This Content Is Only For Subscribers

Venture capital is global, but the rules that govern fundraising and investing are local. If you’re new to VC and thinking about cross-border deals or backing managers outside your home market, here’s a plain-English tour of how regimes differ—and what that means for access, compliance, and timelines.

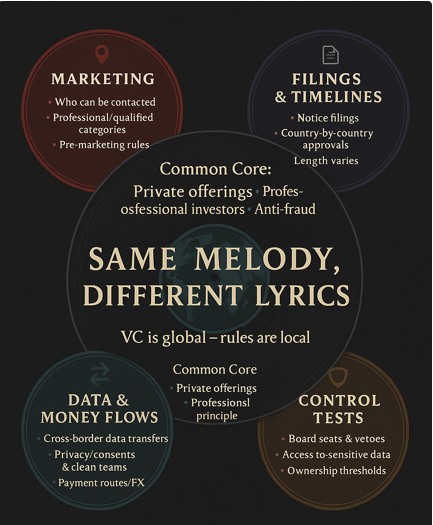

The big idea: same melody, different lyrics

Almost everywhere, venture capital relies on private offerings, professional-investor categories, and anti-fraud principles. The differences show up in who can be marketed to, what filings are needed, how data and money move, and what counts as “control.” Those details decide whether a raise is smooth and fast—or slow and expensive.

United States: adviser-centric oversight

In the U.S., regulation focuses on the investment adviser (the manager). Funds are “private” by relying on Investment Company Act exclusions; offerings typically use Regulation D. For investors, the practical checkpoints are familiar: accredited or qualified purchaser status, consistent offering documents, clear fee math, and an audit path. The U.S. also runs national security screening for foreign investments in sensitive businesses, which can affect cross-border syndicates and later exits.

Investor takeaway: Access depends on eligibility and the offering path (quiet 506(b) vs. public 506(c) with verification). Secondary sales and tender-offer rules can complicate late-stage liquidity events.

European Union: AIFMD + local FDI screening

In the EU, the Alternative Investment Fund Managers Directive (AIFMD) regulates managers of alternative funds (including VC). EU managers typically need authorization and a depositary; non-EU managers often market to professional investors via national private placement regimes (NPPR), country by country. Separately, the EU encourages foreign direct investment (FDI) screening by member states, which can catch deals in sensitive tech and infrastructure.

What changes for you? Expect a patchwork: one fund, many filings. Investor classifications are stricter, disclosures are denser, and timelines can be longer. Privacy rules (think cross-border data transfers) influence how diligence is run and what goes in a data room.

United Kingdom: familiar, but separate

Post-Brexit, the UK runs a regime similar in spirit to the EU’s but on its own legal rails. Managers lean on UK NPPRto approach professional clients; classification and conduct rules echo European concepts, though details differ. The UK also has an active national security and investment screening regime that can reach minority deals in sensitive sectors.

Investor takeaway: Comparable to the EU in feel—professional-only marketing, local filings, and careful documentation—yet approvals and thresholds are not identical.

Singapore and Hong Kong: regional hubs with modern fund wrappers

Singapore and Hong Kong compete as Asia VC hubs. Both restrict marketing to professional or institutional investors and offer manager registrations tailored to alternatives. Each has introduced modern fund vehicles—Singapore’s VCCand Hong Kong’s LPF—to make domiciling funds locally more attractive. Cross-border data rules, sanctions risk, and export-control diligence still apply when portfolio companies touch sensitive tech or markets.

Investor takeaway: Execution tends to be efficient. Make sure your manager’s license, offering notices, and investor classification all line up—and clarify how portfolio companies will handle regional data/privacy obligations.

India: sectoral caps and approvals

India blends securities regulation with sector-specific foreign investment caps and approval routes. Deals may need competition and FDI review, and certain structures (e.g., downstream investments or convertible instruments) bring extra process. For fund LPs, access typically runs through professional-investor channels with local disclosure and KYC requirements.

Investor takeaway: Plan more time for approvals and confirm how currency controls, tax treaties, and withholding will affect distributions.

China: antitrust, national security, and data

Inbound and outbound investments can trigger competition and national security reviews, while data and cybersecurity rules have grown more prescriptive. For venture, that shows up in diligence (which customer and data sets are “sensitive”), governance (board rights and information access), and exit options.

Investor takeaway: Minority positions can still be “high-process.” Work with managers who have a concrete plan for information flows, compliance, and potential on-shore vs. off-shore listing routes.

Australia, Japan, and Korea: sophisticated but specific

All three run mature competition regimes and professional-investor marketing rules. Australia’s FIRB process examines certain foreign investments; Japan and Korea have sectoral screens and disclosure expectations. Documentation is local—U.S. purchase agreements aren’t copy-paste, and employee-equity rules diverge.

Investor takeaway: Deals are doable; timelines depend on sector sensitivity and filing thresholds. Ask for a filing matrix early.

Canada and the Middle East: dual tracks and fast lanes

Canada mixes Competition Act merger control with national-interest review in sensitive areas. Fundraising follows provincial/federal private-offering rules; investor categories mirror U.S. concepts.

In the Middle East, ADGM (Abu Dhabi) and DIFC (Dubai) have grown as fund hubs with English-language common-law frameworks. Marketing focuses on professional investors; licensing is streamlined but documentation standards are high.

Investor takeaway: Solid infrastructure and growing ecosystems. Confirm distribution permissions and any local-custody quirks before wiring.

Latin America and Africa: evolving but investable

Brazil and Mexico have active venture scenes with improving private-offering pathways and local competition review. In South Africa and other African markets, professional-investor regimes and exchange-control rules can shape fund flows and exit options. In many cases, funds domicile in a hub (e.g., Mauritius, Luxembourg, Delaware) and invest locally through subsidiaries.

Investor takeaway: Look closely at currency, tax leakage, and repatriation mechanics; ensure your manager’s on-the-ground counsel is strong.

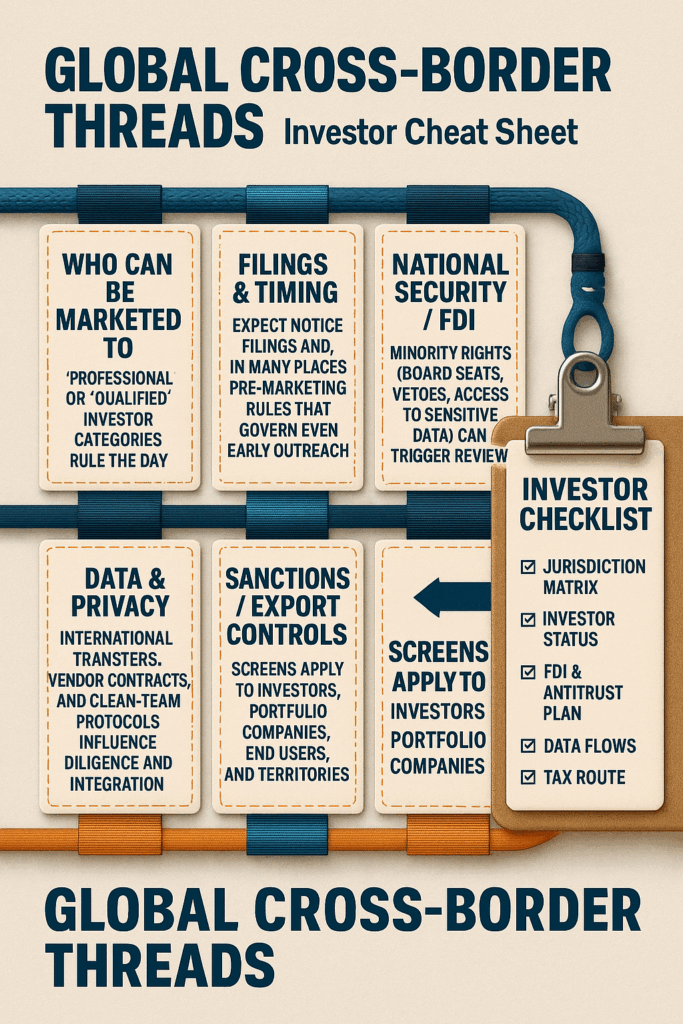

Cross-border themes that matter everywhere

- Who can be marketed to: “Professional” or “qualified” investor categories rule the day.

- Filings and timing: Expect notice filings and, in many places, pre-marketing rules that govern even early outreach.

- National security/FDI: Minority rights (board seats, vetoes, access to sensitive data) can trigger review.

- Data and privacy: International transfers, vendor contracts, and clean-team protocols influence diligence and integration.

- Sanctions/export controls: Screens apply to investors, portfolio companies, end users, and territories.

- Tax and cashflows: Withholding rates, treaty access, and blocker structures can change your net return more than a few basis points of fees.

A quick investor checklist

- Jurisdiction matrix: Where can the manager legally market? What filings are done?

- Investor status: Which category do you fall into locally (professional, sophisticated, institutional)?

- FDI & antitrust plan: Any likely filings for the target sectors and countries?

- Data flows: How will diligence and post-close operations handle sensitive data?

- Tax route: Holding company, treaty benefits, expected withholding, and exit path.

- Local docs: Who is local counsel; how do the SPA/term sheets change by country?

- Timetable realism: Longest-lead approval sets the schedule—has the team planned for it?

Bottom line

Global venture isn’t one market—it’s a network of local rulebooks. The best managers treat regulation as part of execution: they map investor categories, file where needed, design clean data flows, and build realistic calendars. As an LP or co-investor, you don’t need to memorize every statute. You just need to recognize the patterns, ask for the jurisdiction matrix, and back teams that run process as carefully as they pick founders. That’s how you keep the “venture” in cross-border venture—without turning your closing timetable into the adventure.

{kind=link}