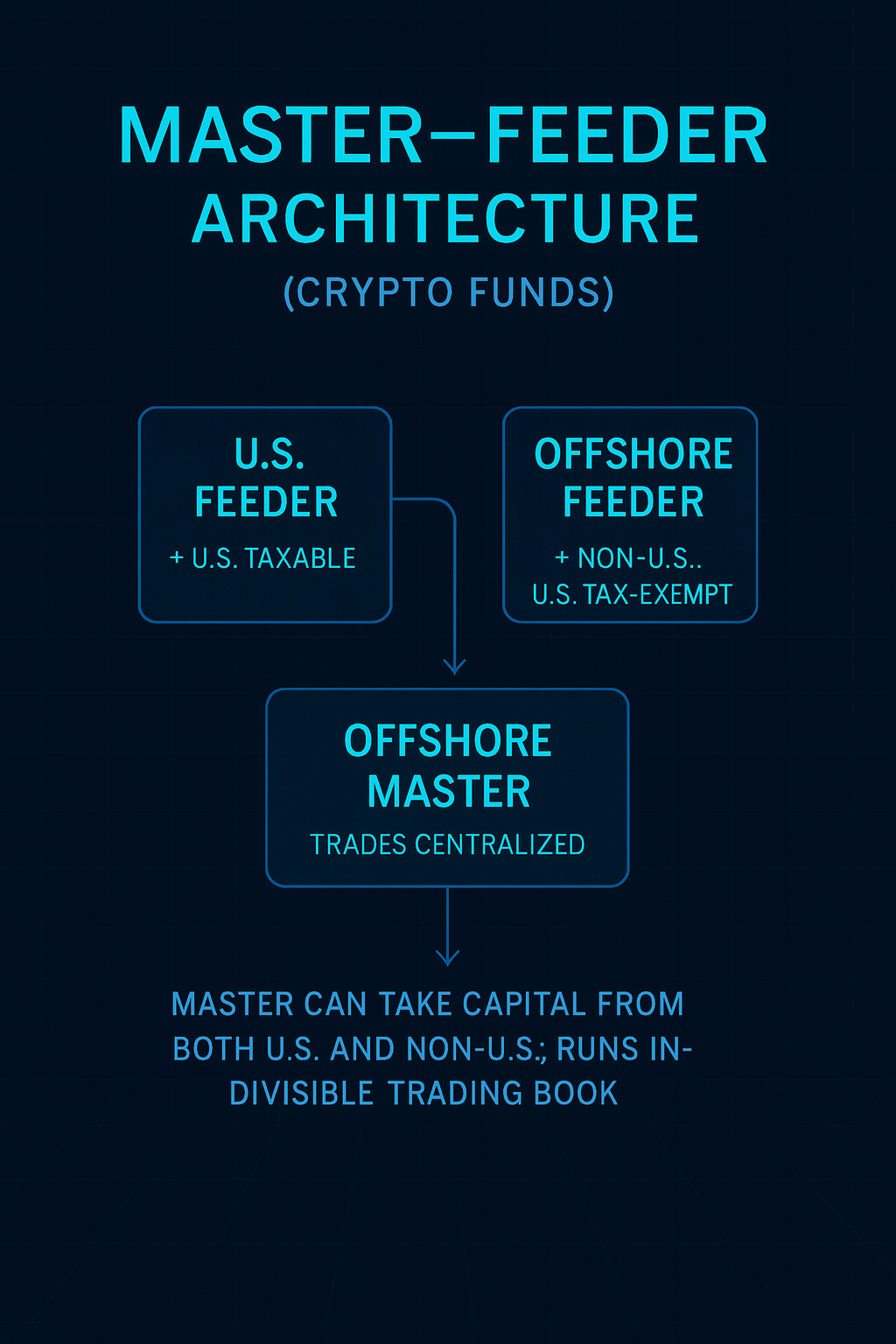

Global access.

An offshore master can take capital from a U.S. feeder (U.S. taxable) and an offshore feeder (non-U.S. and U.S. tax-exempt) while running one trading book.

Mature infrastructure.

Administrators, auditors, directors, and custodians who understand digital assets, on-chain reconciliations, and monthly NAVs.

Predictable law.

English-style company law and courts that institutions know.

Typical building blocks

Master–feeder.

U.S. and offshore feeders invest into an offshore master fund; trades and risk are centralized.

Open-ended vs. closed-ended.

Trading strategies are often open-ended with monthly/quarterly liquidity and gates. Venture/locked-token funds may be closed-ended with capital calls.

Segregated portfolios (SPCs).

Ring-fence liabilities between sleeves when running multiple strategies.

Independent governance.

Boards commonly include two independent directors who approve valuations, gates, side pockets, and key policies. Prefer directors with real digital-asset experience.

Snapshot of popular domiciles

Cayman (CIMA).

The default for many hedge/digital-asset funds. Expect AML/KYC programs, a local AML officer, and annual filings.

BVI (FSC).

Cost-efficient professional/private funds; popular for feeders and SPVs.

Bermuda (BMA).

Strong regulatory reputation; digital-asset business and custodial licenses available.

Jersey & Guernsey (JFSC/GFSC).

Governance-heavy structures and high-quality administrators; EU-adjacent without being EU.

Bahamas (SCB).

Used for specific strategies; verify current licensing and the status of service providers.

No single domicile is “best.” Choice depends on strategy, investor mix, AUM, and preferred admin/custodian stack.

Oversight—aimed at funds, not day-trading

Regulators emphasize disclosure, governance, AML/KYC, and service-provider quality:

- Offering documents spelling out strategy, fees, risks (custody, counterparties, DeFi), liquidity terms, conflicts.

- Independent administrator for NAVs, wallet/exchange reconciliations, investor registers.

- Annual audits with fair-value policies for illiquid/locked tokens and side pockets.

- AML/CTF programs with appointed officers, sanctions screening, and blockchain-analytics monitoring.

Managers who embrace these controls tend to hold up better in stress.

Taxes (fast, plain-English)

Tax-neutral ≠ tax-free.

Funds may avoid local tax, but you still owe tax at home.

Why U.S. tax-exempts use the offshore feeder.

Leverage or certain activities can generate UBTI; investing through an offshore blocker can prevent pass-through UBTI (with some corporate-level leakage).

Reporting still bites.

Expect FATCA/CRS forms (W-8/W-9) and information sharing with tax authorities. Timely, clear investor tax packs are a sign of operational quality.

Crypto-specific questions to ask

Custody clarity.

Where are assets held—qualified custodian or exchange wallets? MPC/HSM, withdrawal whitelists, multi-approvertransfers, and incident logs?

Counterparty discipline.

Approved venues? Caps on on-exchange balances? Off-exchange settlement with the custodian? Results of stress withdrawal tests?

DeFi governance.

Which protocols are approved? Code-audit standards? Position caps? How are oracle risks handled?

Valuation of illiquid/locked tokens.

Documented pricing hierarchies, liquidity discounts, and back-testing of marks vs. realized exits.

Liquidity terms that fit the assets.

For hard-to-trade holdings, you should see gates, suspension rights, and clear in-kind distribution mechanics.

Red flags vs. green lights

Red flags

- Directors with no digital-asset experience; one individual wearing too many affiliated hats.

- Manager-calculated NAVs (no independent admin).

- Custody without whitelists/multi-approvers; large venue balances.

- DeFi “yield” with no protocol list or risk limits.

- Perpetually “pending” audits.

Green lights

- Independent directors who can discuss a recent risk decision.

- Admin that can demo on-chain reconciliation and exchange break resolution.

- Named custodian(s) plus a documented transfer workflow.

- Clear securities/CPO-CTA posture for U.S./EU marketing and derivatives use.

- On-time audits; investor reports with fee math that ties to the LPA.

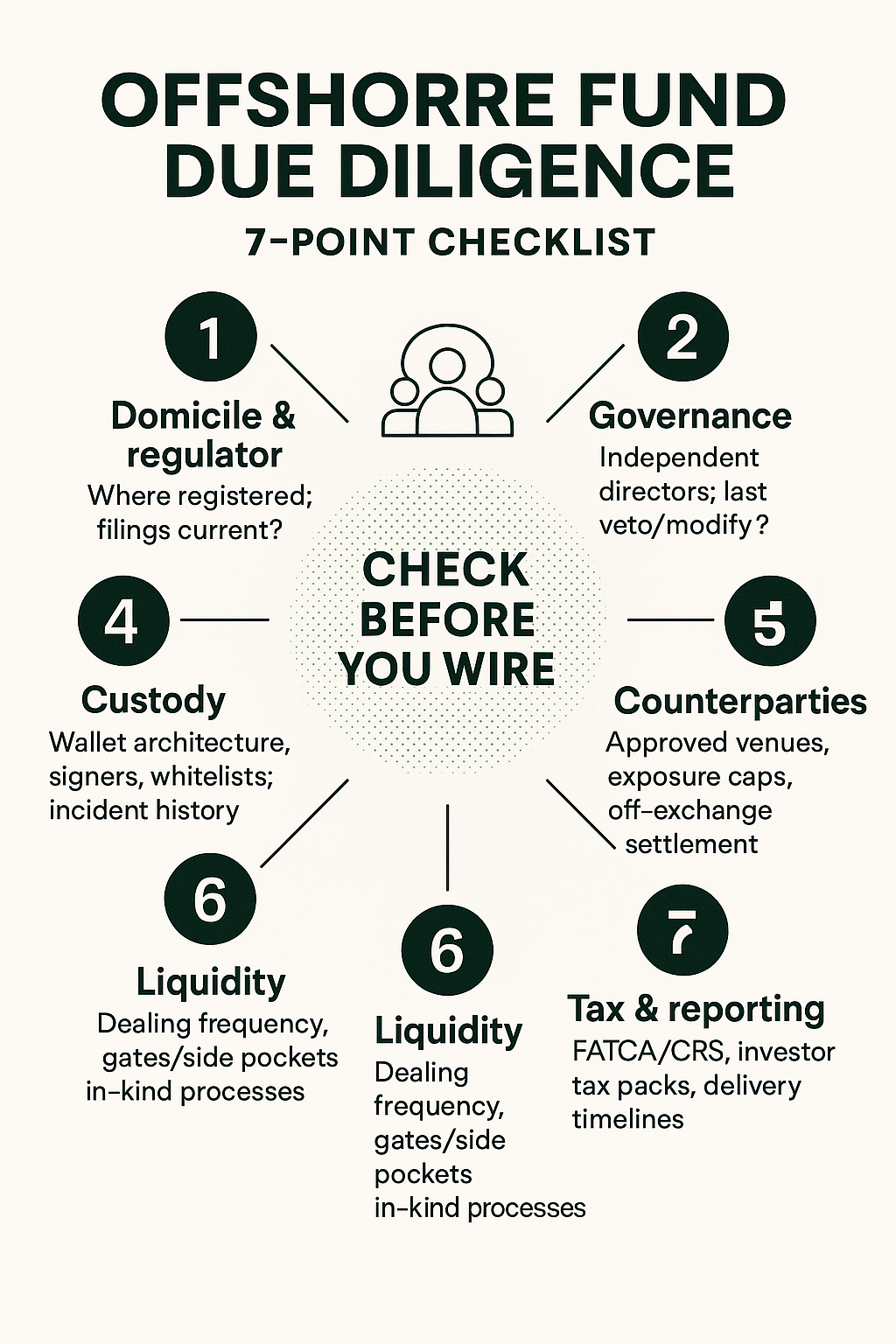

Seven-point diligence checklist

- Domicile & regulator: Where is each vehicle registered; what filings are current?

- Governance: Who are the independent directors and when did they last veto/modify a proposal?

- Admin & audit: Which firms; NAV timetable; audit timing and auditor.

- Custody: Wallet architecture, signers, whitelists, incident history.

- Counterparties: Approved venues, exposure caps, off-exchange settlement.

- Liquidity: Dealing frequency, gates/side pockets, in-kind processes.

- Tax & reporting: FATCA/CRS, investor tax packs, delivery timelines.

Bottom line

“Offshore” isn’t a loophole—it’s a tool to pool global capital under predictable law with specialist providers. Your job as an LP is to confirm that the people and processes—directors, administrator, custodian, auditor, and risk controls—are as strong as the pitch deck. When they are, the offshore structure becomes an advantage: tax-neutral, operationally mature, and built to scale safely through crypto’s cycles.

{kind=link}