This Content Is Only For Subscribers

Private credit has exploded from a niche corner of finance into a mainstream asset class. Pensions, endowments, family offices, and even high-net-worth individuals now allocate to funds that lend directly to companies, real estate projects, or asset pools—outside of the traditional banking system and away from public bond markets. The appeal is easy to grasp: higher yields, more control, and less day-to-day price volatility than public fixed income. The trade-offs are just as real: illiquidity, underwriting risk, and the need for hands-on management when something goes wrong.

If you’re new to private credit, this guide is a plain-English tour of how returns are made, where risks hide, and how to evaluate managers before you wire a dollar.

What is private credit?

At its core, private credit is lending that happens privately—bilateral or club deals negotiated between lenders and borrowers—rather than through broadly distributed bonds or bank loans. A private credit fund raises capital from investors and uses that capital (often with a modest credit facility on top) to originate and hold loans. These loans may finance acquisitions, growth initiatives, working capital, equipment, real estate, or specialty assets like consumer receivables.

Common strategies include:

- Senior secured/direct lending: First-lien loans to middle-market businesses, often sponsor-backed.

- Unitranche: A single blended loan that combines senior and junior risk into one instrument with one set of documents.

- Second-lien and mezzanine: Subordinated loans with higher coupons and sometimes warrants or equity kickers.

- Asset-based lending (ABL): Loans secured by liquid collateral such as receivables, inventory, or equipment with tight borrowing-base formulas.

- Real estate credit: Bridge loans, construction loans, or mezzanine financing on commercial or residential assets.

- Specialty finance/securitized credit: Financing against pools of assets (e.g., auto loans, solar leases, small-business receivables).

- Opportunistic/distressed: Lending into complex or stressed situations, often with stronger downside protections but higher work-out intensity.

Each strategy sits at a different point on the risk–return spectrum. Understanding where a fund plays—and how it controls risk at that point—is step one.

How returns are generated

Private credit returns have several building blocks:

- Base rate + spread. Most loans float off a short-term reference rate. The spread compensates for borrower risk. In floating-rate markets, coupons can rise quickly when rates rise—one reason private credit yields have looked attractive in recent years.

- Fees. Investors benefit indirectly from origination fees paid upfront by borrowers, prepayment fees if loans are taken out early, and sometimes exit fees. These fees boost the yield but are only realized if the loan closes and performs as expected.

- OID (original issue discount). Lending at a discount raises the effective yield.

- Equity kickers. Subordinated or opportunistic strategies may receive warrants or co-investment rights. If the borrower thrives, these can be a meaningful part of total return.

- Active management. Private lenders can amend and extend, add covenants, or adjust pricing as conditions change. Skilled managers earn a premium by staying in front of problems and getting paid for accommodations.

Returns are quoted as yield (current cash coupon), net IRR (after fees and expenses), and MOIC (multiple on invested capital). For income-oriented strategies, look closely at the cash pay portion vs. PIK (pay-in-kind) interest, which accrues but doesn’t bring in cash today.

The core risks you’re taking

Private credit is not “stock-like returns with bond-like risk.” It is credit—and the biggest risks relate to getting your money back and getting it back on time.

1) Credit risk and default

Borrowers can miss payments or violate covenants. The probability of default (PD) and loss given default (LGD)together determine expected losses. Senior secured loans to stable, cash-flowing businesses typically have lower LGD because collateral can be liquidated; subordinated loans or high-capex businesses may have higher LGD.

2) Documentation and covenant risk

The loan agreement is your playbook in good times and your only leverage in bad times. Covenant-lite documents, excessive carve-outs, or weak collateral descriptions reduce control when performance slips. Conversely, tight financial covenants (e.g., leverage, interest coverage), reporting requirements, and negative covenants (limits on asset sales, dividends, or additional debt) are practical tools for early intervention.

3) Liquidity and funding risk

Private credit funds are illiquid. You can’t click “sell.” Your capital may be locked for years, with distributions driven by interest receipts and principal repayments. Many funds use a credit facility to smooth cash flows; that facility introduces lender covenants and margin call risk if portfolio performance drops.

4) Interest-rate and refinancing risk

Floating-rate structures pass rate changes to borrowers. That’s great when spreads are wide and borrowers are healthy, but rising base rates raise their interest burden, potentially squeezing coverage ratios and increasing default risk. On the flip side, when rates fall, income may decline unless spreads widen.

5) Concentration and sector risk

A portfolio of 20 loans where the top five are 50% of NAV behaves differently than one with 100 loans and tighter position limits. Concentrations in cyclical sectors (construction, discretionary retail, ad-supported media) amplify drawdowns in downturns.

6) Vintage and macro risk

Deals originated at peak valuations or peak optimism often feature more aggressive underwriting. Assess the vintage mix in a fund: loans underwritten across several cycles are less exposed to one set of assumptions.

Collateral, seniority, and the capital structure

When you lend, you’re placing a claim in a borrower’s capital stack. Key ideas:

- Seniority. First-lien lenders get paid before second-lien and mezzanine lenders. Seniority usually means lower yield but higher recovery in stress.

- Collateral. The security package describes what you can take if things go wrong: all-asset liens, specific assets (equipment, IP), stock pledges, or property mortgages. In ABL, the borrowing base sets advance rates for receivables or inventory and is tested frequently.

- Intercreditor agreements. When multiple lenders coexist, these documents decide who can enforce remedies and in what order. They matter more than the pitch deck.

A good manager can explain exactly what the collateral is, how it’s monitored, and what the realistic path to recovery looks like under stress.

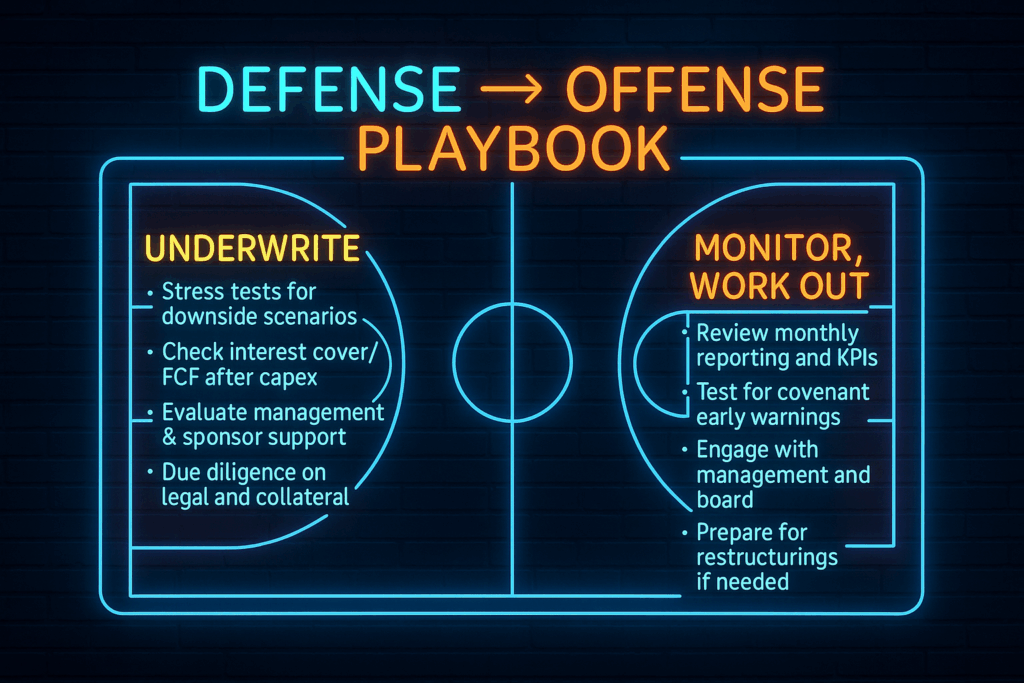

How managers control risk: underwriting and monitoring

Underwriting starts with cash flow. Solid lenders build models that survive ugly scenarios: sales down 20%, margins compress, capex rises, customers delay payments. They check interest coverage, free cash flow after capex, and liquidity runway. They also test for refinancing walls—what happens if a loan matures in a tight credit market?

Beyond numbers, underwriters scrutinize:

- Sponsor support. Private equity sponsors can add capital, talent, and discipline. Non-sponsored deals rely more heavily on collateral and management quality.

- Management and governance. Depth of the team, reporting cadence, and alignment (equity at risk).

- Industry dynamics. Barriers to entry, customer concentration, pricing power, regulation, and cyclicality.

- Legal diligence. Lien perfection, intellectual-property assignments, leases, permits, and litigation checks.

Monitoring is where average managers become great ones. Expect:

- Monthly reporting with borrowing-base certificates (for ABL), aging schedules, and KPI dashboards.

- Covenant testing and early-warning indicators (e.g., rising days sales outstanding, inventory builds, churn).

- Active engagement—site visits, customer calls, board observers, and third-party field exams.

When a loan drifts, good managers act early: tighten covenants, take fees for amendments, obtain additional collateral, or bring in operational help. If deterioration continues, they prepare for workout: appoint advisors, negotiate standstills, run sale processes, or take control via a restructuring.

Portfolio construction: not all diversification is equal

A well-built private credit portfolio spreads risk thoughtfully:

- Position sizing. Caps by borrower (e.g., 2–4% of NAV) and by sector.

- Seniority mix. A core of senior secured loans complemented by higher-yielding junior risk where the manager has edge.

- Collateral diversity. Mix of cash-flow-based and asset-based loans; avoid overreliance on one asset type (e.g., all software ARR or all construction inventory).

- Maturity ladder. Staggered maturities to avoid concentrated repayment risk in any year.

- Leverage discipline. Reasonable use of fund-level credit lines with ample covenant headroom and multiple bank relationships.

Look for non-accrual rates, realized loss history, and dispersion of outcomes across deals. A manager who can show small, frequent gains and small, infrequent losses is often more reliable than one boasting a few home runs and thin data on everything else.

Fees, liquidity, and alignment

Private credit funds typically charge a management fee on committed or invested capital and a performance fee(carry) above a hurdle. Useful questions:

- Is the fee charged on net invested capital or commitments (and for how long)?

- Is carry paid only on realized gains, or can it be accrued against unrealized marks?

- Are there clawback or escrow provisions if later losses materialize?

- How does the manager participate—do they have a meaningful GP commit?

Liquidity varies:

- Closed-end funds call capital over an investment period and return proceeds as loans pay off.

- Evergreen/interval funds or BDCs may target periodic liquidity but can gate redemptions.

- Co-investments can concentrate exposure; understand the rights and timing for exits.

Alignment improves when managers eat their own cooking, have carry truly at risk, and are transparent about how credit facilities are used.

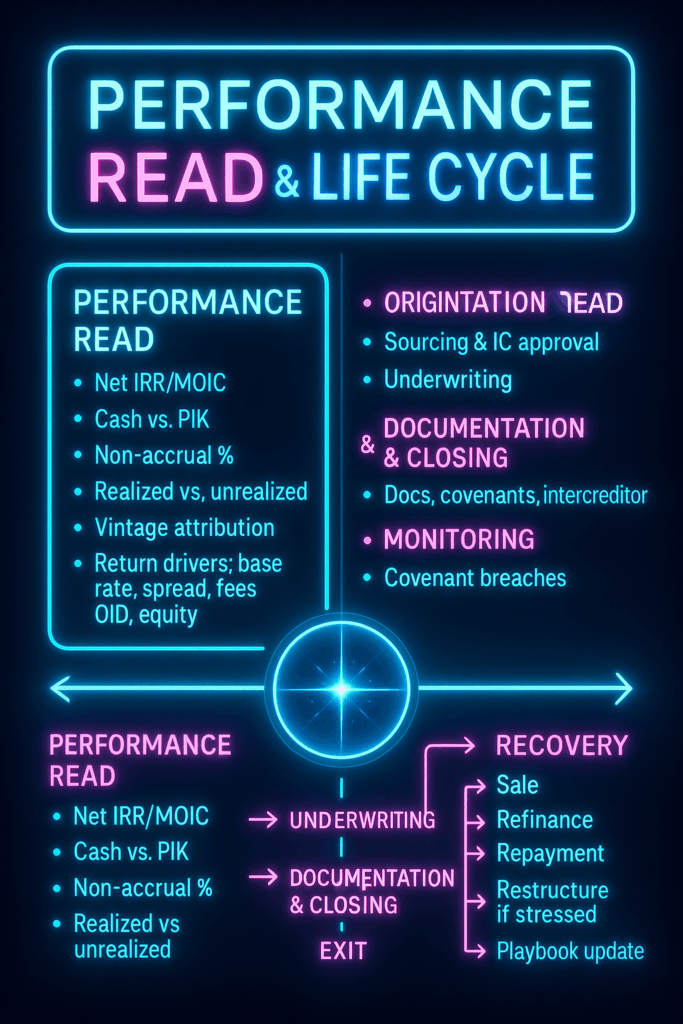

How to read performance

Performance in private credit should be evaluated beyond headline yield.

- Gross vs. net. Focus on net IRR/MOIC after all fees and expenses.

- Cash vs. PIK. High PIK percentages can mask stress.

- Non-accrual rate. What percentage of the portfolio isn’t currently paying cash interest?

- Realized vs. unrealized. Realized loss history is harder to game than interim marks.

- Vintage analysis. How did loans underwritten in different years perform relative to macro conditions?

- Attribution. How much return came from base rate, spread, fees, OID, and equity kickers?

Managers who can disaggregate returns—deal by deal, driver by driver—tend to be more in control.

The loan lifecycle: from term sheet to takeout

- Origination & underwriting. Sourcing (proprietary vs. sponsor), diligence, and committee approval.

- Documentation & closing. Negotiating covenants, security package, and intercreditor terms; funding and fee collection.

- Monitoring. Reporting, covenants, borrowing bases, field exams, and board engagement.

- Amend/extend (if needed). Pricing step-ups, tighter covenants, additional collateral, or partial paydowns.

- Exit. Refinancing, sale of the company, or full repayment at maturity. In stress: restructuring, asset sale, or collateral enforcement.

- Recovery & lessons. Compare underwritten case to actual outcomes; update playbooks and sector views.

Understanding this lifecycle helps you see where a manager’s edge truly lies: sourcing? legal engineering? workout? sector specialization?

Macros that matter

Private credit lives in the real economy. A few macro variables deserve your attention:

- Rate cycles. Rising rates lift coupons but pressure borrowers’ coverage. Falling rates can reduce income; spread dynamics then matter more.

- Bank behavior. When banks retrench, private lenders gain pricing and structure; when banks compete aggressively, underwriting standards can slip.

- M&A cycles. Sponsor deal flow drives demand for acquisition financing and refinancings.

- Inflation. Floating-rate coupons can keep up, but rising input costs can erode borrower margins, stressing covenants.

- Regulatory shifts. Changes in capital rules for banks or risk-retention rules for securitization can alter supply/demand.

Great managers adapt—tighter docs and slower deployment in frothy periods; faster offense with better terms when the market dislocates.

What good risk management looks like

You’ll know you’re looking at a serious platform when you see:

- Clear credit culture. Independent risk teams that can veto deals; post-mortems on losses; compensation tied to long-term performance.

- Process discipline. Standardized memos, model archives, and approval matrices; no “exceptions by habit.”

- Workout capability. Internal legal and restructuring talent (or dedicated external partners) engaged early, not called in when it’s already too late.

- Data and technology. Systems that track covenants, KPIs, and borrowing bases; automated alerts; sector dashboards.

- LP communication. Candid letters, consistent metrics, and humility about mistakes.

Questions to ask before you invest

- Where in the capital structure do you lend, and why there?

- What’s your realized loss rate and non-accrual rate across cycles?

- Show me two tough deals—one saved and one lost—and what you learned.

- How tight are your docs? Show an example covenant package and intercreditor agreement.

- How do you size positions and set sector limits?

- What’s your fund-level leverage and covenant headroom?

- How do you treat fees and OID? Who gets what, and when?

- How much of the return is cash pay vs. PIK?

- How quickly do you mark down credits that slip?

- What’s the GP commit, and how is carry escrowed or subject to clawback?

If a manager answers calmly, with specific documents and data—not just stories—you’re hearing a real process.

The balanced view: why private credit can work in a portfolio

Pros

- Attractive income with floating-rate exposure.

- Structural protections (collateral, covenants) and direct monitoring.

- Lower mark-to-market noise than public credit.

- Diversification from equity beta.

Cons

- Illiquidity and multi-year capital lockups.

- Manager dispersion—the spread between top and median platforms is wide.

- Downturn sensitivity—defaults and losses cluster in recessions.

- Complexity—docs, valuations, and workouts require expertise.

For many investors, the appeal is clear: private credit can deliver compelling risk-adjusted income if you partner with managers who truly control their destiny—on the page (documents) and in the field (monitoring and workout).

Bottom line

Private credit is neither a magic income machine nor a hazard zone to avoid. It’s a contractual asset class where outcomes flow from underwriting discipline, documentation strength, portfolio construction, and workout skill. As you evaluate opportunities, keep your framework simple:

- Understand the strategy and capital-stack risk you’re taking.

- Follow the cash and the collateral.

- Gauge manager behavior when loans drift, not just when they close.

- Demand transparency on realized outcomes, not just projected IRRs.

Do that, and you’ll see private credit for what it is: a powerful source of income and stability when done carefully—and a reminder that the best protection for your capital is still the deal you choose not to do.

{kind=link}