This Content Is Only For Subscribers

When you hear about a startup raising money at a $1 billion valuation, it can sound magical—like the number was pulled from thin air. And in some ways, it is. Unlike public companies, startups don’t have years of audited financials, steady profits, or predictable cash flows. So how do venture capitalists (VCs) decide what a startup is worth?

The truth is that valuing startups is more art than science. It blends financial analysis, market potential, negotiation, and psychology. Understanding how VCs value startups reveals not just how deals are made, but why some companies skyrocket while others struggle to raise funds.

The Challenge of Valuation

Valuing a public company is relatively straightforward. You can look at:

- Earnings per share

- Price-to-earnings ratios

- Cash flows and dividends

Startups don’t have most of these. A seed-stage company may not even have revenue, let alone profits. That forces VCs to rely on proxies, estimates, and judgment calls.

As one VC quipped: “Startup valuation is like astrology—people pretend it’s science, but it’s really belief mixed with math.”

Key Factors VCs Consider

1. Market Size and Potential

A startup’s value often comes from the total addressable market (TAM). If the potential market is huge, the startup has room to grow into a large company—even if today it’s tiny. That’s why VCs love markets like AI, fintech, or healthcare.

2. Traction and Growth

Early signs of customer adoption matter more than profits. VCs look at:

- Monthly active users

- Revenue growth rates

- Customer retention

Even modest revenue can justify high valuations if growth is fast and accelerating.

3. Team Quality

VCs say they “invest in people, not ideas.” A strong founding team with relevant experience and grit can justify a higher valuation.

4. Competitive Landscape

If competitors are weak—or if incumbents are slow to adapt—the startup is worth more.

5. Comparable Deals

VCs look at recent valuations of similar startups. If a peer just raised at a $500M valuation, they may benchmark against that.

The Valuation Methods

Despite the uncertainty, there are frameworks VCs use.

Venture Capital Method

This back-of-the-envelope calculation estimates:

- The startup’s potential exit value (IPO or acquisition).

- The VC’s target return multiple (often 10x).

- The required ownership percentage to reach that return.

Example: If a VC thinks a company could exit at $1B in 7 years, and they want 10x on a $20M investment, they’ll target 20% ownership. That implies today’s valuation should be around $100M.

Scorecard Method (often used in seed rounds)

Investors compare the startup against an “average” funded company on criteria like team, market, and product. They then adjust the valuation up or down.

Discounted Cash Flow (DCF)

Rarely used for early-stage startups, since cash flows are speculative. More common in later-stage deals with actual revenues.

Comparables (“Comps”)

Valuing based on similar companies—public or private. For instance, if other SaaS startups are valued at 10x revenue, a $10M-revenue SaaS company might be valued at $100M.

The Role of Negotiation

Valuation isn’t just math—it’s also negotiation. Founders want the highest price; VCs want to pay less while still winning the deal. The “right” valuation is often whatever the two sides agree upon.

Hot markets (like AI in 2023–24) push valuations higher because multiple VCs compete for the same startups. In downturns (like 2022), valuations fall as capital tightens.

Dilution and Rounds

Valuations also determine how much of the company founders give up.

- Seed round: $5M valuation, $1M raised → investors own 20%.

- Series A: $20M valuation, $5M raised → new investors get 25%.

- Series B: $100M valuation, $20M raised → 20% sold.

Over multiple rounds, founders can be diluted significantly. That’s why “getting the valuation right” early matters—it affects ownership years down the line.

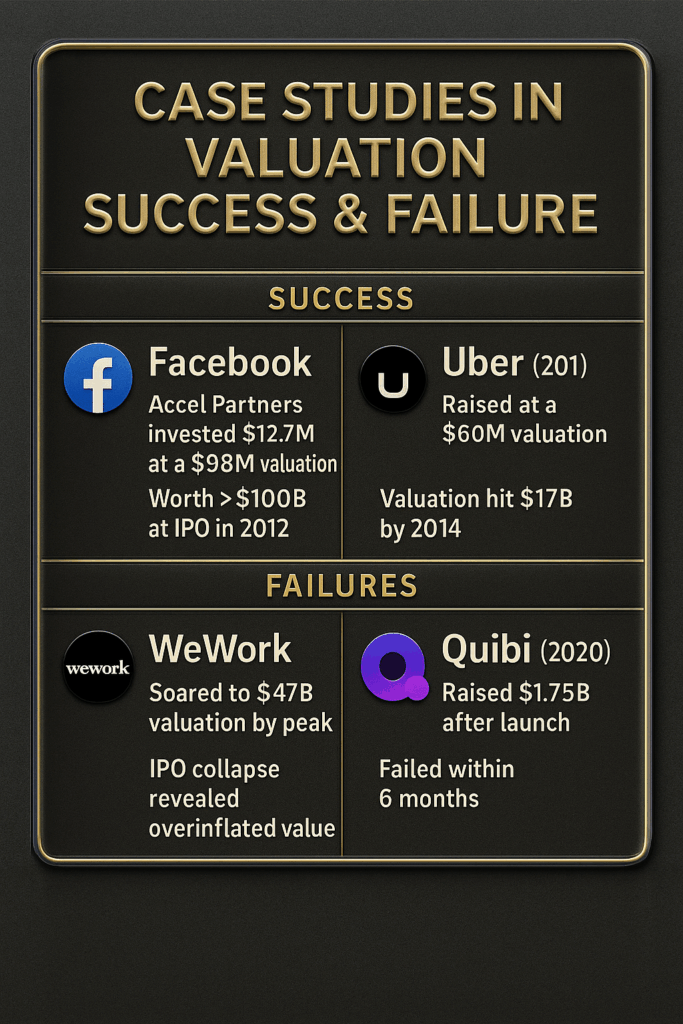

Case Studies in Valuation

Facebook (2005)

Accel invested $12.7M at a $98M valuation. At IPO in 2012, Facebook was worth over $100B. That early valuation, high at the time, proved a bargain.

Uber (2011)

Raised at a $60M valuation; by 2014, it was worth $17B on paper. Each round reset expectations upward, showing how momentum drives valuation.

WeWork (2019)

At its peak, WeWork was valued at $47B. When its IPO collapsed, it showed how overinflated valuations can unravel quickly.

Why Valuation Isn’t Everything

For founders, a higher valuation isn’t always better. A sky-high valuation can create problems:

- Pressure: The company must grow into it quickly.

- Down rounds: If growth slows, future investors may demand a lower valuation, hurting morale.

- Exit mismatch: If the valuation is too high, acquirers may balk.

Sometimes, raising at a realistic valuation sets a healthier trajectory.

Lessons for Novice Investors

Even if you never invest in startups, the way VCs value companies offers lessons:

- Value is about potential, not just the present. Growth and market size matter as much as current revenue.

- Comparables shape expectations. Whether it’s stocks or startups, markets look to peers for benchmarks.

- Negotiation drives price. The “right” valuation is often what someone will pay.

- Don’t overpay for hype. WeWork is a reminder that sky-high valuations can collapse.

- Ownership matters. Dilution happens in startups; in personal investing, it’s a reminder to track how your share of an investment changes over time.

Final Thoughts

Startup valuations are both science and art. They mix financial models, market analysis, negotiation, and sometimes sheer optimism. For VCs, getting it right is critical—overpaying makes returns harder, while underestimating can mean missing the next big winner.

For novice investors, the deeper lesson is this: valuation is about balancing risk with potential. Whether you’re buying shares of a public company or negotiating the price of a house, the same principle applies. Price is what you pay, but value is what you get.

{kind=link}